We've saved about $1 million in cash and CPF and own 2 condos - should we sell both or rent out for now?

Should you purchase a home at Palm Oasis?

PHOTO: Stackedhomes

Good Day Team,

We have always read your content with interest which are helpful for the common folks.

As such we will like to share our situation and appreciate your advice on what is the next best option.

We are a family of four, my Partner and myself are mid-30s and the little ones are five and newborn with a helper.

Our household income comprises of:

Party A: approx 200k p.a. and Party B: approx 50k p.a.

Property under Party A: Freehold boutique small duplex Penthouse 3.5 bedder apartment at D15, current est value about 1.7m to 1.9m. Outstanding mortgage about 1m.

Property under Party B: 99 years leasehold condo, about 89 years balance lease, two bedder at D18, current est value about 0.9m to 1m. Outstanding mortgage of about 0.5m.

Liquid cash + OA available at the moment is approx. 0.9m to 1m.

Currently we have not rented out any of our properties. Both properties have a couple of primary school options within the <1km and 1km to 2km range.

We seek your advice on what is the best possible option for us given our situation.

Should we sell both properties or one of them and rent for the time being?

Given the above information, I am not certain what is our budget and what kind/type of property should we target moving forward, appreciate recommendations.

1. 99 years LH is waterview / FH is Palm Oasis.

2. Cpf usage 50k for waterview / 300k for Palm Oasis.

Look forward to your input and insight.

Cheers

Hey there,

Thanks for writing in and we're happy to hear our content has been helpful to you!

Owning two properties is the Singaporean dream (for most) but many a time after achieving this milestone, the big question on buyers' minds is "What's next?". We understand it can be overwhelming when you do a search online and are faced with the multitude of information and options out there.

That said, you are also in quite a healthy position and frankly, at this point, you could very well not do anything at all. We aren't sure why you've not rented out your properties yet given the high rental rates at the moment but will assume the plan would be to move into the bigger one for your own stay, and the smaller place to be rented out for income.

But if you do feel you made a mistake buying either (perhaps you have different needs for your own stay, or you would like to sell and acquire possibly better-performing properties), then in that case let's see if you do have a case to do so.

In this article, we'll run through the following pointers which hopefully, will give you a clearer idea of how best to move forward:

| Description | Amount |

| Sale price | Assuming $900,000 |

| Outstanding loan | $500,000 |

| CPF used plus accrued interest | $50,000 |

| Cash proceeds | $350,000 |

| Description | Amount |

| Sale price | Assuming $1,700,000 |

| Outstanding loan | $1,000,000 |

| CPF used plus accrued interest | $300,000 |

| Cash proceeds | $400,000 |

As we do not know the exact breakdown for the $0.9 to 1M liquid cash + CPF, we will assume $500,000 to be cash and $250,000 each in CPF. We will set aside the $500,000 cash as emergency funds and will not include that in the following calculations.

| Description | Amount |

| Maximum loan based on fixed monthly income of $16,000 and age 35 | $1,843,259 (30 years tenure) |

| CPF funds | $550,000 |

| Cash | $400,000 |

| Total loan + CPF funds + Cash | $2,793,259 |

| BSD based on $2,793,259 | $109,263 |

| Estimated affordability | $2,683,996 |

| Description | Amount |

| Maximum loan based on fixed monthly income of $4,100 and age 35 | $472,335 (30 years tenure) |

| CPF funds | $300,000 |

| Cash | $350,000 |

| Total loan + CPF funds + Cash | $1,122,335 |

| BSD based on $1,122,335 | $29,493 |

| Estimated affordability | $1,092,842 |

Now that we have a better sense of the numbers, let's take a look at how the two projects are performing!

Waterview is a 99-year leasehold development located in District 18. It is a mid-sized project with 696 units of two to four bedroom types. It obtained its Top in 2014 while its lease started in 2010, making it 13 years old.

These are some of the recent two-bedroom transactions:

| Date | Size (sq ft) | No. of bedrooms | PSF | Price | Level |

| Jan 2023 | 786 | Two | $1,171 | $920,000 | #11 |

| Dec 2022 | 786 | Two | $1,171 | $920,000 | #14 |

| Nov 2022 | 926 | Two | $1,067 | $988,000 | #02 |

| Nov 2022 | 926 | Two | $1,262 | $1,168,000 | #13 |

| Oct 2022 | 926 | Two | $1,132 | $1,048,000 | #10 |

| Oct 2022 | 786 | Two | $1,120 | $880,000 | #02 |

| Oct 2022 | 786 | Two | $1,145 | $900,000 | #08 |

Source: Edgeprop

And two-bedroom rental transactions:

| Date | Size (sqft) | Monthly rent | No. of bedrooms |

| Dec 2022 | 700 to 800 | $3,000 | Two |

| Dec 2022 | 900 to 1,000 | $3,300 | Two |

| Dec 2022 | 900 to 1,000 | $3,200 | Two |

| Dec 2022 | 900 to 1,000 | $4,200 | Two |

| Dec 2022 | 900 to 1,000 | $4,400 | Two |

| Dec 2022 | 700 to 800 | $3,950 | Two |

| Dec 2022 | 1,100 to 1,200 | $5,500 | Two |

| Dec 2022 | 1,100 to 1,200 | $5,000 | Two |

| Nov 2022 | 700 to 800 | $3,550 | Two |

| Nov 2022 | 900 to 1,000 | $3,600 | Two |

Source: Edgeprop

We will assume you own the smaller two bedder which is 786 sq ft. The average rent for a 786 sq ft two-bedroom unit in Q42022 is $3,172 while the average price for a unit of the same size is $900,000, so the rental yield comes up to around 4.23 per cent.

| Year | Waterview | Singapore’s average resale PSF (99-year leasehold projects) |

| 2014 | $1,113 | $1,451 |

| 2015 | $1,089 | $1,250 |

| 2016 | $1,034 | $1,243 |

| 2017 | $1,029 | $1,154 |

| 2018 | $1,054 | $1,253 |

| 2019 | $1,051 | $1,369 |

| 2020 | $1,009 | $1,519 |

| 2021 | $1,048 | $1,393 |

| 2022 | $1,125 | $1,466 |

| 2023 | $1,171 | $1,601 |

| Annualised | 0.56 per cent | 1.10 per cent |

We can see from the chart above that since 2018, prices at Waterview have been moving in line with the overall resale market for 99-year leasehold projects.

Its annualised returns look poorer for Waterview considering its high start point in 2014. However, if we focus on recent years, it's actually performing really well:

| Year | Waterview | Singapore |

| 2020 | $1,009 | $1,519 |

| 2021 | $1,048 | $1,393 |

| 2022 | $1,125 | $1,466 |

| 2023 | $1,171 | $1,601 |

| Annualised | 5.07 per cent | 1.78 per cent |

While Tampines has a lot of private condominium supply, there's also an ample number of HDB dwellers and potentially upgraders who wish to stay in the same estate. This gives Waterview and its neighbouring condos some price support.

Palm Oasis is a freehold project located in District 15. It is a low-rise boutique development with 56 units of two and three bedders and it obtained its TOP in 2008.

These are some of the recent three-bedroom transactions:

| Date | Size (sqft) | No. of bedrooms | PSF | Price | Level |

| Nov 2022 | 1,421 | Three | $1,042 | $1,480,000 | #05 |

| Aug 2022 | 1,421 | Three | $1,091 | $1,550,000 | #05 |

Source: Edgeprop

And three bedroom rental transactions:

| Date | Size (sqft) | Monthly rent | No. of bedrooms |

| Nov 2022 | 1,400 to 1,500 | $5,500 | Three |

| Jul 2022 | 1,400 to 1,500 | $4,400 | Three |

| Feb 2022 | 1,400 to 1,500 | $3,000 | Three |

Source: Edgeprop

Based on the single sale and rental transaction in Q42022 at $1,480,000 and $5,500 respectively, the rental yield comes up to 4.46 per cent.

As this is only based on one transaction, do note that it may not be the most conclusive.

| Year | Palm Oasis | Singapore’s average resale PSF (Freehold/999-year) |

| 2016 | $840 | $1,322 |

| 2017 | $799 | $1,381 |

| 2018 | No Data | $1,427 |

| 2019 | No Data | $1,387 |

| 2020 | No Data | $1,388 |

| 2021 | $1,079 | $1,606 |

| 2022 | $1,067 | $1,655 |

| Annualised | 4.07 per cent | 3.82 per cent |

From the table above, we can see that the three-bedroom at Palm Oasis has performed close to the average performance in Singapore for freehold/999-year leasehold properties of similar sizes.

We must caution that boutique developments typically have a lower transaction volume which could result in their prices being less accurate. In this case, we saw no transactions between 2018 to 2020, and transactions can often be misrepresentations of the underlying fundamentals given the low volume.

In addition, a lower turnover rate also generally leads to a slower growth rate since banks will typically value a property based on its recent transactions.

In terms of rental yield, both properties are almost on par, but if we were to look at their growth rates, Waterview is definitely more consistent given its larger supply.

While the development has done quite decently in the past few years, we must keep in mind the issue of lease decay given it is a 99-year leasehold development.

Seeing that the current rental yield is pretty decent, you could rent it out and use the rental to offset your monthly mortgage.

As for Palm Oasis, we think that the development poses some challenges in terms of capital appreciation.

While it is freehold and hence its land value is protected, the development doesn't really stand out.

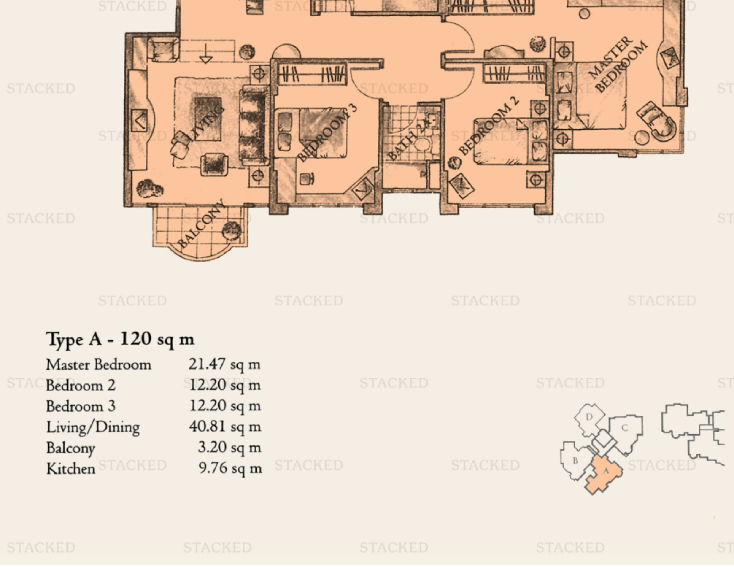

The development is situated in a sea of other freehold developments. Moreover, its layout is less than desired. While we don't have the exact 1,421 sq ft layout to show, here's what the three-bedroom 1,431 sq ft layout looks like:

A lot of the space goes towards the open roof terrace and balcony, something which isn't very utilised and is a more niche lifestyle product — so you will face a smaller pool of buyers when it comes to selling.

The living room is also not very wide for a three bedder. Even the dining area shows that it can only fit a four-seater which is usually too small for a three-bedroom unit.

As such, even though it also has a decent rental yield, we think that there are better opportunities for capital appreciation if invested in another project.

In light of the fact you're currently sitting on potential cash proceeds of around $400,000, it might be a wise move to cash out and purchase something else with a better appreciation potential.

With a family of four and a helper, we are assuming you are staying in the Palm Oasis unit since it has three bedrooms. We will not suggest selling both properties at the same time and renting a place, especially in the current market where rental prices are on an upswing.

It is also a better option to own two properties, so you keep the investment and own stay separate, rather than selling both properties to purchase one.

If Party A were to sell Palm Oasis, your affordability for the next property would be at $2.68m which will open up your options to a considerable number of developments.

In the best-case scenario, you'll be able to find a suitable place soon after you've secured a buyer so there is no need to move twice. But in the event you are not able to find something you like as quickly, you could move into the Waterview unit although it will be rather cramped for five people.

Currently, the most affordable unit for rent on the market is $3,200 for a four-room HDB. With the high demand, landlords are most likely looking at a one-year lease minimally. Renting a unit at $3,200 for a year would add up to $38,400 which is pretty substantial.

While it might not be the most ideal living situation for five people to stay in a two-bedroom unit, your children are still fairly young and you probably will not need a year to find a suitable place.

As for Waterview, since prices are likely to hold for the short to medium term, you can take advantage of the current rental market and rent it out for the next few years before swapping it for another development with better appreciation potential.

Seeing as both the developments you currently own are located in the East, we presume your family prefers to live in that area so we've picked out a project in the east that might be suitable for you.

The Makena is a freehold development situated in District 15 that obtained its Top in 1998. It is a mid-sized project made up of 504 units of two to four bedroom types and sits on a huge 34,000 sqm plot of land.

Older developments tend to have more spacious units and given its large land size, the blocks are well spread out.

As you're a family of four with a helper, we will be looking for units with at least three bedrooms and a utility.

These are some of the recent three-bedroom transactions:

| Date | Size (sqft) | No. of bedrooms | PSF | Price | Level |

| Nov 2022 | 1,518 | Three | $1,802 | $2,735,000 | #15 |

| Nov 2022 | 1,292 | Three | $1,935 | $2,500,000 | #13 |

| Oct 2022 | 1,615 | Three | $1,858 | $3,000,000 | #17 |

Source: Edgeprop

With a budget of $2.68m, we will likely be looking at the smaller three bedders which are still considerably well sized at 1,292 sq ft and they also come with a utility room.

The three bedders at The Makena come in several sizes and floor plans. Their layouts are generally efficient but due to the shape of the building, some units have odd corners. This particular one is regularly shaped which provides ease of furniture placement.

The living area is sunken which creates an illusion of space and is also a nice segregation from the dining room. All three bedrooms are of a good size and can comfortably fit a double bed with ample space to move around.

There is also a yard attached to the kitchen which is great for doing laundry rather than having to do it on the balcony which some may find unsightly.

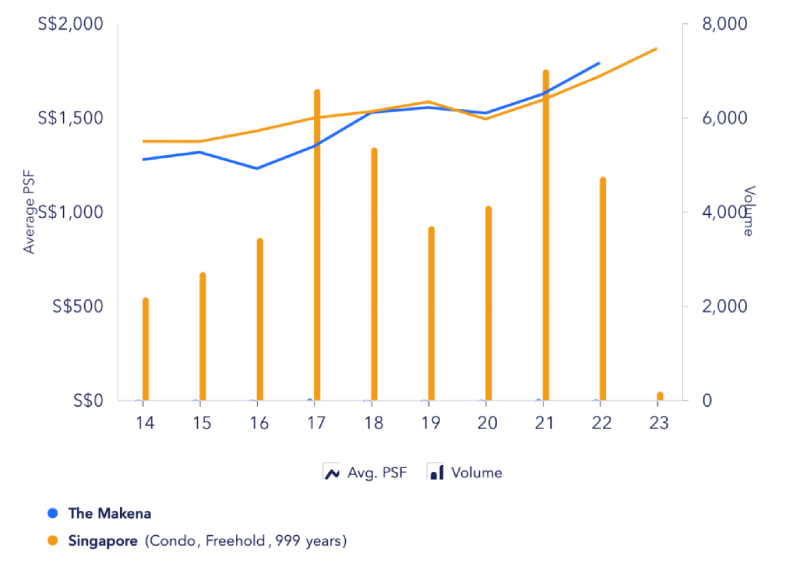

| Year | The Makena | Singapore’s average resale PSF (Freehold & 999-year leasehold projects) |

| 2014 | $1,277 | $1,366 |

| 2015 | $1,316 | $1,365 |

| 2016 | $1,223 | $1,396 |

| 2017 | $1,350 | $1,466 |

| 2018 | $1,527 | $1,543 |

| 2019 | $1,558 | $1,575 |

| 2020 | $1,525 | $1,504 |

| 2021 | $1,625 | $1,592 |

| 2022 | $1,790 | $1,715 |

| Annualised | 4.31 per cent | 1.65 per cent |

The drop in average PSF for The Makena in 2016 is due to two particular transactions that changed hands at a much lower PSF of $1,0xx.

Besides this one odd year, prices at The Makena are moving in line with the overall market for freehold and 999-year leasehold developments. In terms of annualised returns over the last eight years, it has actually outperformed the overall market by 2.66 per cent.

In land-scarce Singapore, there are not many developments that sit on such a huge land plot and are not densely populated. A huge land plot also translates to a higher land value especially one that is freehold.

On top of that, the upcoming Tanjong Katong MRT station will increase connectivity of the project so we believe demand for The Makena will continue to hold up even in the long run.

As mentioned at the beginning, you are in a spot where even if you decide not to do anything, it's not going to be detrimental.

[[nid:545843]]

But, for example, if the layout at Palm Oasis is not making too much sense for your family and you are looking to explore if there are better options, then yes, there are.

Looking at the performances of both developments, it may make sense to cash out from Palm Oasis while it's a positive sale, seeing as the chances of realising a significant capital appreciation even in the long run is not high.

However, we will not advise selling both properties at the same time and renting somewhere else given the high rental rates now. You should probably look to sell Palm Oasis and rent out Waterview.

If the timeline is planned well with the sale of Palm Oasis and the purchase of your next property going smoothly, you will save the trouble of having to move twice.

But in the event finding a place you like takes longer than planned, you have the option to temporarily move into the unit at Waterview.

This article was first published in Stackedhomes.