'Can I afford it?' is only part of the big question when buying a first home

PHOTO: Stackedhomes

Or at least, a dangerously incomplete one. I get that it's intuitive; if you're a young first-time homebuyer, the first thoughts that float to mind are: Can I make the downpayment? Do I have enough in my CPF? Can I meet the Mortgage Servicing Ratio or Total Debt Servicing Ratio, and why is everything an alphabet soup of acronyms?

The good news is that when the home-hunting season starts after Chinese New Year, there will be a lot of options at many different price points. We have around 13,400 flats reaching MOP this year, and around 55,000 BTO flats that will be launched between last year and 2027. We're also seeing a return to (hopefully) more affordable properties in the Outside of Central Region (OCR) this year.

Chances are, most of you young, first-time homebuyers will find something affordable — either in the sense of qualifying for the loan, or a mortgage that doesn't result in premature hair loss. You'd have done better than me, in the latter case.

But having gone through this process myself — more than once now — I've come to realise "Can I afford it" is just one-half of the consideration. It feels like the responsible question to ask, but it skips over the issue of optionality. Affordability only tells you whether you can get in, but it tells you very little about what happens after you buy.

A more important question is this: If my life changes, can I change my housing decision without getting burnt?

Many young buyers today are doing well on paper. They have decent incomes, stable careers, and more or less have their first property locked in. But in the years that follow the first property purchase, some will realise serious issues creeping in.

The most common one I encounter — and which I've mentioned often — is that of singles who buy a private one-bedder instead of an HDB flat as their first home.

Subsequently, they meet the right person and want to settle down, but now find their shoebox unit is too small, and it's not always a simple matter to just sell and get an HDB flat. There is, for instance, no assurance that the market will be good at the time you need to sell, and a one-bedder is not the easiest property to market.

(P.S. There's also a 15-month waiting period to buy a resale flat after you liquidate a private property, and a 30-month wait for a BTO flat)

But there are other instances as well. I meet young homeowners who change their career or employer, and realise they can't move closer to work without paying much more. Some run into job cuts like we saw last year, and realise they can't downgrade without losing money.

In some cases, the results are a loss of opportunity. Just this week, for instance, I spoke to a 33-year-old first-time homeowner who got an offer for her dream job abroad. But this is just her second year of home ownership, and she can't take a career risk when the mortgage looms over her head.

Even if nothing goes 'wrong' per se, these homeowners feel trapped because there's suddenly very little room to change course in their lives.

Many homebuyers are prudent — it's not as if you can choose to overleverage anyway, with the many loan curbs the government has put in place. But just because a home is affordable now doesn't mean the home is still the right fit in 10 years' time; and life changes come quicker and more frequently in younger years.

When those changes come, initial affordability doesn't guarantee a painless exit. In fact, young first-time buyers often face the most asymmetric risks: they have less in the way of accrued savings, and they're often pushed to buy earlier. Waiting too long can push prices even further out of reach, so even prolonged rental isn't a great solution.

The end result is a demographic of buyers who are quietly pressured to commit early, commit heavily, and get it right the very first time.

For those who don't, the least-worst result is long commutes, but there are also lifestyle compromises, career decisions shaped around their mortgage instead of their opportunities, and even shattered relationships, depending on who they buy with. These aren't always dramatic failures, but they can be a source of long-term grinding stress.

I think the worst outcome is a property that forces an unhappy couple to stay together. We often talk about how Singaporeans are obsessed with acquiring a flat before marriage. Perhaps we should talk more about the dangers of a flat that keeps two people bound together, even if a relationship sours or turns abusive.

You can't change the property market, but you have a little more control over how you're exposed to its risks. The aim is not to look at just affordability, but at whether you're giving up future options.

Among your shortlisted homes, which ones have layouts that can adapt? A two-bedder may be able to house a small family for a time, even if it's a bit cramped, but not a one-bedder. A project that's in the OCR, where there are more schools and heartland conveniences, can cater to multiple buyer profiles and not just one niche. A good question to ask your property agent is:

"Who else would want this unit if I needed to sell or rent it?"

Perhaps most importantly, it's good to have the distinctly un-Singaporean trait of separating your housing from your self-worth. If you're buying just because it's a milestone and a proof of adulthood, you're more likely to overcommit and to end up enduring a bad fit for too long.

Don't think of affordability as just whether you can buy, but also whether you can back out later with minimal damage. That way your home will support your lifestyle, rather than define it.

Top 5 most expensive new sales (by project)

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | TENURE |

| CHUAN PARK | $4,067,600 | 1550 | $2,624 | 99 yrs (2024) |

| ONE MARINA GARDENS | $3,738,000 | 1238 | $3,020 | 99 yrs (2023) |

| AMBER HOUSE | $3,732,474 | 1216 | $3,069 | FH |

| NAVA GROVE | $3,670,000 | 1464 | $2,507 | 99 yrs (2024) |

| SPRINGLEAF RESIDENCE | $3,489,000 | 1475 | $2,366 | 99 yrs (2024) |

Top 5 cheapest new sales (by project)

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | TENURE |

| THE CONTINUUM | $1,428,000 | 560 | $2,551 | FH |

| OTTO PLACE | $1,442,000 | 872 | $1,654 | 99 yrs (2024) |

| BLOOMSBURY RESIDENCES | $1,716,000 | 678 | $2,530 | 99 yrs (2024) |

| HILLHAVEN | $1,748,000 | 700 | $2,498 | 99 yrs (2023) |

| CANBERRA CRESCENT RESIDENCES | $2,067,400 | 990 | $2,088 | 99 yrs (2024) |

Top 5 most expensive resale

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | TENURE |

| THE VERMONT ON CAIRNHILL | $9,050,000 | 6060 | $1,493 | FH |

| MARINA COLLECTION | $6,800,000 | 4725 | $1,439 | 99 yrs (2007) |

| GLOUCESTER MANSIONS | $5,100,000 | 3466 | $1,471 | FH |

| BAYSHORE PARK | $4,275,000 | 3800 | $1,125 | 99 yrs (1982) |

| PATERSON RESIDENCE | $4,220,000 | 1496 | $2,820 | FH |

Top 5 cheapest resale

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | TENURE |

| PAVILION SQUARE | $618,000 | 398 | $1,552 | FH |

| SUITES@CHANGI | $690,000 | 441 | $1,563 | FH |

| RIVERBANK @ FERNVALE | $750,000 | 495 | $1,515 | 99 yrs (2013) |

| GUILLEMARD SUITES | $800,888 | 635 | $1,261 | FH |

| THE WOODGROVE | $825,000 | 872 | $946 | 99 yrs (1996) |

Top 5 biggest winners

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | RETURNS | HOLDING PERIOD |

| CHARMING GARDEN | $3,400,000 | 1808 | $1,880 | $2,500,000 | 20 Years |

| THE SIXTH AVENUE RESIDENCES | $4,200,000 | 2605 | $1,612 | $2,007,140 | 19 Years |

| THE WINDSOR | $4,120,000 | 2454 | $1,679 | $1,752,000 | 14 Years |

| VALLEY PARK | $2,700,000 | 1216 | $2,220 | $1,650,000 | 27 Years |

| CASPIAN | $2,580,000 | 1593 | $1,620 | $1,559,790 | 17 Years |

Top 5 biggest losers

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | RETURNS | HOLDING PERIOD |

| MARINA COLLECTION | $6,800,000 | 4725 | $1,439 | -$3,524,600 | 16 Years |

| OUE TWIN PEAKS | $3,950,000 | 1604 | $2,463 | -$718,000 | 9 Years |

| MARINA ONE RESIDENCES | $2,315,000 | 1163 | $1,991 | -$285,000 | 7 Years |

| FOURTH AVENUE RESIDENCES | $1,030,000 | 484 | $2,126 | -$62,000 | 5 Years |

| GUILLEMARD SUITES | $800,888 | 635 | $1,261 | -$38,000 | 4 Years |

Top 5 biggest winners (ROI per cent)

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | ROI (per cent) | HOLDING PERIOD |

| CHARMING GARDEN | $3,400,000 | 1808 | $1,880 | 278 per cent | 20 Years |

| PALMWOODS | $1,080,000 | 850 | $1,270 | 195 per cent | 19 Years |

| PARC EMILY | $1,958,000 | 904 | $2,165 | 186 per cent | 20 Years |

| YISHUN SAPPHIRE | $1,368,000 | 1216 | $1,125 | 174 per cent | 21 Years |

| VALLEY PARK | $2,700,000 | 1216 | $2,220 | 157 per cent | 27 Years |

Top 5 biggest losers (ROI per cent)

| PROJECT NAME | PRICE | AREA (SQ FT) | $PSF | ROI (per cent) | HOLDING PERIOD |

| MARINA COLLECTION | $6,800,000 | 4725 | $1,439 | -34 per cent | 16 Years |

| OUE TWIN PEAKS | $3,950,000 | 1604 | $2,463 | -15 per cent | 9 Years |

| MARINA ONE RESIDENCES | $2,315,000 | 1163 | $1,991 | -11 per cent | 7 Years |

| FOURTH AVENUE RESIDENCES | $1,030,000 | 484 | $2,126 | -6 per cent | 5 Years |

| GUILLEMARD SUITES | $800,888 | 635 | $1,261 | -5 per cent | 4 Years |

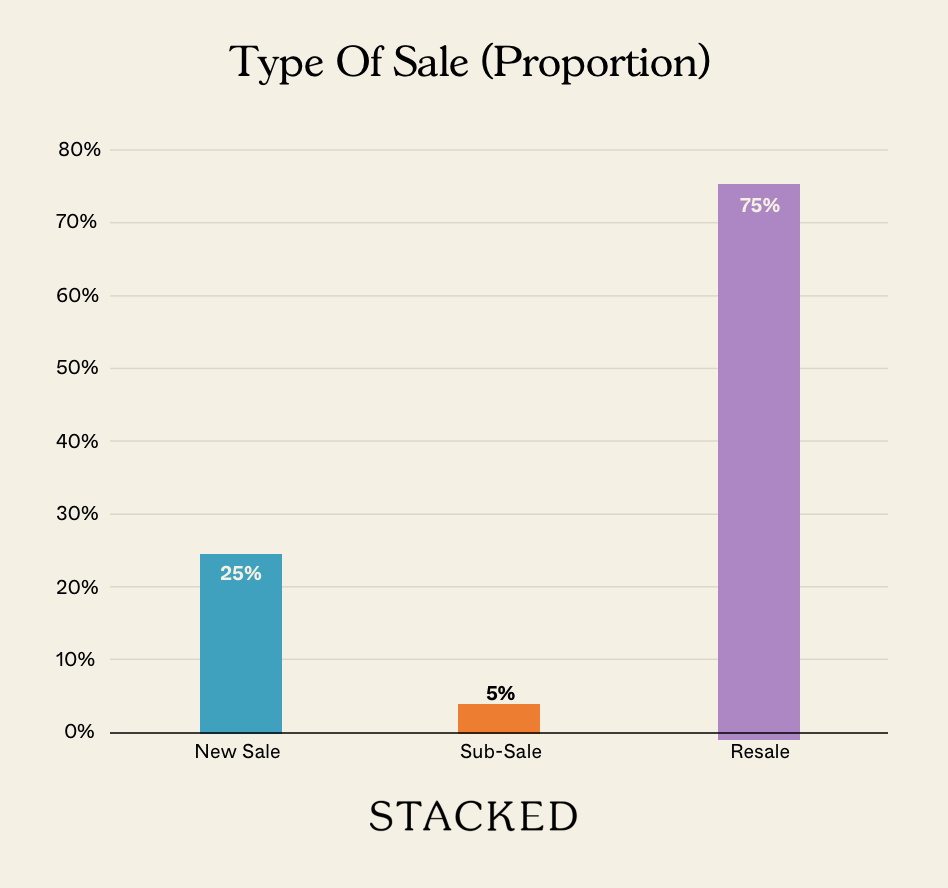

Transaction breakdown

[[nid:727822]]

This article was first published in Stackedhomes.