Timing the market: Is it a good time to enter the financial markets now?

PHOTO: Unsplash

Talking to our friends and clients, we discovered that many have put their investment plans on hold, citing the same concerns: That the markets may have bounced back too much, and they should wait to go in at lower levels.

We know we shouldn’t and we don’t like to admit it, it is just too tempting to try to time the market.

In February and March, as markets were falling, many were also hesitant to invest out of fear that the markets could fall further. No matter how circumstances and the direction of markets change, the fundamental drivers of human psychology and behaviour don’t.

We are worried about the “what-ifs”, and this often leads us to inaction. We are limited in our ability to execute an investment because we are either scared to lose money (fear), or because we feel that we can buy it at a lower price and achieve greater upside (greed).

It is not the aim of this article to attempt to definitively answer the question posed in the title. However, we do need to assess where the markets are and also look into why we feel, think and act this way despite our best intentions.

We must overcome these fears (and tame our greed) to achieve the long-term investment outcomes that are needed to secure our financial future.

Let’s reflect on what we have just experienced. Who would have thought as we were consoling our clients (which includes all the employees of Endowus!) and licking the painful wounds of financial losses in the throes of the crisis in March, that in just two and half months, we would have experienced one of the fastest market recoveries in history.

Markets have recouped most of the losses and are up 40 per cent+ from the bottom. All of this happened during a period of massive economic and social dislocation, while global Covid-19 cases were still on the rise.

In fact, as the table above shows, the S&P 500 Index recovered all of its losses for the year, while the Nasdaq index and a few other better-performing markets had already made it into positive territory for the year.

It is also important to note that the major global fixed income index had recovered its losses earlier since April, working effectively as a natural diversifier.

Hopefully, many investors are in a position where they have recovered a significant portion of the losses from earlier in the year. So a common question that our investors ask is, “Where are we headed from here?”

The bear case is clear – it is characterised by the sentiment – “but things are still so terrible!” It is the exact same reasons why the markets fell in the first place as it came to grips with the reality of a global pandemic, the far-reaching consequences of the subsequent lockdowns, and its associated economic and social fallouts.

Earnings were being slashed, companies were declaring bankruptcies, people were losing jobs in the tens of millions, and people were sick and dying.

[[nid:496815]]

As the stock market is a leading indicator, before we saw any data that confirmed our worst fears, we had already sold down the market by more than 30 per cent and ranked it as one of the worst – albeit one of the shortest – bear markets in history.

Uncertainty is the biggest enemy of the stock market, and we have had massive doses of it.

Are we certain about the future outlook of the economy? Maybe not. Valuations are stretched and short-term technicals are extended, so a short-term correction is a natural concern.

If the correction extends itself, the question of whether we will see the previous low or go beyond to new lows will surely haunt us and our decisions.

We know that human beings are terrible at forecasting but yet we continue trying. Basing those forecasts on macroeconomic indicators that come out with a significant lag is a loser’s game. After all, markets fell dramatically before anyone could even shout recession!

The problem is that the bull case is equally clear – it is summarised by the sentiment that the worst is over. The rate of daily new infections for Covid-19 have peaked and while we worry about a second wave, every day is one hopeful day closer to a vaccine or therapeutic drug development.

Unemployment numbers have peaked and earnings have bottomed.

Some tailwinds of lower inflation and lower prices are everywhere (including in oil prices). It also means household balance sheets are being shored up by less spending and lower cost. With the gradual reopening of the economy, it seems that there is finally a light at the end of the tunnel.

Government fiscal support (i.e. cheques in the mail!) is filling what is seen as a temporary demand gap, while central bank liquidity pumping supercharges the financial markets.

All around the world, major central banks have coordinated rapid interest rate cuts and introduced quantitative easing at an unprecedented scale.

We need to understand that financial markets are also driven by demand and supply. Trillions of dollars of cash are sitting on the sidelines, with pension funds and retail savers continuing with their investments and regular savings plans.

There is no new supply to the market – be it IPOs, rights issuance or forced sellers, although a recovering market will entice a few issuers.

These may be some structural reasons for a rising market, driven by an abundance of liquidity and an ageing population that finds fewer and fewer alternative opportunities to generate the yields needed to secure their future.

Furthermore, markets are as explained, a leading indicator; the bulls would argue that the bad news is priced-in and unless we see things we have never seen before, we will not be surprised.

Regardless of where the markets head from here, there is a group of investors who have recently been touted as the big winners of 2020 by the media – it has been retail investors, as a group, who have won out.

This may be because they did not panic and sell into the correction unlike institutional investors, who collectively dumped stocks. Whether these individual investors were shell-shocked into inaction or were accustomed to buying the dips and just carried on buying into falling markets, they clearly made the right call.

It is encouraging that most individual investors remain invested in their long-term retirement accounts and also continue putting money into regular saving plans and pension plans. This led to a net inflow in passive investment products.

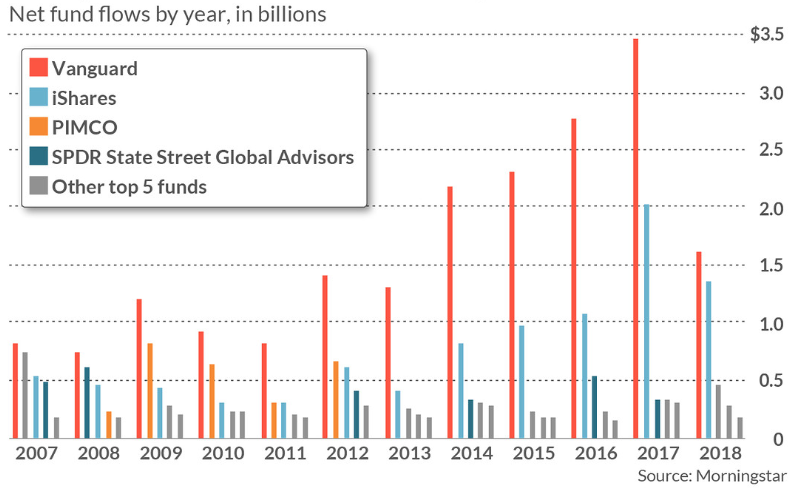

Vanguard Group, which saw the largest inflows in the US for all index mutual funds and ETFs, emerged as the biggest beneficiary. The largest asset manager in the world is Blackrock, but in the retail mutual fund and ETF market in the US, Vanguard rules supreme.

[[nid:494310]]

This is nothing new – Vanguard has seen more net inflows than Blackrock every single year since 2007.

While the above chart ends in 2018, Vanguard saw the biggest net inflows in 2019 and again in the first quarter of 2020. On the current trend, Vanguard is projected to overtake Blackrock as the largest asset manager globally within the decade.

Our partnership with Vanguard means that CPF members have an option to invest passively in globally diversified portfolios exclusively through Endowus.

By utilizing a passive low-cost investing strategy and exercising the power of dollar-cost averaging (DCA), individual investors who stayed the course, especially those that stuck to their long-term financial investment plan, came out as the big winners.

One of the most frequent questions we receive from clients is whether to invest a lump sum or to spread out the investment over a period of time through dollar-cost averaging.

There is no simple answer as it depends on your age, your future income (whether there is more money to be invested to DCA in the future), your risk appetite, your investment goals and future liabilities.

Historical and empirical evidence on DCA have suggested that the longer you spread out your investments, the poorer your returns are relative to lump sum investing.

If you consider how the stock market trends upwards over the long run, then it’s easy to understand that as time passes, you miss out on the compounding returns of stock markets.

Obviously, there are exceptions as nothing is always so simple, otherwise the gurus would have penned foolproof strategies on market timing. For instance, investing in a lump sum at the beginning of 2020 would have lost out to dollar-cost averaging.

However, the jury is still out on the full-year returns for 2020. It is also a very short period that we are looking at and if we look further back to the beginning of 2019, then the chart below clearly shows that lump sum would have led to a better outcome.

The above chart shows 6 scenarios for S&P 500 monthly returns Jan 2019~May 2020.

The reason why DCA and a regular savings plan are critical in our investment plan is that they align with our monthly income cycle. Setting aside a certain portion of our income on a regular basis and investing it in markets helps us to curb our natural instinct to try our hand on market timing.

The bite-sized investments lower the hurdle of putting our money to work and removes barriers to inaction. It is an antidote to our behavioural problems.

As we make our way through another potential period of heightened volatility caused by higher levels of uncertainty, I hope that empirical evidence and historical precedence have taught us all some valuable lessons in our investing journey – particularly that time in markets is more important than timing the market.

Having a financial plan that is suitable for you and your goals and sticking to it, even and especially through periods of uncertainty and volatility. It pays to be fully invested and to remain invested in the markets, especially if you have more income in the future.

Remember that it’s more about managing risk than maximising returns that will give you the peace of mind you need to make your money work for you, so that you can live easier today, and better tomorrow.

For the latest updates on the coronavirus, visit here.

This article was first published in Dollars and Sense.