The investment roller coaster

It is often said that we are our own worst enemy when it comes to investing because we allow our emotions to get the better of us.

And that is not just a financial folk tale: There is a wealth of behavioural finance studies showing that investors are not motivated by sound practices but by greed and fear.

Many retail investors find it difficult to ignore the noise in the market. Led by herd instinct and fed by greed, they jump on a bandwagon, resulting in overvalued assets.

When the values of their portfolios plummet due to declining equity markets, fear takes over and most investors go into a selling frenzy.

Some of us would have experienced that sinking feeling recently when anxiety and fear took over as a result of markets heading south due to factors such as Brexit, pending interest rate hikes in the United States and China's slowing economy.

Greed and fear are also singled out by financial research firms like Dalbar as the primary emotions that lead investors astray. US-based Dalbar has been tracking the effects of investor decisions to buy, sell and switch into and out of unit trusts since 1984.

The results consistently show that the average investor's performance is more dependent on his investing behaviour than on fund performance. Mutual fund investors who hold on to their investments are more successful than those who try to time the market.

Ms Tan Wei Mei, head of portfolio solutions for Asia Pacific at Credit Suisse Private Banking, says psychology plays a big part in investing, and so understanding psychological motivations and behavioural biases can help investors avoid financial pitfalls.

10 common biases investors should look out for

"Our brains, behaviour and culture affect our investment decisions," she adds.

In fact, finance experts like Mr William Cai, vice-president at GYC Financial Advisory, believe we are naturally programmed to lose money.

"Most investors are often willing to invest only after they feel 'safe', which is often the worst time," he notes. "Ironically, it is hard for investors to make a bold decision to invest when I see the opportunities, as it is always during a time when it feels wrong to invest."

That is why most investors do not make money from the stock market. They invest at a market peak and bail out at market bottom, only to repeat this losing process.

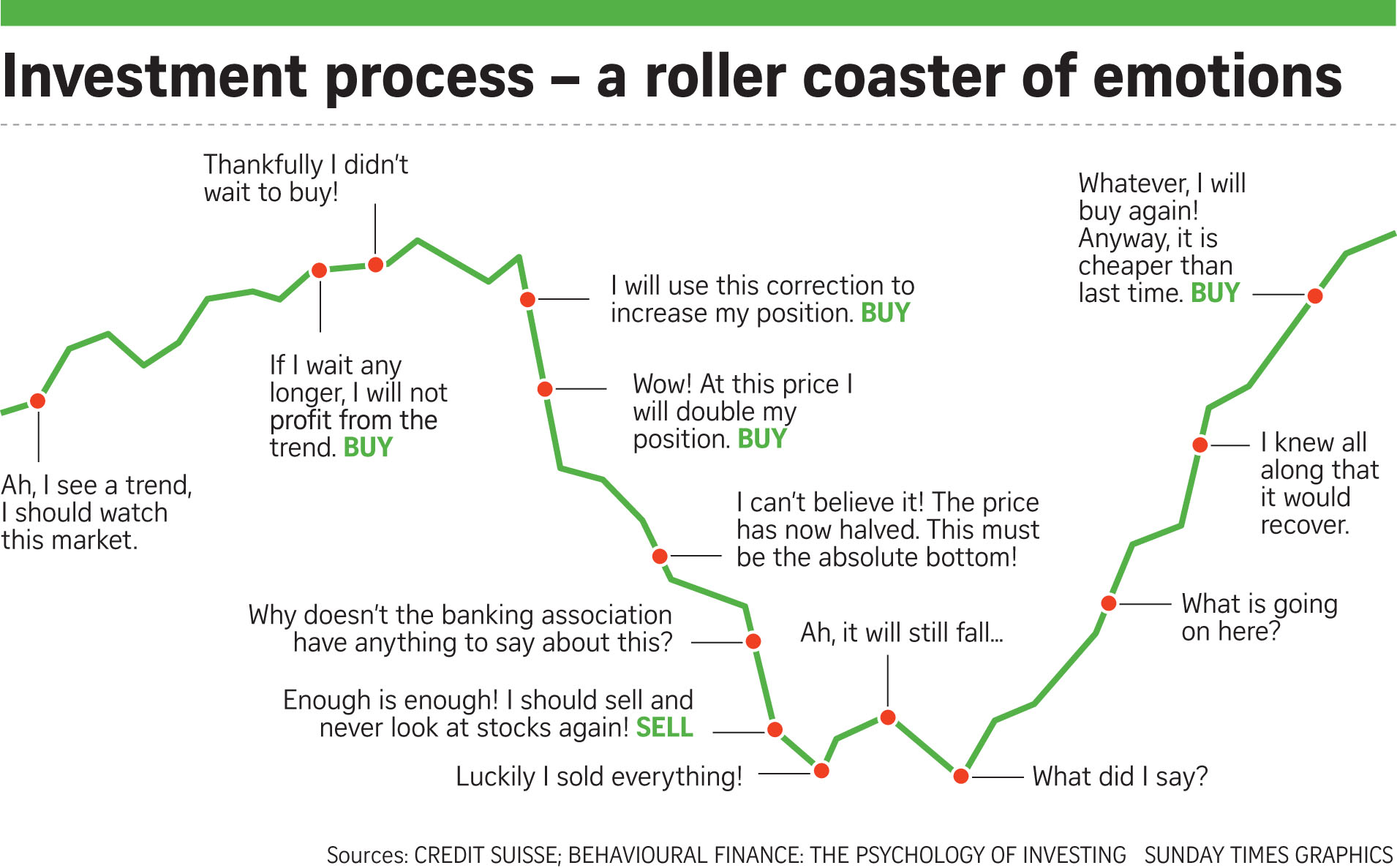

The investment roller coaster In a bull market, the actions of optimistic investors push assets higher, until the investment process reaches euphoria - the point at which they are most bullish.

More and more investors will decide to catch the uptrend before it is too late and end up buying at high prices.

But the market would likely have become overvalued and ripe for a fall by then. It may just take a bit of bad news to start shares sliding.

Investors would see the initial sell-downs as a short-term phenomenon, not realising that it is more than a "buy on dips" opportunity and that a bear market has begun.

Fear raises its ugly head when prices start plummeting and anxious investors become more pessimistic, liquidating their positions and so selling at low prices.

Having been bitten by losses, investors feel remorse as the market recovers. They typically wait too long before getting back on the roller coaster again, when the market shows signs of recovery.

As you can see, this behaviour is counter to the "buy low, sell high" investment advice.

Behavioural finance biases Here are 10 common biases highlighted in a recent report from Credit Suisse in collaboration with the University of Zurich with research conducted by Dr Thorsten Hens and Ms Anna Meier.

ANCHORING

Investors tend not to rely on fundamental factors when making decisions. Rather, they base their decisions on the price at which the stock was bought. This acts as the anchor that causes irrational decisions. Anchoring influences decisions when investors do not realise how the information is presented.

Let us assume you are faced with three set-meal choices at your favourite food stall. Set A is a $5 value meal of nasi lemak while set B is a $10 special-value meal of nasi lemak with soup, drink and dessert. Most people will opt for set A.

One day, the stall owner introduces set C - an $11 standard meal of nasi lemak with drink and dessert.

Ms Tan says that with the introduction of an anchor, which in this case is set C, most will change their decisions and opt for set B as it appears to offer the best value.

"Anchoring occurs when you are influenced by information of little or no relevance and primes us into making quick and irrational decisions without doing much or further research," she says.

MYOPIC LOSS AVERSION

Most investors fear losses more than they enjoy profits. As such, people strongly prefer to avoid losses than acquiring gains.

So if they have a habit of checking their stock portfolios too often, they may see they have lost money and decide to sell everything off.

To counter this, a long-term view would be better and they should check their stock performance less frequently.

OVERCONFIDENCE

Most times, we overestimate our own abilities and think we are above average. In fact, experts overestimate themselves frequently, and to a greater degree, than laypersons do. Overconfidence is often seen when markets are on the rise.

CONFIRMATION BIAS

This refers to the phenomenon of seeking selective information to support your own opinion or to interpret the facts in a way that suits your own world view. Investors seek confirmation for their assumptions. They avoid critical opinions and reports, reading only those articles that put their point of view in a positive light.

HOME BIAS

Most investors tend to purchase stocks from firms in their home country. It is easy to understand why. After all, they grew up with these company names, so there is greater familiarity.

FAVOURITE LONG-SHOT BIAS

People who fall into this psychological trap always bet on the long shot because it promises very high returns. The downside of this is that they forget that the likelihood of the long shot winning cancels the profit.

FRAMING BIAS

Here, decisions are based mainly on how facts are depicted or worded in statistical terms. For instance, some people may not realise that "Four out of 10 are winners" and "Six out of 10 are losers" mean the same thing.

The statements are identical, but most people do not realise it.

GET-EVEN-ITIS

This refers to the inclination of risking more to avoid a definite loss, even if it may result in a greater loss. The Credit Suisse report highlighted that this behaviour is seen in all cultural regions.

MENTAL ACCOUNTING

Many investors make distinctions mentally that do not exist financially. Often, losses incurred are viewed separately from paper losses.

People are too quick to sell stocks when they make gains and too slow to sell when they sustain a loss.

REGRET AVOIDANCE

If we invest in a blue chip and it does not perform as hoped, we attribute it to bad luck. However, if we invest in a niche product that fails to perform well, we tend to regret this more than we do the failure of the blue-chip stock.

This is because we are comforted that many others have made the same mistake and thus our decision to buy does not seem so wrong.

Tips to retail investors

DON'T TIME THE MARKET

Findings suggest that the average investor attempts a market-timing approach, which usually does not work in their favour and they end up doing poorly in their investments. Though it is beneficial to avoid market downturns, very few investors actually do so consistently and successfully.

Investors seemingly switch in and out of funds at the wrong time, moving out of low-performing ones just before a recovery, and moving on to high-performance funds just before a fall.

Because it is difficult to accurately predict market movements all the time, it is time in the market that matters.

Understand that market volatility is part and parcel of investing and that missing out on opportunities for gains can affect your returns. Financial advisers have a role to play when fear and panic set in, advising clients not to sell in panic and wait to get back in later.

To manage volatility, finance experts encourage investors to apply dollar-cost averaging, which means investing in smaller, regular amounts via a savings plan, regardless of fluctuating price levels. Dalbar found that investors who practise dollar-cost averaging reap 50 per cent higher returns.

RECOGNISE YOUR OWN PSYCHOLOGICAL BIASES

Just as it is essential to understand your investment timeframe and objectives, you should be aware of your psychological capabilities and money habits.

Ask yourself: Do I usually react to market noise? Am I constantly self-sabotaging my investments because of my investing biases?

Know that the markets are not solely driven by fundamentals but by investing behaviour, which is irrational at times.

Once you are aware, work on the steps to achieve your goals and inculcate the drive and commitment to want to change. This may include reviewing your diversified portfolio on a regular basis and engaging a financial adviser.

At Credit Suisse, it is possible to identify your behavioural biases with a diagnostic test. In addition, its advisory process can help investors explore their actual risk ability and risk appetite, as well as identify their current financial knowledge.

So the long-term performance of your investments depends a lot more on how you behave than on how your stock or fund behaves. Preventing the roller-coaster cycle of emotions requires having discipline, an understanding of your psychological make-up and a plan in place.

This article was first published on July 31, 2016.

Get a copy of The Straits Times or go to straitstimes.com for more stories.