A beginner's step-by-step guide: How to buy a HDB resale flat without an agent and save on fees

PHOTO: Unsplash

Sometime last year, my family and I moved house from an HDB resale flat in the Northeast to an HDB flat that was more central. Just as we were about to engage a property agent for our HDB flat purchase, I met a friend of mine and told him about our plans to do so.

This was a turning point, as my friend strongly advised us to buy an HDB flat without an agent and save on the one per cent commission when you engage a property agent to buy a flat.

Although one per cent may not seem a lot, hear me out.

To get an idea of how much you can save, I took the average of the median prices for four-room HDB-flat in all the towns for Q2 2020. The value I arrived at is $466,154, which means that you will save about $4,661.54 in property agent commission fees.

Imagine, this money can be used to renovate your home and build a mini cinema room in your house. Intrigued by his proposition, I went back to research the whole process and found that I was not alone.

According to HDB, there have been a rising number of people engaging in Do-it-yourself (DIY) resale transactions or buying and selling their HDB without property agents.

From 2010 to 2018, the percentage of DIY resale transactions more than tripled, growing from 11 to 28 per cent.

This upward trend will likely continue, as the revamped HDB Resale Portal has cut down the time for resale transactions by half to about eight weeks, and has made it easier for those who are engaging in DIY resale transactions as well.

However, fair warning, you will have to put in a lot of time and energy into this whole process. If you are still not deterred, here is a beginner-friendly step-by-step guide to buying an HDB resale flat without a property agent!

When it comes to commissions for property agents, The Council for Estate Agencies (CEA) Singapore does not really regulate or set guidelines for commission rates. This is done to allow the market to drive competitive pricing in the industry.

The fee that you pay property agents is a percentage of the transaction price of the flat for their services.

For HDB resale flats, the seller usually pays about two per cent in commission to the agent while the buyer pays about one per cent.

When you decide to forgo a property agent, you will have to do without these services that a good property agent provides.

Financial Planning Advisory: Property agents will consult your finances and advise you on what kind of flat you can afford. (P.S. you can also check out this Property Affordability Calculator .)

Information Advantage: Researchers at the Singapore Management University have found that “agent buyers have more information advantages in a less informative environment, and high ability agent buyers have even more information advantages.” In other words, they can help you find a ‘diamond in the rough’ based on the criteria that you set.

Comparative Market Analysis (CMA): They will help you do CMA on the shortlisted properties so that you get the best price.

Conduct Background Checks on Property/Seller: They will check to see if the property or the seller is up to scratch and look out for things like signs of unlicensed moneylenders harassment.

[[nid:501162]]

Defect Checks: They will help you check if there are any potentially costly defects in the units you are interested in.

Price Negotiation: They will help you negotiate with the seller or the seller agents representing the seller for a better offer.

Paperwork: The buying process can be a bit complex as you have to sort through all the legalese for the legally binding contracts and make sure everything is in place. A good agent will do the paperwork right for you.

If you are willing to put in the time and energy and are confident enough to be able to do the above-mentioned things, you can save quite a bit by not hiring a property agent for your HDB flat purchase.

Without further ado, let’s dive into the process!

Your journey to buying an HDB resale flat without a wizened property agent’s help starts with you registering an Intent to Buy on the HDB Resale Portal.

Do note that if you are purchasing the flat together with other applicants like your family or partner, only one of you needs to register. Also, no one else can register on your behalf, so you will need to register yourself.

Applicant(s) need to fulfil the following criteria:

But, the most straightforward way to check this is to register for the Intent to Buy. Once registration is complete, you can see if you are eligible to buy an HDB resale flat, which grants you can get, or whether you can apply for an HDB concessionary housing loan.

Your registered Intent to Buy is valid for only 12 months. Once it expires, you will need to re-apply again.

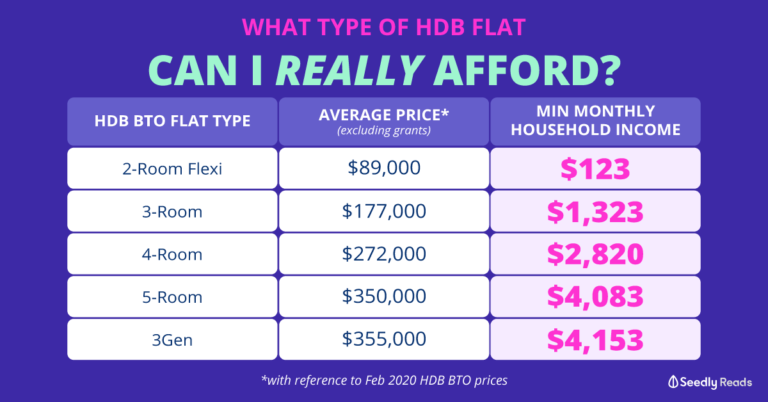

The next step will be to figure out what kind of HDB flat you can really afford and budget from there.

You can conduct this simple exercise as outlined in our article: What Type of HDB Flat Can I Really Afford?

For this exercise, I determined what is the minimum average monthly household income needed when considering what type of HDB flat to get.

Note: this price and income range is ONLY a guide, a flat in a mature estate is obviously going to cost more.

Feel free to apply my calculations to your respective BTO or Resale flat purchase to see which type of HDB flat you can comfortably afford.

You will also need to consider:

Once you have nailed down your budget, you can start looking for the flat of your dreams. You can find property listings from the numerous online property portals like:

Also, the best part about buying a resale flat (compared to a BTO flat) is the freedom. You can choose from any flat on the island — within your budget of course.

For example, you might want to get a house near your parents which also entitles you to the HDB Proximity Housing Grant (PHG) (up to $30,000).

You will also need to check if there are any EIP or SIP restrictions on the flat in the block you are considering. You can use this tool from HDB to check this.

CPF usage and HDB loans will be pro-rated based on whether the property’s remaining lease can cover the youngest buyer till age 95. Buyers who purchase a home for life will face lesser restrictions on their CPF usage

The amount of CPF that can be used depends on whether the remaining lease can cover the youngest buyer until age 95:

| Remaining Lease Of Property At Least 20 Years & Can Cover Youngest Buyer Till Age Of 95 | Use Of CPF |

|---|---|

| Yes | Maximum allowed Up to VL |

| No | Maximum allowed will be pro-rated based on extent the remaining lease of property can cover the youngest buyer until age 95 |

This change will help buyers set aside CPF savings for their housing needs during retirement (e.g. a replacement property).

With the update, NO CPF can be used if the property’s remaining lease is less than 20 years .

The updated rules will apply to any HDB flat applications and CPF withdrawal applications received on or after May 10, 2019.

For this step, your time will be spent doing property viewings.

When inspecting the resale flat you will need to look out for things like:

You will also need to inform your seller that you are not represented by an agent.

Generally, the price you see on Singapore property listings are negotiable, so do not be afraid to bargain.

Once you and the seller agree on the price, you can make an offer to the seller who will offer you an Option to Purchase (OTP).

The OTP is a legally binding contract between you and the seller which guarantees your right to purchase the HDB flat at the agreed-upon price. For the next 21 days, the seller cannot sell the unit to anyone else.

You can then proceed to sign the Option to Purchase (OTP) which should already be printed out by the seller.

You will also need to pay the option fee to ‘book’ the flat. The option fee can range from $1 to $1,000 (also negotiable).

Do note that once you have paid the option fee, you are obliged to exercise the OTP within 21 days as the option fee is forfeited if the OTP is not exercised.

If you do not exercise the OTP the seller is free to sell the flat to anyone else after 21 days.

The next step would be to submit a request for value of the flat you are buying online on the HDB Resale Portal. You should do this one working day after the Option Date (found on the OTP).

Do note that the whole home valuation process will take five to seven working days after submitting the Request For Value.

Once the valuation is out, take a moment to go through the HDB resale checklist. You can use it for your own planning but you need not submit it before you exercise the OTP.

The next step would be to sign on the OTP and pay the exercise fee which should not be more than $5,000 (includes option fee) .

The next step is for both parties to submit their part of the resale application to HDB.

This is a contractual agreement between you and the seller. The timeframe can be extended with mutual consent. A vital thing to note is that once either party has submitted the first portion of the resale application, the other party needs to send the corresponding portion within seven calendar days.

If this is not done, the application will expire and you will need to start over with the whole application process.

You are almost there!

Once both flat seller and buyer have submitted their resale applications, HDB will start processing the whole application. If everything is in order, HDB will then inform both seller and buyer by SMS and/or emails within 10 working days. You can also check the application progress status on the HDB Resale Portal.

This transaction will be completed about eight weeks after HDB’s acceptance of the resale application.

Within these eight weeks, both parties will need to endorse all documents prepared by HDB via the HDB Resale Portal and settle all the necessary fees online,

[[nid:499262]]

You will also need to arrange for a final inspection of the flat. Once the documents have been endorsed, an in-principle approval for the resale will be granted.

After this, HDB will arrange for a Resale Completion Appointment at the HDB Hub . Both sellers and buyers will need to physically attend to complete the resale transaction.

*If you have engaged private solicitors, your solicitor representative can attend the resale completion appointment on your behalf.

The seller will then handover the keys to the flat. And there you have it, you have successfully bought an HDB flat all by yourself. Congratulations!

This article was first published in Seedly.