10 Singapore blue chip stocks yielding more than 5%

PHOTO: Pixabay

The STI index is in the bear market territory (update: still feels like we are in one when every other markets has rallied) and naturally, one would expect most of the STI component stocks to be trading more than 20 per cent off their recent high.

Is the stock market carnage expected to continue? At the risk of trying to sound like I am “instigating” fear among the investment community, I believe we might still be at the early stages of the current bear market (Update: well, I have been dead wrong on this).

No crystal ball prediction, just my own personal “feel”. Again, there is nothing wrong with feeling fearful. Fear is what keeps us on our toes. Nonetheless, I am not saying that one should not be capitalizing on opportunities that might be present at the moment. Just make sure you don’t go ALL IN.

Below, we look to identify 10 Singapore blue chip stocks (form part of the STI index) that are currently yielding more than 5 per cent. Are they possibly undervalued?

To answer that question, I first look at their historical dividend payment trend. Next, I look at their current dividend yield relative to their historical dividend yield to identify signs of potential undervaluation (most are likely spotting a much higher dividend yield at this juncture).

I would then reference their forward DPS with what the street is expecting to see if a significant reduction might be on the cards which will make their current yield inflated.

Based on their average historical DPS payment and historical yield, I derived my fair value of the counter by dividing the average DPS by the average yield. This is a simplistic fair value calculation based on the Dividend Yield Theory.

I wrote in this article: Dividend Yield Theory – the underappreciated valuation tool, highlighting the usage of a counter’s historical dividend yield to evaluate if they might be fundamentally undervalued.

Personally, I believe this might be a better valuation tool for comparing US stocks vs. Singapore stocks due to the formers’ more robust dividend-paying profile. Nevertheless, it is a good reference point.

The table below illustrates the Straits Times Index stock components, the 30 largest Singapore Blue Chip stocks, their current price performance vs. 52-week high, sorted by their current forecasted dividend yield.

I showcase 10 Singapore blue-chip stocks that are currently yielding more than 5 per cent.

At the top of our list, we have got SingTel, once upon a time the largest market capitalization counter in Singapore. On the surface, the counter seems to be one of the most resilient Singapore blue chip stocks amid the current market carnage hit by Covid-19.

I mean most of us are probably not going to cut back on our mobile usage despite a potential recessionary scenario.

While not looking to do an in-depth analysis of SingTel in this article, I believe recent share price weakness could be due to concerns over its Bharti stake and skepticism over Bharti’s operational turnaround.

Concurrently, its Australia business is also facing mounting competitive pressure. Coupled with a high gearing profile, there are concerns that SingTel might have to cut its dividend in 2020.

Assuming Singtel maintains its $0.175 DPS payment (no longer the case), its yield will be at 6.8 per cent based on the current price which is very attractive for a relatively defensive play. However, do note its relatively high payout ratio close to 1x.

SingTel has an average DPS of $0.171 over the past 15 years with an average yield profile of 5.2 per cent. If we are to use these numbers, its calculated fair value (Average DPS/ average yield) based on our Dividend Yield Theory would be approx. $3.28.

At the current level of $2.56, it does seem like there is a good margin of safety to be progressively entering into this Singapore blue-chip stock that should be relatively resilient amid the Covid-19 issue.

Singtel has drastically cut its DPS from 17.5cts/share to just 12.3cts/share in its latest FY2020 full-year results.

Hence despite its share price is lower than when we first wrote about it (current $2.49 vs. $2.56), the forecasted yield based on an unchanged DPS of 12.3cts/share is roughly about 4.9 per cent, a shade below our required 5 per cent level.

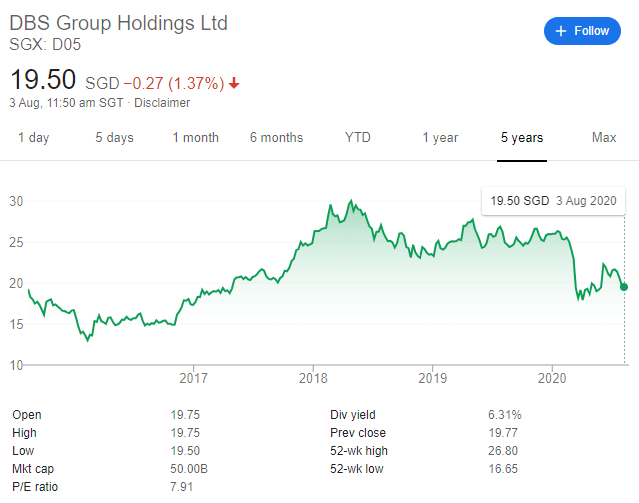

Another perpetual favorite among Singaporean investors, DBS Bank is the largest bank in South East Asia and one that is rightfully so, given its history of being at the forefront of banking/technological developments.

We have previously written that DBS bank is one of the Top 20 transformational global companies in 2019, a rare accolade among Singapore stocks.

I did not include DBS bank as one of my Top 5 resilient Singapore Stocks to buy amid Covid-19 uncertainty as I believe that its forward earnings could be significantly impacted due to economic slowdown as well as potential rise in NPLs as SMEs get impacted.

Nonetheless, I have got to admit that DBS remains one of the most well-run and respected Singapore Blue-Chip stocks, with a relatively resilient dividend payment profile since 2016 where DPS more than doubled in 2017 and has been maintained at a relatively high level since then.

Most analysts in the street do not expect a major dividend cut. If DBS maintains its current DPS of $1.23, its yield will be an attractive 6.5 per cent. This compared favorably to its 15-year average dividend yield of 4.2 per cent, with an average DPS of $0.76

Its fair value is calculated at $18.11 based on its 15-year average yield and DPS. However, if one does not expect its DPS to trend towards its average level of $0.76, then its fair value might be significantly higher. For example, an S$1 DPS will translate to an assumed fair value of $23.85.

The Monetary Authority of Singapore (MAS) has thrown a huge spanner, restricting the dividend payments of our local banks for 2020 to just 60 per cent of their 2019 level.

This has resulted in the share prices of our local banks such as DBS falling rather significantly by c.5 per cent over the past couple of trading days.

There is no guarantee at the present that 2021 DPS will revert back to the norm and it really depends on the economic outlook of Singapore.

DBS’s CEO Piyush Gupta has warned that the financial blowout could be rather significant in 2021 when the government is no longer able to financially dire SMEs can no longer survive the long-drawn recession.

Based on 60 per cent of 2019 DPS level, the forecasted yield of DBS is expected to be around 3.8 per cent

Casino stocks have been hard hit due to the virus issue and Genting Singapore has not been spared either, with its share price collapsing by almost 40 per cent from its 52-week high of $1.08

The company was recently disqualified from is Osaka casino bid due to late application submission and will now fully focus on competing for the Yokohama IR concession bid.

More critically, investors will be looking out for the impact that the Covid-19 might cause to its operations, whether it is going to be a 1-2 quarters issue or a longer-term threat to its operational performance.

The counter last traded this low back during the GFC period.

Based on its short dividend payment record, the implied fair value of Genting stands at $0.90/share vs. its current level of S$0.62. We assumed a sustainable DPS of $0.40 on an average yield of 4.0 per cent.

However, using the dividend yield theory to value stock like Genting might give a pretty erroneous conclusion due to the short dividend payment history. Hence even though its implied fair value is significantly above the current level, I will not be in a hurry to enter a position in the stock.

Earnings deterioration might be so significant if the global tourism industry remains in the doldrums for 2020 that the company might have to reduce its DPS significantly, taking into consideration hefty $4.5bn in Capex for RWS expansion.

A media behemoth that seems to be lost in a structural decline, SPH has seen its DPS reduced significantly from mid-S 20 cts to the current projected level of $0.11 for FY2020.

Even at the current level of $0.11 DPS, that still translates to an attractive 5.9 per cent yield on a yield standalone basis.

However, if one is to look back at its 15-year yield history, the average yield of the counter translates to approx. 6 per cent.

Hence, using $0.11 as our DPS basis (instead of the 15-year average DPS amount), our projected fair value of the counter is at $1.84 which seems to imply that despite the hefty decline in its share price over the past year, SPH is still not attractively valued, in our view.

A perpetual underperformer, SPH could remain a value-trap, one where the rebound in its share price likely lags its other blue-chip counterparts when the Covid-19 issue is finally contained.

Most Singaporeans will probably be familiar with Comfort Delgro, the largest Taxi operator in Singapore.

Ironically, it is also its taxi business that has been a key drag in the Group’s operating performance, with the latest impairment to its taxi segment a major negative surprise to the street.

The company also cut its final dividend, another nasty surprise, the first cut since 2008 to $0.098/share

Despite being seen as a relative defensive play, Comfort’s share price has also taken a beating, with its share price now hovering around the $1.62 level.

The street has a fair value over $2 for the counter at present. It remains to be seen if they will be rushing to upgrade the counter in-lieu of the hefty share price decline or to reduce the fair value of the counter significantly in their next round of review.

With an average 15-year DPS of $0.084 and an average yield of 4.4 per cent, our implied fair value of the counter is $1.92.

This implied fair value is approx. 15 per cent higher than its current price level, which makes Comfort Delgro one of the more attractive plays in this Singapore blue chip list.

A DPS reduction to $0.084 will still make this counter a 5.2 per cent yielder. I, however, don’t foresee such an aggressive dividend cut in 2020.

Further share price weakness to the $1.50 level will enhance the long-term return potential of the counter, in my view.

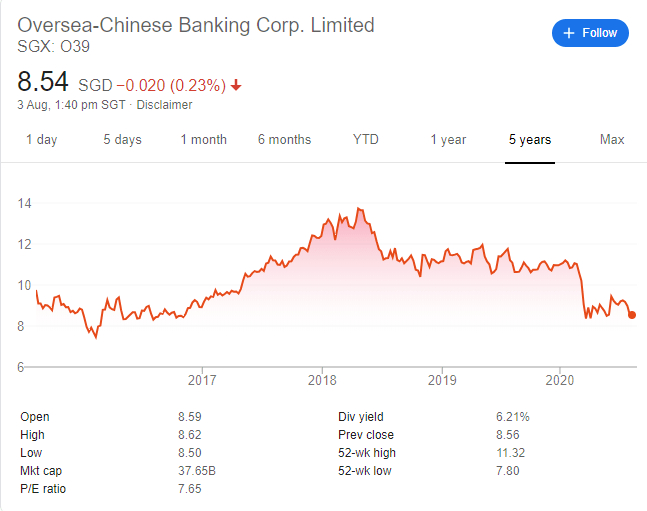

The second bank in our list, OCBC, just like its peers, has not been spared by the recent market volatility, with its stock now trading at c.$8.80, yielding approx. 6 per cent, assuming an unchanged DPS of $0.53 for 2020.

The last time OCBC’s yield exceeded 6 per cent was back during the GFC period.

The key concern for our local banks is a significant uptick in credit costs due to a prolonged virus outbreak. For OCBC, the bank has guided for credit cost to rise to about 25 to 30 basis points.

Despite a cut in earnings outlook, analysts are expecting dividend payouts to be sustainable due to strong CET-1 CAR, which is above 14 per cent.

Based on a 15-year average DPS of $0.34 and an average yield level of 3.8 per cent, the fair value of OCBC is at $8.93.

With the counter trading at approx. $8.72, the counter is trading just a shade below our assumed fair value.

One of our preferred REIT to purchase/put in watch-list amid the current Covid-19 volatility, Capitaland Mall Trust has one of the strongest track records when it comes to maintaining its dividend growth, an area which we highlighted in our article: Which S-REITs have the best track record of dividend growth.

With its share price having corrected to $1.92 at present, Capitaland Mall Trust is expected to have a forward yield of approx. 6.0 per cent.

We previously highlighted that the Covid-19 issue is undoubtedly having a much larger negative impact on Capitaland Mall Trust vs. Frasers Centrepoint Trust, the latter’s asset portfolio mostly comprising of suburban malls.

On the other hand, CapitaLand Mall Trust’s suburban mall only comprised 56 per cent of its FY2019 revenue, a significant decline from the 78 per cent back during the SARS period.

High-end malls such as Ion Orchard are still suffering from a lack of tourists, which accounts for a significant proportion of the malls’ footfall.

This can be seen from the share price outperformance of FCT vs. CMT.

CMT spots an average yield of 5.1 per cent with a 15-year average DPS of $0.10. Based on these two figures, we obtain a fair value of $2.00 for the counter, which is slightly above where the counter is currently trading.

I recently came out with a REIT scoring system for easy filtering of the “Best REITs” available right now, based on a combination of operational fundamentals as well as price attractiveness.

CapitaLand Mall Trust is 1 of the current 12 stocks with a score above 3.5 (out of a maximum of 5.0). For a full list of REITs and their respective scores, do refer to these two articles:

The only China-based counter in the list, Yangzijiang spots the lowest forward yield of 5 per cent in this Top 10 list of Singapore blue chip stocks.

I have written on Yangzijiang on several occasions, providing my take on the counter’s quarterly earnings performance.

I generally maintain a cautious view on the company’s operational outlook, based on an extremely challenging industry outlook where new orders have declined significantly.

Consequently, Yangzijiang’s order back is now at a record low, with its backlog only sufficient to support order construction till mid-2021.

Not only are new orders declining, but the gross margins on new orders are also expected to see a significant decline from mid-teens level to mid-single-digit by 2021.

On top of that, there is uncertainty over China’s credit situation. A rapid deterioration in the credit market could result in a hefty hit to Yangzijiang’s investment division.

With an average DPS of $0.043 since 2008 when it listed, the counter spots an average yield of 3.9 per cent. Based on that, its implied fair value of $1.09 v. current share price level of $0.82.

While there is a 30 per cent upside to our implied fair value, I remain concerned over a significant deterioration in the company’s operating performance over the next 1-2 years which ain’t just a Covid-19 issue.

UOB makes the list as one of the top Singapore blue-chip stocks with a yield of over 5 per cent. If UOB’s DPS of $1.30 can be maintained, its yield will amount to 6.6 per cent based on the current price of $19.60.

The difference in UOB’s yield (now at 6.6 per cent vs. GFC (based on average 2009 yield of 4 per cent)) is now at 2.6ppt, the largest among the three banks. DBS yield difference is 2ppt while OCBC yield difference is 1.8ppt.

Hence, assuming a similar compression rate, UOB does present the highest share price upside on this metric.

The counter has an average DPS payment of $0.81 and an average yield of 4 per cent. Based on that, our fair value assumption of the counter is $20.08.

With UOB trading at $19.62, there is a 2.4 per cent upside at present, similar to OCBC.

SATS makes it to our list of Top 10 Singapore blue chip stocks with a yield of over 5 per cent. If the company can maintain its track record of DPS growth, which has been unbroken since 2014, the counter would yield 5.6 per cent.

However, I believe that SATS dividend growth track record will come to an end in 2020, with a potential large dividend cut in 2020 due to the large negative impact from the rapidly declining global tourism industry.

I like SATS as a non-capital-intensive levered play to the tourism industry. However, that can prove to be a double-edged sword, with the once robust tourism industry now witnessing its worst-ever industry downturn since the SARS period back in 2003.

SATS’s performance will likely be hugely impacted when the company reports its FY4Q20 results and there are concerns that the company’s dividend will come under heavy downward pressure.

Based on an average 15-year DPS of $0.15 and an average yield of 5 per cent during this period, the implied fair value of the counter is $3.04. With the counter trading at $3.36, it is still a 10 per cent premium to our implied fair value.

This list of 10 Singapore blue chip stocks yielding more than 5 per cent is meant to be a reference guide and not a recommendation to Buy or Sell any of the counters mentioned.

Personally, the ones that are looking attractive to me are SingTel and ComfortDelgro. SingTel currently spots a share price last seen 15 years ago (based on average price) while ComfortDelgro’s share price is also at an 8-year low.

Both these counters can be considered relatively defensive although ComfortDelgro’s taxi division remains a major operating concern to me.

The local banks’ earnings are clouded with uncertainty and there is just no telling how much credit cost and non-performing loans might rise for our banks if the Covid-19 issue drags beyond 2H20.

However, on a valuation basis, using yield as a gauge, it is getting more attractive. Our assumption used a pretty conservative DPS (36 - 38 per cent DPS haircut from the current level) for each of the 3 banks in our fair value calculation.

That is not likely to be the case. Among the 3 banks, UOB might present the greatest upside based on current yield compression vs. GFC level.

To expand my list further in this follow-up article, I highlight names that have a market cap of around $3bn with a potential yield above 5 per cent although they might not be part of the STI component stocks.

This article was first published in New Academy of Finance. Disclaimer: All content is displayed for general information purposes only and does not constitute professional financial advice.