Best mortgage insurance in Singapore (2021)

PHOTO: Unsplash

What if we can’t make our home loan repayments one day? With mortgage insurance, you can ensure that your outstanding loan amount is taken care of if misfortune or tragedy strikes.

When we buy a home, the litany of insurance products deemed as important can seem endless — and with good reason. Your home could easily be the most expensive asset you own and the importance of protecting it holds no bounds.

First thing that may be pop into mind while we’re on this topic is fire insurance and home insurance, as they are usually dubbed as the ultimate duo for essential home coverage. But what may fly under your radar is another, equally important financial coverage against the messiness that is life — mortgage insurance.

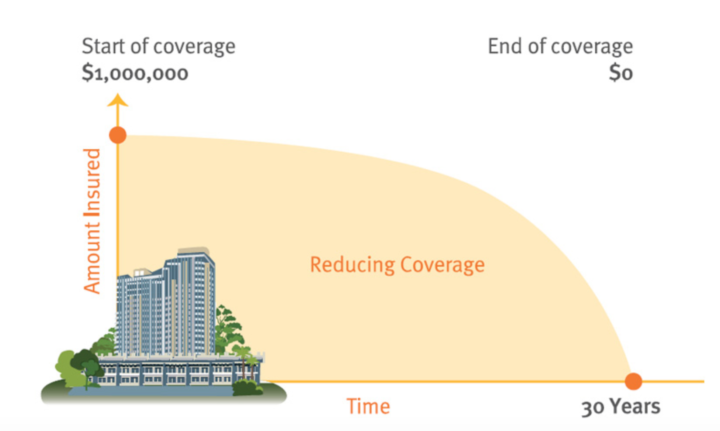

Mortgage insurance is also known as Mortgage Reducing Term Assurance (MRTA). This means that the sum assured reduces as the policy term ages — the outstanding home loan amount also reduces with time (as seen in the above illustration).

When life gives you lemons and you find that you can no longer pay your home loan repayments, mortgage insurance provides a safety net in the form of a lump sum payment to service the outstanding home loan amount.

This ensures that your spouse and/or family will never have to bear the brunt of paying the loan installments should anything happen to you or fear the possibility of homelessness.

Besides preventing considerable financial burden, buying mortgage insurance also gives you the peace of mind that your family will always have a roof over their heads.

Granted, all HDB homeowners who choose to pay off their mortgage via CPF savings are already covered by the mandatory Home Protection Scheme (HPS). However, private insurance products on the market could potentially give your more perks and better coverage than HPS.

ALSO READ: Why HDB flat owners need to know about the Home Protection Scheme

That being said, whether you own an HDB flat or private property, it’s highly recommended for you to get mortgage insurance if you’ve taken up a home loan. As we’ve already established, your home is your most precious asset, and you would want to protect it from foreclosure if your ability to make mortgage repayments is hindered.

Below, we’ve narrowed down the best mortgage insurance plans in town to ease your search.

| Plan Name | Interest Rate | Key Benefits | Optional Riders/Benefits | Other Info |

| AXA Decreasing Term Insurance | 0 per cent to 15 per cent |

Covers death, total and permanent disability or terminal illness Choice of single or regular premium payments in 1-year intervals, from 10 to 30 yearsSingle premium payment term between 5 to 30 years Regular premium payment term between 10 to 30 yearsJoint life coverage for both co-owners |

Personal accident benefit Living accelarator benefitWaiver of premium benefit |

|

| Great Eastern MortgageCare | Pegged to home loan interest rate |

Covers death, disability or terminal illness Joint life coverage for both co-ownersFixed premium throughout limited premium term |

Get free 12 months’ Dengue Care when you sign up for regular premium plans | |

| Etiqa eProtect mortgage | 1 per cent to 4 per cent |

Covers death, total and permanent disability or terminal illness Policy term between 6 to 40 years or up to age 75 (ANB), whichever is earlierPay premium for 90 per cent of policy term |

eXTRA secure waiver | Cash advance for funeral expenses |

| Prudential PruMortgage | 1 per cent to 7 per cent |

Covers death or terminal illness, with option of coverage against total and permanent disability Policy term between 10 to 35 years Joint life coverage for both co-owners |

DisabilityEarly Stage Crisis WaiverCrisis Waiver III |

When buying a mortgage insurance plan, you will likely peg your home loan interest rate to the insurance interest rate. The last thing you want is to be over or under-insured.

This is why an insurance plan which offers a wide range of interest rates is key. Luckily, the AXA Decreasing Term Insurance plan provides homeowners with exactly that — offering interest rates ranging from 0 per cent to 15 per cent. Best of all, the interest rate can be pegged at 1 per cent intervals, giving you the flexibility to choose the coverage amount you need and align seamlessly with your mortgage loan rate.

Thanks to the plan’s flexible premium payment terms, you have the flexibility to choose regular payment terms if you’re not comfortable with making a single premium. Note that there’s a premium waiver for the last three years if you opt for the former.

If rising premium payments is one of your biggest concerns, the Great Eastern Mortgage Care plan puts those worries promptly to rest. Your annual premium amount is fixed throughout the duration of the limited payment term. Limited payment term means that while the policy term is set at 10 years, the plan can be fully paid off within 8 years.

You’ll also be pleased to know that if you and your spouse are co-owners, you’ll both enjoy joint coverage and receive a payout that amounts to the outstanding loan in the event that something happens to either one of you.

Moreover, if you find it necessary to get enhanced coverage for critical illnesses, you’ll also have the option to choose add-on cover for 37 different illness types with the MortgageCare (Living Assurance) plan.

If flexibility is what you’re looking for in a mortgage insurance plan, Etiqa’s eProtect mortgage is a worthy option to consider. The protection is quite extensive, with a lump sum payout in the event of death, total and permanent disability or terminal illness.

Policy holders are able to select the policy term length they prefer which ranges from six to 40 years, or up to age 75 (age next birthday), whichever is earlier.

Based on your home loan interest rate, you can choose your preferred interest rate of 1 per cent to 4 per cent. Limited premium term is on the table as well, allowing policy holders to make premium payments for only 90 per cent instead of the entire policy term.

You can also opt for eXTRA secure waiver, which offers add-on coverage for premium waiver in the event of an unfortunate critical illness diagnosis.

What makes this stand out from the others on the list is that you’ll have the freedom to choose the frequency of premium payments — monthly, quarterly, bi-annually or annually — as your premium amount remains the same.

While there’s no limited payment term and coverage is not as extensive as Etiqa’s (death and terminal illness coverage only), you’ll find that this mortgage insurance plan does the job in protecting you from the unforeseen.

You can choose your preferred policy term duration (10 to 35 years) and interest rate (ranging from 1 per cent to 7 per cent) — plus the sum assured amount in order to fully repay the outstanding home loan amount.

If you and your spouse are co-owners of the house, you’ll also be pleased to know that PruMortgage is a joint-life policy and offers coverage for both of you.

This article was first published in SingSaver.com.sg.