Enhanced Housing Grant: How much do you get and how does it affect your first HDB flat purchase?

PHOTO: Unsplash

2026 offers a warm welcome to first-time homeowners. New Build-to-Order (BTO) launches in developing areas (Bayshore and Tengah) have drawn strong interest. More young couples are also turning to resale flats to live nearer to work, parents, or familiar neighbourhoods.

With the introduction of the Enhanced Housing Grant (EHG), planning your first home purchase now feels more open and hopeful than before.

While the grant isn't new, the updated amounts and wider eligible income coverage give first-timers more flexibility to choose the home that truly fits them.

For couples and singles in their twenties and thirties, these updates prove beneficial in shaping their home ownership choices — whether to wait for a BTO, or consider a resale

As you plan your first home purchase, it's important to understand how these grants work. While they lower the upfront cost of buying a flat, they aren't a free windfall.

Eventually, when you sell your flat — whether you're upgrading or right-sizing — the grant amount will have to be returned to your Ordinary Account with accrued 2.5 per cent interest. This will be automatically deducted from your sale proceeds.

What this means for you:

A simple way to think about it:

CPF housing grants work like using a portion of your future CPF savings to reduce your housing cost today. When you sell your flat, the amount goes back into your CPF.

Grant refund at sale = Grant amount used × (1 + 2.5 per cent yearly interest )^ number of years

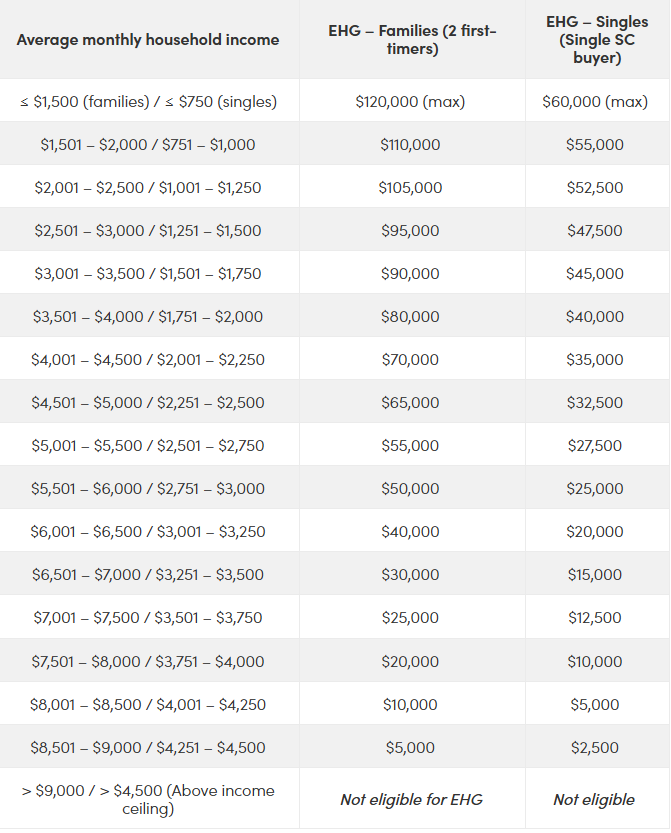

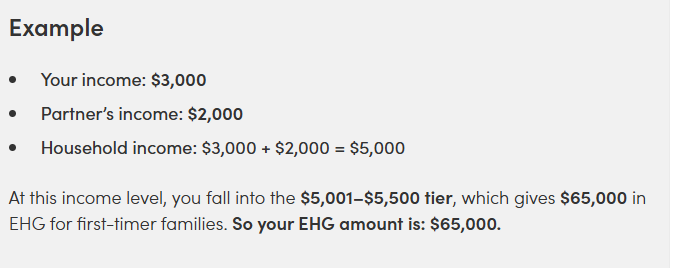

The amount of Enhanced CPF Housing Grant (EHG) you qualify for depends on your average monthly household income. The lower your income, the higher your grant. After the 2024-2025 enhancements, families can receive up to $120,000 and singles up to $60,000.

Should you choose to buy a resale flat, the EHG forms only part of your total support.

When combined with the EHG, these grants can amount to as much as $230,000 for eligible first-timer applicants.

Let's see how the new EHG will affect the purchase of HDB flats.

With that in mind, here's how the updated EHG affects the real cost of buying a HDB flat.

To find out how much you qualify for, the first step is to determine your average monthly household income. The EHG is designed to support lower- and middle-income first-timers, so the grant amount decreases as your household income increases.

Here's how your 2025 income is assessed:

The lower your combined income, the higher your EHG quantum, and the more grant you have to reduce the upfront costs of your first home.

Notes: The above EHG amounts assume the flat's lease covers the youngest buyer to age 95; if not, the grant will be pro-rated .

"Families" refers to households with two first-timer applicants (e.g., a married couple who are both first-time owners). First-timer households comprising one first-time and one second-time homeowner can qualify for half of these grant amounts (since their income ceiling is halved to $4,500).

Singles grants apply to single Singapore Citizens aged 35 or above buying on their own (under the Single SC Scheme), or joint singles schemes as applicable.

Before the EHG was introduced in 2019, AHG and SHG had stricter conditions: lower income ceilings, different grant amounts for different estates, and restrictions on flat size. Many lower-income couples couldn't enjoy the full grant unless they bought smaller flats in non-mature estates.

Today, the upgraded EHG is much simpler and far more generous in allowance:

This gives first-time homeowners more freedom to choose a flat that truly fits their needs-instead of being forced into certain flat types just to maximise grants.

Historically, resale flats were known to be pricier than BTO flats, even after accounting for grants. With the 2024-2025 grant enhancements, the playing field has shifted-especially for first-timer homeowners buying resale.

Here's why:

Resale buyers, however, can stack three major grants:

- CPF Housing Grant (Family Grant): up to $80,000 (income ceiling $14,000)

- Enhanced Housing Grant (EHG): up to $120,000 (income ceiling $9,000)

- Proximity Housing Grant (PHG): up to $30,000 (if living with parents) or $20,000 (within 4km)

First-timer couples buying resale can receive up to $230,000 in total grants, compared to a maximum of $120,000 for BTO buyers.

With this level of grant support, a resale flat can be more affordable than many first-timers think. For those eligible for the Proximity Housing Grant, the final cost may rival that of a new BTO, especially when you consider location and quicker move-in.

As we said earlier, there are some limits to how you can use your grant:

Rohaini and her fiance are planning to buy a 4-room resale flat costing $500,000. It's their first home, and both are Singapore Citizens. Together, they earn a combined monthly of $7,000.

Based on the 2025 grant scheme, they qualify for:

Total grants they qualify for: $105,000

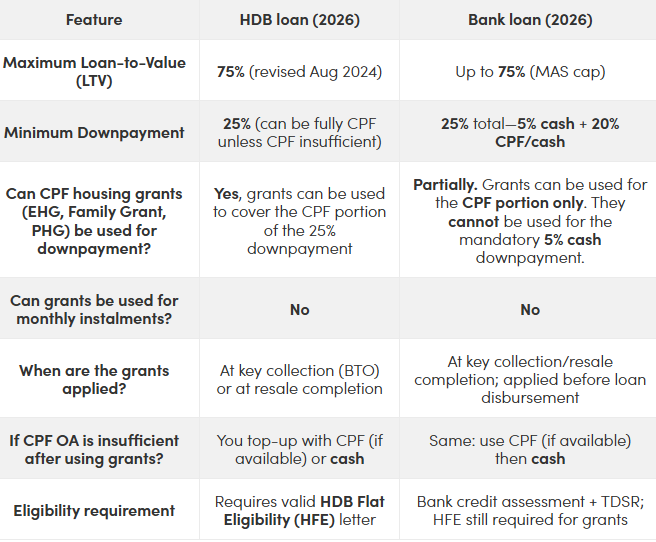

A bank loan requires a 25 per cent downpayment:

Their grants of $105,000 can be used only for the CPF portion, not for the mandatory cash.

Meaning:

Since Rohaini and her fiance don't have $25,000 cash saved, the bank loan option isn't feasible right now-even though they technically have enough CPF and grants to cover the 20 per cent.

Under the current rules, a HDB loan requires a 25 per cent downpayment-but the key advantage is:

There is no mandatory cash component.

The entire 25 per cent can be paid using CPF savings + CPF housing grants.

For their $500,000 flat:

Outcome:

They don't need to fork out cash upfront, and HDB finances the remaining 75 per cent (up to limits stated in their HFE letter).

How the grants work long-term

When Rohaini eventually sells the flat, the grants used-and any CPF she used for the flat-will be returned to her CPF OA with 2.5 per cent accrued interest.

This ensures her retirement savings stay intact while allowing her to afford her first home.

[[nid:727528]]

This article was first published in MoneySmart.