5 best credit cards to use for Black Friday 2025 in Singapore

PHOTO: Pexels

Black Friday isn't just about snagging the best deals — it's about making every dollar work harder for you.

With the right credit card, you can stack cashback, rack up rewards, and even dodge those sneaky foreign transaction fees when shopping on overseas sites.

But with so many cards out there, how do you know which one really delivers?

Whether you're eyeing gadgets on Amazon, filling your cart at Shopee, or nabbing limited-time vouchers, choosing the right card can mean the difference between a good deal and a great one.

Below, we break down the best cards for Black Friday 2025 — plus a few smart tips to help you save even more as you shop.

Ready to make the most of your Black Friday haul? Let's dive in.

| Credit card | Best for these Black Friday purchases | Key reward/feature | Cashback/Points cap | Min. spend for perks |

| Citi Rewards Card | Scattered small-to-medium online buys—think groceries, food delivery, fashion, ride-hailing, or daily deals across multiple sites | 10X points (4 miles/$1) on online, groceries, food delivery, ride-hailing | 9,000 bonus points/month (~$1,000 spend) | None |

| DBS Woman’s World Card | Big-ticket Black Friday hauls and large online spends—ideal for shoppers who want to max out rewards with 1 or 2 big purchases | 10X DBS Points (4 miles/$1) on online spend | $2,000 online spend/month | None |

| UOB EVOL Card | Blending online shopping, in-store contactless (Apple/Google Pay), streaming, gym, telco and overseas Black Friday deals—great for digital natives and travellers who want high cashback and 0% FX fees. | 10% cashback (online, contactless, gym, telco, streaming), 3% overseas FX spend (till 31 Jan 2026), 0% FX fees worldwide | $80/month (category sub-caps apply) | $800/month |

| OCBC FRANK Card | Overseas and local Black Friday shopping, especially on foreign sites or with eco-friendly brands—perfect for those who want cashback on international buys | 8% cashback (online, mobile, FX), +2% on green merchants | $100/month | $800/month |

| HSBC Revolution Card | All-rounder for any online or contactless Black Friday deal—ideal for set-and-forget shoppers who want flexible rewards with no annual fee or min. spend | 10X points (4 miles/$1 or 2.5% cashback) on online/contactless | 13,500 points/month (till Feb 2026) | None |

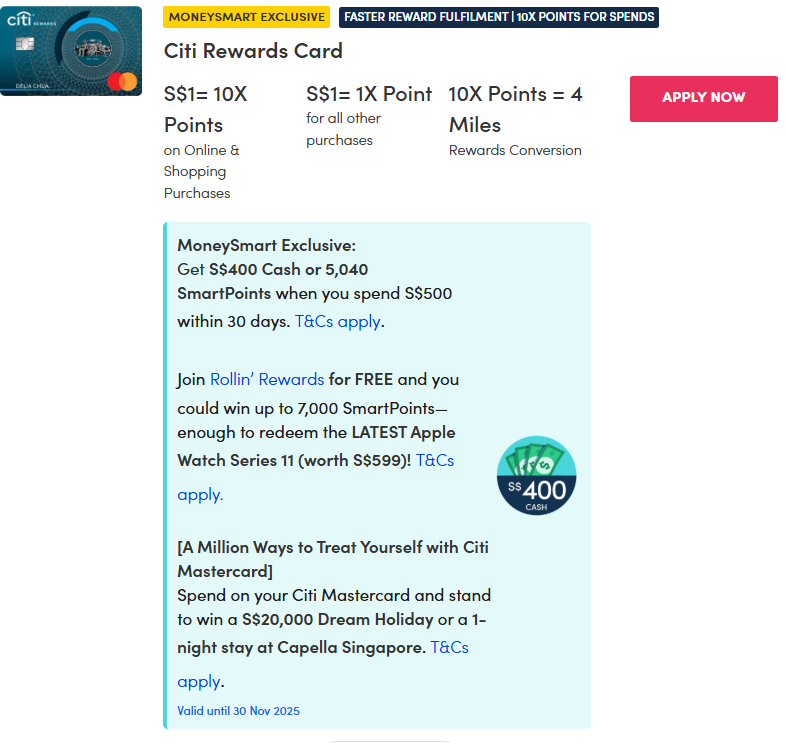

If you love shopping online or in-store, the Citi Rewards Card is built to help you rack up points fast on everyday purchases. You'll earn a whopping 10X Citi ThankYou Points (equivalent to 4 miles per $1) on a wide range of online spend — from groceries and food delivery to ride-hailing, fashion, and department stores.

With a cap of 9,000 bonus points per statement month (or roughly $1,000 in eligible spend), it's an easy way to maximise rewards on the things you already buy.

Redemption is flexible-points last five years and can be swapped for miles, shopping vouchers, or used to offset purchases directly. There's no minimum spend, and you'll also enjoy up to 14 per cent fuel savings at Esso and Shell, plus access to Citi World Privileges globally.

Just keep in mind that travel-related and mobile wallet transactions aren't eligible for bonus points, and the annual fee is $196.20 (waived the first year).

Key facts:

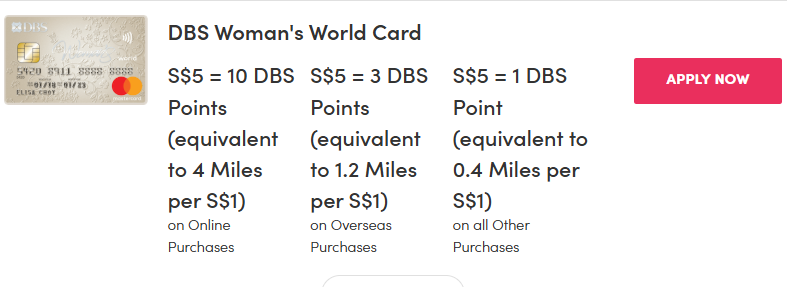

Despite the name, the DBS Woman's World Card is open to everyone — and it's a real favourite among high-volume online shoppers. You'll earn a powerful 10X DBS Points (equal to 4 miles per $1) on online spend, with the flexibility to redeem for air miles, vouchers (including to the Apple Rewards Store!), or cashback.

Whether you're shopping on e-commerce sites or booking your next staycation, this card's perks are tough to beat-plus you get complimentary e-commerce protection for extra peace of mind on your purchases.

Do beware there's a cap of $1,000 in eligible online spend per month for the 10X points. Additionally, the annual fee is $196.20 (waived in the first year), and you'll need a minimum annual income of $80,000 to qualify. One highlight: DBS Points can be converted to miles instantly via the app, or used for immediate redemptions at checkout.

Key facts:

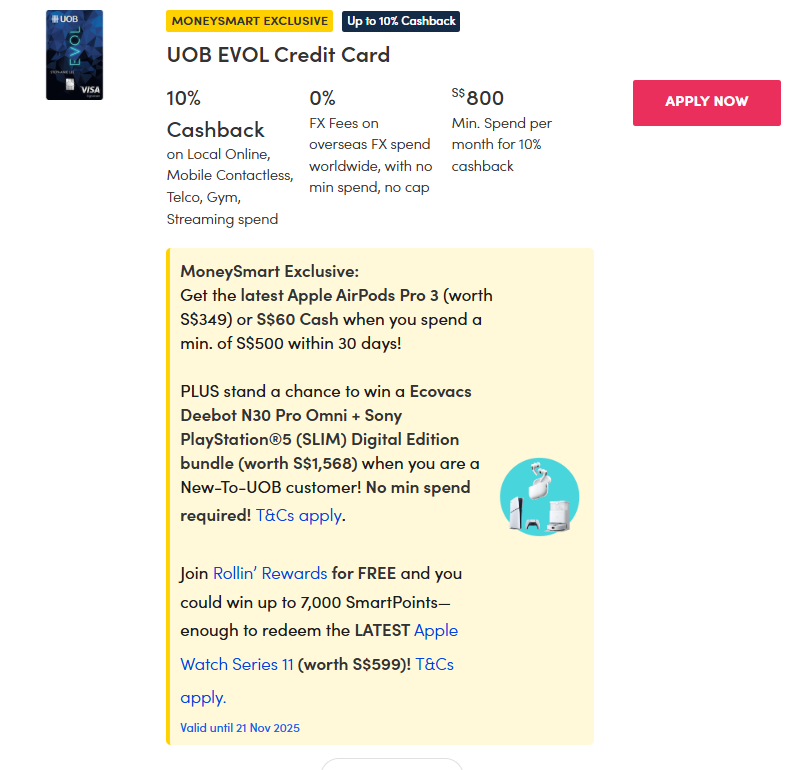

The UOB EVOL Card is a go-to for digital natives who want fuss-free cashback on all the essentials. You'll enjoy up to 10 per cent cashback on local online shopping, mobile contactless payments (like Apple Pay or Google Pay), as well as gym, telco, and streaming bills.

Overseas spenders also get a rare perk — 0 per cent FX fees worldwide, so you can shop internationally without extra charges. On top of that, enjoy three per cent cashback on all overseas foreign currency spend till Jan 31, 2026.

To unlock the bonus cashback rates, just hit a minimum $800 spend per month. The card's monthly cashback cap is $80, broken down into further category sub-caps, so you'll want to plan your spending to maximise each dollar.

The annual fee is $196.20 but is waived for the first year — and can stay free if you make at least three transactions each month for a year. It's perfect for those who use digital wallets, stream entertainment, or shop on global platforms, and prefer cashback that's easy to track and redeem.

Key facts:

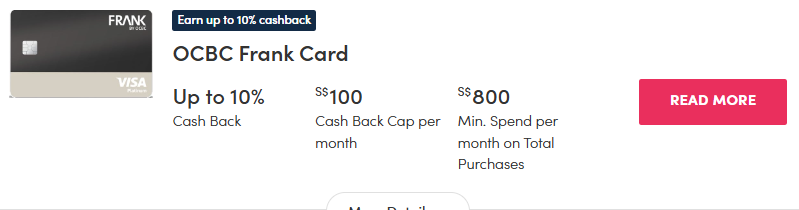

The OCBC FRANK Card is a favourite among young adults who want simple, high cashback on their everyday digital lifestyle. You can earn up to eight per cent cashback on online and mobile contactless purchases in Singapore, plus eight per cent cashback on all foreign currency spend — perfect for those who shop internationally during Black Friday.

If you spend with eco-friendly merchants like SimplyGo or BlueSG, you'll enjoy an extra two per cent bonus cashback, rewarding you for going green.

To unlock the full cashback, just hit a minimum spend of $800 per month. There's a generous cashback cap of $100 each month, so you can maximise rewards without overthinking categories.

Annual fees are waived for the first two years, and after that, you only need to spend $10,000 per year for continued waivers. It's a strong pick for digital-first and eco-conscious spenders.

Key facts:

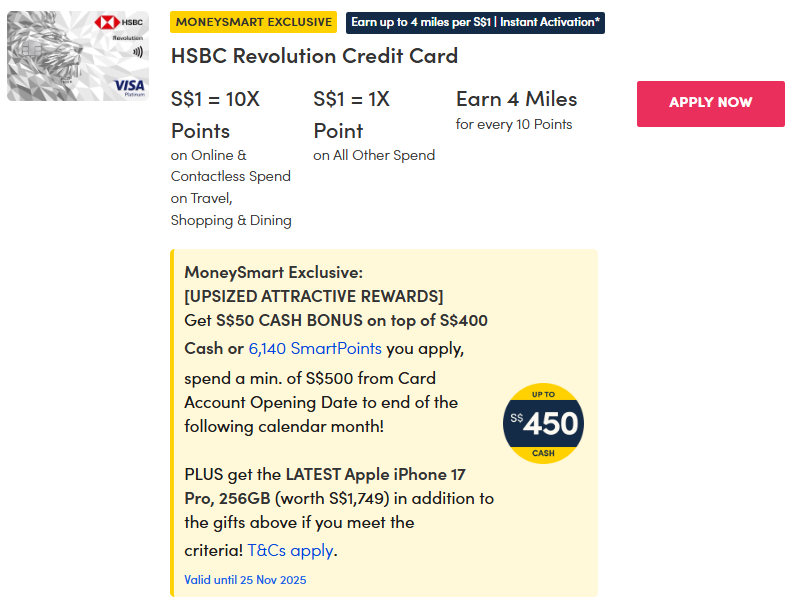

The HSBC Revolution Card is a fuss-free favourite for anyone who wants to rack up miles or cashback on daily spend — without worrying about annual fees.

You'll earn 10X Reward Points (that's 4 miles or 2.5 per cent cashback per $1) on a huge range of categories: online shopping, dining, travel bookings, ride-hailing, entertainment, and all mobile contactless payments (Apple Pay, Google Pay, Samsung Pay).

With no minimum spend and no annual fee, it's super accessible for those who want rewards on everything from Shopee splurges to weekend brunches.

For moderate spenders, the newly raised bonus cap — 13,500 points per month until Feb 28, 2026 — means you can optimise your Black Friday haul. Points are flexible: redeem them for air miles, cash, or gift cards, but do remember they expire after 37 months. The main watch-out is the $65,000 minimum income requirement (from October 2025), and certain transactions like insurance, utilities, and bill payments are excluded from bonuses.

Key facts:

Want to make your Black Friday haul even sweeter? Here are some tried-and-tested ways to squeeze the most value from every dollar — without breaking a sweat.

Don't just rely on card perks alone — double up! Combine your credit card's special Black Friday promotions with platform vouchers, bank promo codes, and site-wide discounts. It's the best way to multiply your savings on big-ticket items.

Each card has its own set of terms, reward caps, and fine print. Before you start swiping, check if your card's bonus rewards have a monthly or category limit, and make sure your purchases actually qualify.

Shopping on Amazon, ASOS, or Taobao? Always pay with a card that charges no foreign transaction fees (like the UOB EVOL Card). You'll avoid hidden charges and get the real exchange rate.

Don't let flashy discounts fool you. Work out your total cost after factoring in cashback, site vouchers, and any fees, so you can be sure you're getting the lowest price.

It's easy to overspend in the rush. Use your bank or card app to set a budget or get notified when you're close to your limit-so you score the deals you want, without busting your wallet.

Black Friday is your chance to get more out of every dollar-but only if you're smart about which card you use. Before you start shopping, take a moment to check your cards, register early for bank promotions, and make sure you're stacking all the best deals.

[[nid:724928]]

This article was first published in MoneySmart.