Buying a BTO flat in 2021? Here are 5 important changes you should be aware of

PHOTO: Stackedhomes

It’s BTO season right now with the launch of the May 2021 BTO flats . As of the time of writing, the number of applicants is more than 5x oversubscribed for three-room flats and above – and by the end of tonight, it could be worse.

So while you may have missed the boat for this one, there’s still an August 2021 BTO launch to look out for.

And despite the availability of the HDB website, there’s still a lot of confusion among first-time buyers of HDB flats. This is especially prevalent among home buyers who are getting advice from friends or family, who bought their units decades ago.

Times have changed; so for those applying for a BTO flat – especially in the current Covid-19 environment – do take note of some key differences:

In the same month we’re writing this (May 2021), the public has been surprised at the lack of details on the November BTO launch. As it turns out, this wasn’t a mistake or delay.

HDB has just said that, from this point forward, only the town of BTO launch sites, and the types of flat available, will be announced six months prior. The exact site location, along with the number of flats available, will only be announced three months prior.

[[nid:502588]]

This is a reversal of a previous practice from 2019, when we would know the exact site and flat numbers six months beforehand. HDB hasn’t yet given a reason for this.

While this isn’t a huge impact overall, it does create an added layer of annoyance. Without knowing the number of flats available , it’s harder to guess if the flats are going to be oversubscribed (although some analysts opined that’s easy anyway – as long as it’s a mature estate, you can safely bet it will be).

You also have less time to scout out the exact site and make a decision. And as plenty of home buyers can tell you, just knowing which HDB town the launch is in is a bit vague. Tampines, for instance, can mean being close to the hotspot of Tampines hub, or way off where it straddles the boundary of Bedok Reservoir.

We’ll still update you with BTO site analysis when it becomes available, but now you know why they’ll be coming in later.

As of 2019, the Special CPF Housing Grant (SHG) and Additional Housing Grant (AHG) schemes became defunct. These have effectively been combined into the Enhanced Housing Grant (EHG) scheme.

The EHG came with the following changes:

The grant amount is as follows:

| Monthly Household Income | EHG Amount |

| $1,500 or under | $80,000 |

| $1,501 to $2,000 | $75,000 |

| $2,001 to $2,500 | $70,000 |

| $2,501 to $3,000 | $65,000 |

| $3,001 to $3,500 | $60,000 |

| $3,501 to $4,000 | $55,000 |

| $4,001 to $4,500 | $50,000 |

| $4,501 to $5,000 | $45,000 |

| $5,001 to $5,500 | $40,000 |

| $5,501 to $6,000 | $35,000 |

| $6,001 to $6,500 | $30,000 |

| $6,501 to $7,000 | $25,000 |

| $7,001 to $7,500 | $20,000 |

| $7,501 to $8,000 | $15,000 |

| $8,001 to $8,500 | $10,000 |

| $8,501 to $9,000 | $5,000 |

The EHG has greatly simplified the grant process, as you’re no longer trying to meet criteria in two different schemes. The most significant impact, however, comes from the universality of the EHG; buyers could potentially afford a BTO flat even in a mature district, thanks to the grant.

As of March 2020, HDB has eased up on eligibility rules for single and / or unmarried parents.

Divorced or widowed parents can now form a family nucleus with their child (the child must be under your legal custody). This allows them to buy under the Public scheme, which means they can buy from age 21 onward. These single parents are also no longer restricted in terms of flat size and location.

[[nid:525946]]

An unwed parent can also buy a flat from age 21 or above. They can now buy up to three-room BTO flats in non-mature estates (previously they were restricted to two-room flats).

The EHG applies similarly to an unwed parent as it does to any single buyer (i.e., they receive half the grant amount a couple does).

These changes have significantly increased the range of BTO flat options for this demographic. However, do bear in mind that single parent buyers must still meet the Mortgage Servicing Ratio (MSR) – their monthly home loan repayment still cannot exceed 30 per cent of their gross monthly income.

This could make larger flats unaffordable on single income, even if they meet the other criteria.

As of 2019, the income ceiling for flats has been raised to $14,000 a month, for four-room or bigger flats. If you’re purchasing a flat with extended family as co-owners, the ceiling is raised to $21,000.

For three-room or smaller flats, the income ceiling is either $7,000 or $14,000 (HDB will specify the amount for each project).

If you previously found yourself just over the income ceiling, you might want to try again for a BTO flat.

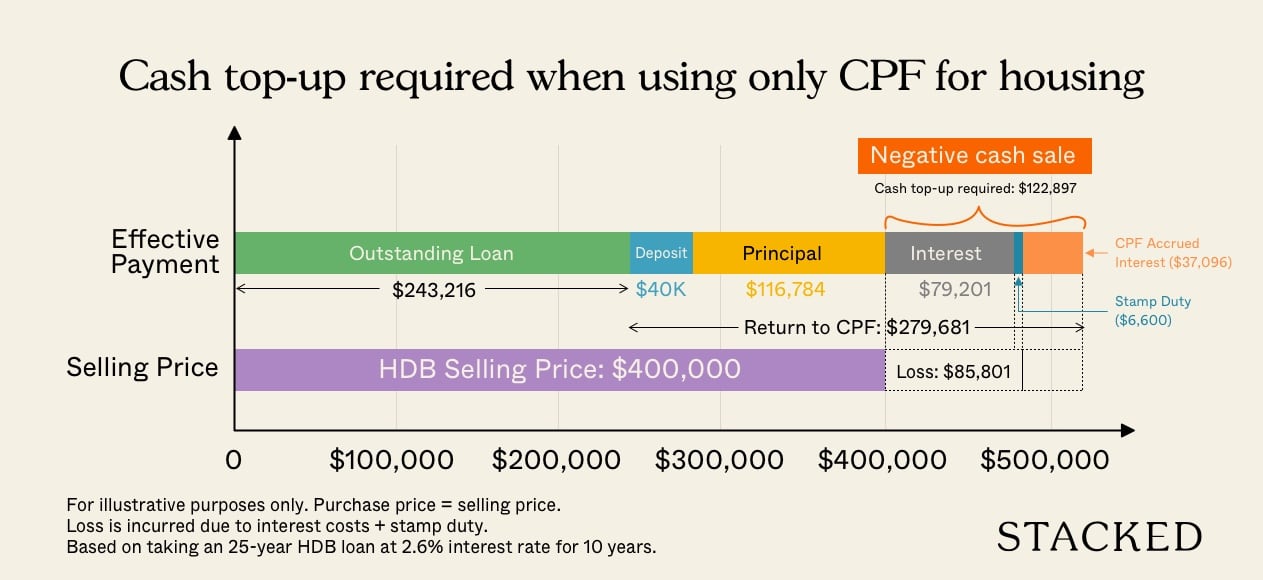

As of 2018, you no longer need to wipe out your entire CPF Ordinary Account (CPF OA) when buying an HDB flat. You can now opt to keep up to $20,000 in your CPF OA.

This allows buyers to create a safety buffer. In fact, it’s advisable to retain at least six months of your monthly loan repayments; and it may as well be in your OA (since an interest rate of 2.5 per cent is more than a savings account would give you).

Do talk to a financial professional about it however, as it may not be for everybody. If you already have enough savings, for example, it may be better to use it all and reduce your loan quantum.

To date, 85 per cent of BTO projects – or around 43,000 homes – are facing delays of six to nine months. This means that, if you buy a BTO flat this year, you should have a contingency plan for any delays.

We’ve said it time and again, but it’s also worth noting that the Minimum Occupancy Period (MOP) is five years, starting from the point of key collection.

[[nid:527135]]

This may be off-putting to buyers with an eye on asset progression; it means at least half a year of waiting before your flat can be sold on the open market (in the meantime, private property prices are steadily rising).

Contractors and interior designers are similarly affected by supply and labour shortages. Unless you make the most spartan choices, do expect a second delay stemming from this.

All in, BTO flat buyers in 2021 may want to plan for an additional 12 months delay.

This article was first published in Stackedhomes.