Best fuss-free savings accounts with no conditions in Singapore 2021

PHOTO: The Straits Times file

We’ve previously seen the best saving accounts for working adults.

Most of them come with different requirements, including salary crediting or credit card spend.

But what if you’re just looking for a zero-effort, fuss-free savings account without having to consider the 1,001 conditions to fulfil?

Which might be something you’re looking for if you’re self-employed or a freelancer.

Or you just have extra cash and not knowing where to park it (like your emergency funds )…

And so this article is for those who are looking for something that is simple and straightforward.

In short, we are considering savings accounts with better interest rates that would beat the usual 0.05per cent p.a. with no complicated requirements.

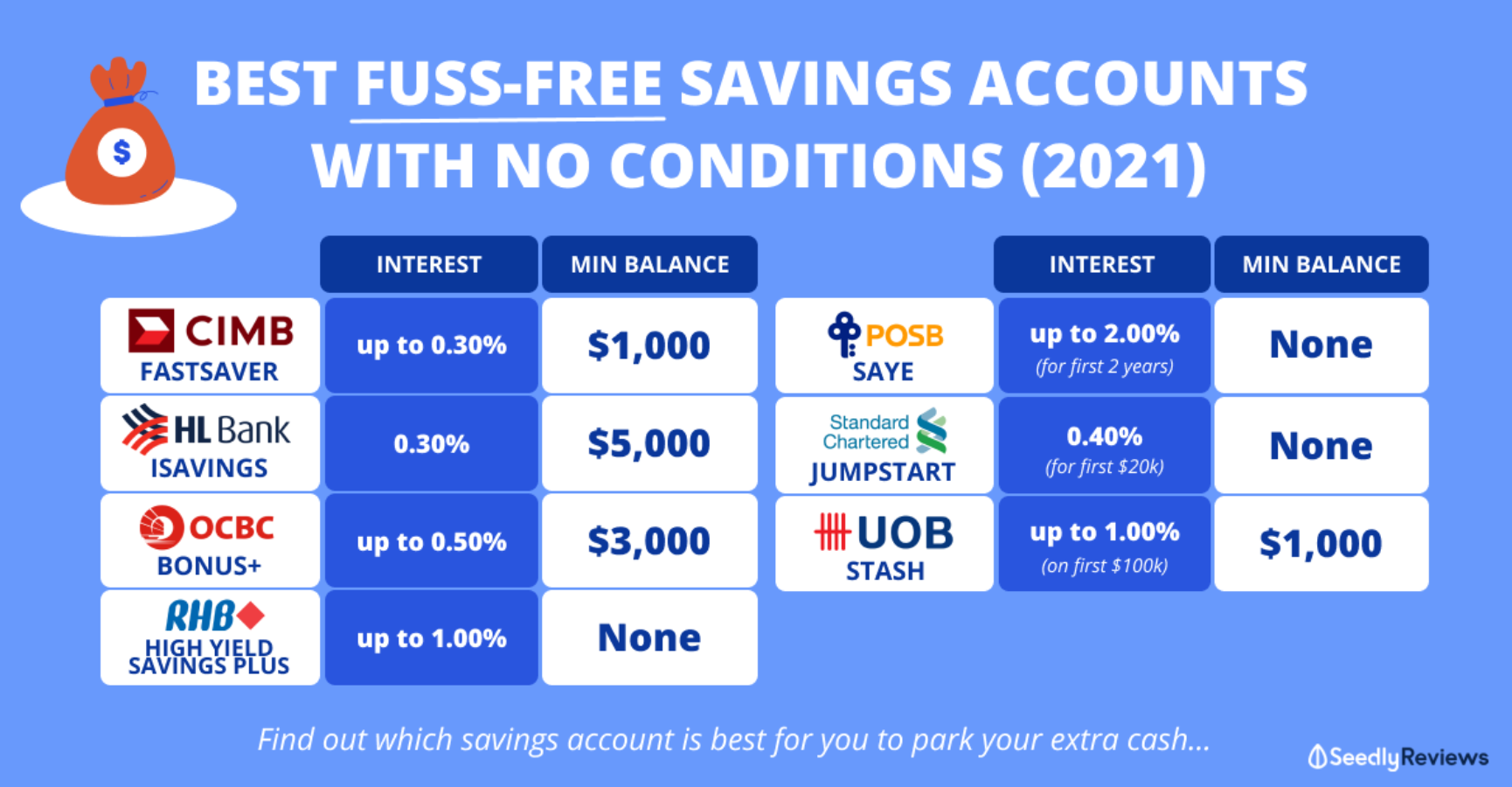

In order to find the best savings account, we assume that we are looking to park $20,000 into the savings account.

Based on this criterion that we set out, here’s how much interest you’ll be getting:

| Savings Account | Interest Earned |

|---|---|

| CIMB FastSaver | 0.30 per cent p.a. |

| HL Bank iSavings | 0.30 per cent p.a. |

| OCBC Bonus+ | Up to 0.40 per cent p.a. |

| POSB SAYE | 2.00 per cent p.a. |

| RHB High Yield Savings Plus | 0.8 per cent p.a. |

| Standard Chartered Jumpstart | 0.40 per cent p.a. |

| UOB Stash | Up to 0.30 per cent p.a. |

If you find that everything’s too much work…

You can use the FREE Seedly Savings Account Calculator to help you make your decision faster!

The whole process of choosing the best savings account can be rather confusing as we all have different spending habits and incomes.

To make it easier for you, we created the Seedly Savings Account Calculator which you can use for FREE !

All you have to do is fill up some basic information like your:

And the calculator will tell you which savings account gives you the highest interest rate!

If you’re still unsure, you can also read real user reviews left by on Seedly to find out if it’s really the best savings account for you!

| Account Balance | Interest Rates (Before Jan 15, 2020) |

Interest Rates (After Jan 15, 2020) |

|---|---|---|

| First $50,000 | 0.30 per cent p.a. | 0.30 per cent p.a. |

| Next $25,000 | 0.50 per cent p.a. | 0.30 per cent p.a. |

| Next $25,000 | 0.75 per cent p.a. | 0.15 per cent p.a. |

| Above $100,000 | 0.30 per cent p.a. | 0.15 per cent p.a. |

CIMB FastSaver has long been one of the favourites when it comes to a fuss-free savings account.

Especially before the reduction of interest rates, where we could earn 1 per cent p.a. for the first $50,000.

With the latest change with effect from 15 Jan 2021, individuals can earn up to 0.30 per cent for the first $50,000.

While the interest rates have fallen, it remains as one of the better savings accounts out there with no conditions.

| Account Balance | Interest Rates (p.a.) |

|---|---|

| First S$20,000 | 0.30 per cent |

| Next S$30,000 | 0.30 per cent |

| Next S$150,000 | 0.30 per cent |

| Next S$800,000 | 0.30 per cent |

| Above S$1,000,000 | 0.30 per cent |

Similar to CIMB FastSaver, get to earn 0.30 per cent p.a. for up to $1,000,000.

They are currently running a promotion till Jan 31, 2021, where individuals will get bonus interest rates on top of the prevailing rates, as follows:

| Account Balance | Interest Rates (p.a.) | Bonus Rates (p.a.) | Promo Rates (p.a.) |

|---|---|---|---|

| First S$20,000 | 0.30 per cent | 0.38 per cent | 0.68 per cent |

| Next S$30,000 | 0.30 per cent | 0.38 per cent | 0.68 per cent |

| Next S$150,000 | 0.30 per cent | 0.38 per cent | 0.68 per cent |

| Next S$800,000 | 0.30 per cent | 0.15 per cent | 0.45 per cent |

| Above S$1,000,000 | 0.30 per cent | 0.15 per cent | 0.45 per cent |

This means getting 0.68 per cent for the first $150,000, which is a pretty good rate for something that requires zero effort.

| OCBC Bonus+ Account | Interest Rates (p.a.) |

|---|---|

| Base interest | 0.05 per cent |

| No-withdrawal bonus interest | 0.10 per cent |

| No-withdrawal & Save bonus interest | 0.25 per cent |

| Total | Up to 0.40 per cent |

For OCBC Bonus+, there are two types of bonus interest if you meet the eligibility criteria:

Get up to 0.40per cent p.a. if these two conditions are fulfilled.

| Account Balance | Interest Rates (p.a.) |

|---|---|

| First $50,000 | 0.80 per cent |

| Next $25,000 | 0.90 per cent |

| Next $25,000 | 1.00 per cent |

| Above $100,000 | 0.40 per cent |

Earn up to 1.00 per cent p.a. for your first $100,000 with the RHB High Yield Savings Plus account.

Even if you don’t have $100,000, 0.8 per cent p.a. for the first $50,000 is a great deal as well.

The Standard Chartered Jumpstart account is another hot favourite when it used to give 2.00 per cent p.a. interest on the first $20,000 in the account.

Since Jan 1, 2021, this has been slashed to 0.4 per cent p.a. interest on balances up to $20,000 year-round.

And any incremental balances above $20,000 will receive 0.1 per cent p.a ..

The only catch? You need to be between 18 and 26 years old .

| Account Balance | Base Interest (p.a.) | Bonus Interest (p.a.) | Interest Rates (p.a.) |

|---|---|---|---|

| First $10,000 | 0.05per cent | 0.00 per cent | 0.05 per cent |

| Next $30,000 | 0.25 per cent | 0.30 per cent | |

| Next $30,000 | 0.55 per cent | 0.60 per cent | |

| Next $30,000 | 0.95 per cent | 1.00 per cent | |

| Above 100,000 | 0.00 per cent | 0.05 per cent |

Get up to 1.00 per cent p.a . for the first $100,000, given that the monthly average balance in the account is maintained or increased.

This means that withdrawals are allowed for this account, but have to be topped up again (to minimally the previous month’s balance, or more) to earn the bonus interest.

Do note that there is no bonus interest for the first $10,000.

In a low-interest-rate environment, most of the banks are probably affected which resulted in the changes to their consumer products.

With different banks cutting their interest rates every few months, it gets difficult to keep up with the ones that are offering the highest rates.

If you’re choosing to open a new savings account, you may also want to take into consideration the accessibility of the ATMs as some of them may have fewer around.

This article was first published in Seedly.