Could prime CCR condos start surging in demand after Q3 2021?

PHOTO: Stackedhomes

Overall home prices continued their steady upward pace in 2021; but property analysts have tipped private property prices to continue their rise as 2021 comes to a close.

Prime region properties, which were lagging far behind fringe region counterparts, have shown signs that demand could be on the uptrend. Let’s look at what’s been happening and some of the possible reasons why:

The condo market retains its momentum, climbing for the sixth consecutive quarter. URA flash estimates show prices edging up to around 0.9 per cent, broadly similar to the pace set in Q2 (0.8 per cent rise).

While modest, Q3 mostly beat expectations. It was thought that a combination of the Heightened Alert (July to August), and the Seventh Month Festival (August to September) would see a much cooler market in Q3. As it turns out, most buyers have shrugged off these concerns.

The Core Central Region (CCR) saw prices dip by 0.6 per cent, as opposed to a 1.1 per cent increase in Q2.

Interestingly, the red-hot Outside of Central Region (OCR) market also saw prices drop; a decrease of around 0.2 per cent, down from a 1.9 per cent increase in the previous quarter. This is despite the majority of top sellers – at least for the month of August – coming from this region.

The RCR saw the highest increase with prices up 2.2 per cent. In the previous quarter, RCR home prices were only up 0.1 per cent. But this is mainly on the back of Normanton Park and Avenue South Residence, where developers raised prices.

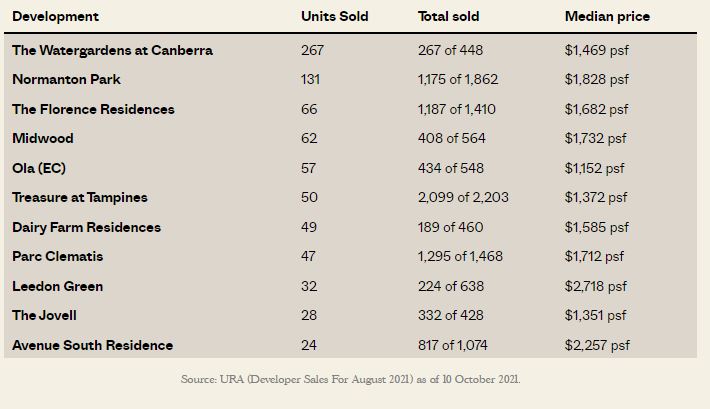

Data below excludes ECs

In the CCR, condo prices averaged $2,387 psf, while RCR condos averaged $1,781 psf. In the OCR, prices averaged $1,374 psf.

Details for the best sellers of September 2021 are not yet released at the time of writing. Follow us on Stacked so we can provide you with an update.

Note that apart from Leedon Green (CCR), Normanton Park (RCR), and Avenue South Residence (RCR), all other developments were in the OCR.

There’s a growing demand for luxury homes in 2021. In August, for example, Les Maison Nassim saw a jaw-dropping transaction at $5,786 psf, or $35 million, which was the record for the month.

The boutique Park Nova at Orchard – which only recently launched – has already sold 18 units, at an average price of $5,016 psf. It’s certainly no small feat given the large sizes and subsequently large units. The cheapest unit transacted there so far was at $6.7 million – an amount that could get you a landed home in a decent location.

These types of boutique properties are small in number; so buyers unable to secure a unit are likely to cast their gaze over the wider CCR market. If so, there’s no end to new launches upcoming in 2021 in the region, such as Canninghill Piers and Perfect 10.

The second reason is the return of affluent foreign buyers. Certain incidents abroad, such as China’s clampdown on tech moguls, are also driving this; and due to political unrest, our closest competing real estate market – Hong Kong – may not be as viable right now.

The biggest signs are clear for all to see – 16 per cent of purchases in the Core Central Region during July and August 2021 were by foreigners, doubling the 8 per cent seen in Q2.

In fact, some realtors have pointed out that price dips may be related to this. Developers attempting to target wealthy Chinese buyers may be lowering the price slightly, hoping to raise awareness and get further momentum going.

(We don’t think buyers in this demographic are hugely concerned about the price though!)

Lastly, border measures have been easing which further points to more activity from foreigners looking to purchase property in Singapore.

| Category | Countries/Territories (From 13 October 2021) |

| I | Hong Kong, Macau, Mainland China, Taiwan |

| II | Australia, Austria (new), Bahrain (new), Belgium (new), Bhutan (new), Brunei, Bulgaria (new), Canada, Croatia (new), Cyprus (new), Czech Republic, Denmark, Egypt (new), Fiji (new), Finland, France, Germany, Greece (new), Iceland (new), Ireland (new) , Italy, Japan, Liechtenstein (new) , Luxembourg, Malta, Netherlands, New Zealand, Norway (new), Poland, Portugal, South Korea, Saudi Arabia, Slovakia (new) , Spain, Sweden, Switzerland (new), Turkey (new), UK (new), USA (new), Vatican City (new) |

| III | Estonia (new), Latvia, Lithuania, Maldives, Slovenia (new) |

| IV | All other countries/territories |

| VTL | Current: Germany, Brunei From Oct 19: Canada, Denmark, France, Italy, Netherlands, Spain, UK, USA From Nov 15: South Korea |

| ? SHN Measures by Category and Vaccination Status | ||

| Fully-Vaccinated | Unvaccinated | |

| VTL | No SHN | Not allowed |

| Category I | No SHN | |

| Category II | 7-day SHN (home/hotel) |

|

| Category III | 10-day SHN (home/hotel) |

10-day SHN (hotel) |

| Category IV | 10-day SHN (hotel) |

|

Overall, developers with CCR offerings are likely in for an easy ride in 2021; despite Covid-19 and viewing difficulties.

It’s hard to draw too much from a single quarter. But given how crazy the market has been, any hint of a slowdown is great for first-time homebuyers/upgraders. Still though, realtors have mentioned there are not many new launches in the fringe regions as compared to the bumper crop from before.

This is still a limited supply, given the surge of upgraders who like the OCR. As such, you may want to start considering resale options.

We can provide you with the most in-depth reviews of new and resale properties alike on Stacked; so follow us for more insights as the market changes.

This article was first published in Stackedhomes.