Bank stocks in Singapore are likely to survive this recession

PHOTO: Pexels

Bank stocks in Singapore have been massively sold down. However, I think they are well-positioned to ride out the recession. Here’s why.

With a recession looming, it is no surprise that bank stocks in Singapore have been massively sold down. Besides the Covid-19 pandemic halting businesses around the globe, lower interest rates and the plunge in oil prices could also hurt banks.

Despite this, I think the three major banks in Singapore are more than able to weather the storm. Here’s why.

First of all, DBS Group Holdings (SGX: D05), Oversea-Chinese Banking Corp (SGX: O39) and United Overseas Bank (SGX: U11) are each very well capitalised.

A good metric to gauge this is the Common Equity Tier-1 ratio (CET-1 ratio). This measures a bank’s Tier-1 capital – which consists of common equity, disclosed reserves, and non-redeemable preferred stock – against its risk-weighted assets (i.e. its loan book).

The higher the CET-1 ratio, the better the financial position the bank is in. In Singapore, banks are required to maintain a CET-1 ratio of at least 6.5per cent.

As of Dec 31, 2019, DBS, OCBC, and UOB had CET-1 ratios of 14.1per cent, 14.9per cent, and 14.3per cent respectively. All three banks had CET-1 ratios that were more than double the regulatory requirement in Singapore.

This suggests that each bank has the financial strength to ride out the ongoing stresses in Singapore and the global economy.

In a recent interview with Euromoney, DBS CEO Piyush Gupta “noted that years of Basel reforms have left banks with ‘enormous capital reserves’ and a clear protocol: to dip first into buffers, then counter-cyclical buffers and finally into capital reserves.”

The trio of banks also have well-diversified loan portfolios.

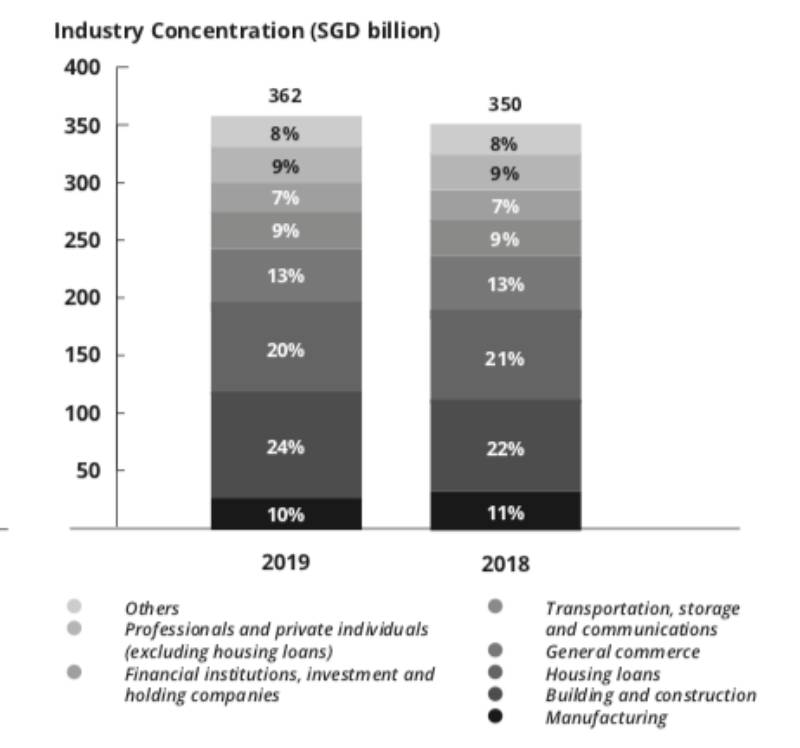

For instance, the chart below shows DBS’s gross loans and advances to customers based on MAS industry code.

From the chart, we can see that building and construction and housing loans make up the bulk of the loan book. While the 22per cent exposure to building and construction could be seen as risky, I think it is still manageable considering that the loan portfolio is well-spread across the other industries.

Similarly, UOB’s and OCBC’s largest exposure was to the building and construction sector at around 25 per cent and 24per cent of their total loan portfolio respectively. Though there is an element of risk, the loan portfolios at the three banks are sufficiently diversified in my opinion.

I think the big question on investors’ minds is whether the trio of banks will cut their dividend. We’ve seen some banks around the globe slash their dividends amid the crisis to shore up their balance sheet.

[[nid:480006]]

Regulatory bodies in some other countries have even stepped in to prevent some banks from paying a dividend in order to ensure that the banks have sufficient capital to ride out the current slump.

However, based on what DBS’s CEO said in the interview with Euromoney, it seems unlikely that DBS will cut its dividend in the coming quarters. The bank is sufficiently capitalised and can continue to pay its regular dividend without stretching its balance sheet.

Gupta elaborated: “If there is a multi-year problem… banks will likely get to the point where they can’t pay dividends. But promising now to not pay them is, to me, illogical.”

I think besides DBS, both UOB and OCBC also have sufficient capital to keep dishing out their dividends too. Both have high CET-1 ratios, as I mentioned earlier, and similar dividend payout ratios to DBS.

Banks in Singapore are going to be hit hard by Covid-19. There’s no sugarcoating that.

We have seen banks in the US increase their allowances for non-performing loans in the first quarter of 2020 and they expect to do so again in the coming quarters. If the US banks are anything to go by, we can expect a similar situation in Singapore, with bank earnings being slashed.

However, all three major local banks still have strong balance sheets and diversified loan portfolios. So, despite the near-term headwinds, I think that the three banks will ultimately be able to ride out the recession.

For the latest updates on the coronavirus, visit here.

This article was first published in The Good Investors. All content is displayed for general information purposes only and does not constitute professional financial advice.