Far East Hospitality Trust share price at $0.54: Is this a buy?

PHOTO: Pexels

Far East Hospitality Trust ‘s share price (technically known as unit price for REITs and trusts) has plunged around 31 per cent, to $0.54 on June 16, 2020.

Market sentiment surrounding Far East Hospitality Trust has certainly been affected ever since the Covid-19 pandemic started in Singapore.

However, does the stapled group present an investment opportunity for long-term investors?

Let’s take a look using my 10-step guide to pick the best Singapore REITs .

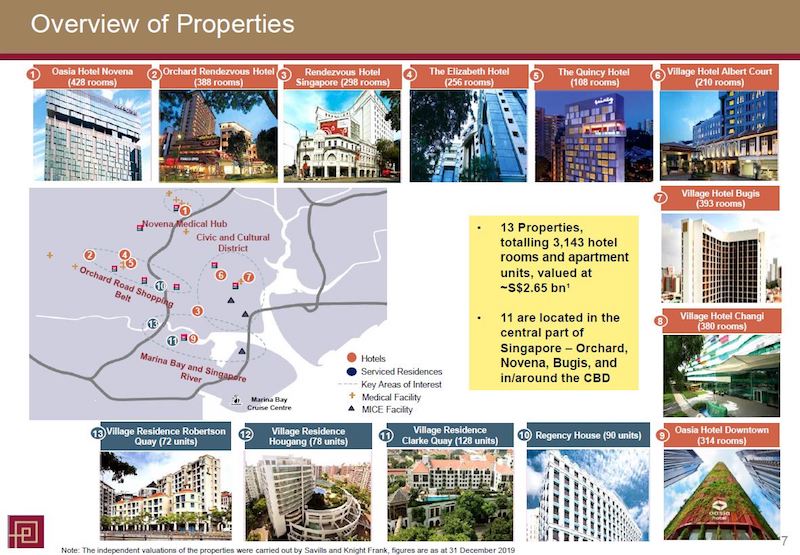

Far East Hospitality Trust is a Singapore-focused hotel and serviced residence hospitality trust.

Currently, the trust has a portfolio of nine hotel properties and four serviced residences, making it Singapore’s largest diversified hospitality portfolio by asset value.

Far East Hospitality Trust’s sponsor is Far East Organisation, which has a 61 per cent stake in the trust.

Check for: Increasing gross revenue and NPI

Far East Hospitality Trust has a financial year that ends on 31 December each year.

Firstly, let’s check out how it has performed in the last five financial years.

| 2015 | 2016 | 2017 | 2018 | 2019 | Compound Annual Growth Rate (CAGR) | |

|---|---|---|---|---|---|---|

| Gross Revenue (S$' million) |

114.6 | 109.1 | 103.8 | 113.7 | 115.5 | 0.2 per cent |

| Net property income (S$' million) |

103.7 | 98.4 | 93.2 | 102.8 | 104.3 | 0.1 per cent |

From 2015 to 2019, both gross revenue and NPI have increased, even though they have been inconsistent.

For the first quarter of 2020, gross revenue tumbled 18 per cent to $22.9 million largely due to a decline in the hotels’ master lease rental as a result of the Covid-19 pandemic. Correspondingly, NPI fell 21 per cent to $19.9 million.

Verdict: Pass

Check for: Increasing DPU

Now let’s look at Far East Hospitality Trust’s historical growth of distribution per stapled security (DPS; similar to DPU for REITs).

| 2015 | 2016 | 2017 | 2018 | 2019 | CAGR | |

|---|---|---|---|---|---|---|

| DPS (Singapore cents) | 4.60 | 4.33 | 3.90 | 4.00 | 3.81 | -4.6 per cent |

Over the past five years, Far East Hospitality Trust’s DPS has fallen, and that’s not a good sign.

Verdict: Fail

Check for: Property yield of between 5 per cent and 9 per cent

For 2019, Far East Hospitality Trust had an NPI of $104.3 million and a portfolio value of $2.65 billion.

The figures translate to a property yield of 3.9 per cent.

Far East Hospitality Trust fails this criterion as well.

Verdict: Fail

Check for: Gearing ratio below 40 per cent

As of 31 March 2020, Far East Hospitality Trust had a healthy gearing ratio (also known as “aggregate leverage”) of 39.5 per cent, which just meets my criterion of below 40 per cent.

Verdict: Pass

Check for: Interest coverage ratio above 5 times

At the end of 2019, Far East Hospitality Trust’s interest coverage ratio stood at 3.1 times, which is below 5 times.

Verdict: Fail

Check for: Healthy portfolio occupancy rate

Far East Hospitality Trust’s hotel portfolio had a strong start in January 2020 but was affected by the onset of Covid-19 thereafter.

Due to that, for the first quarter of 2020, the trust’s hotel portfolio’s average occupancy fell by 23.9 per cent points year-on-year to 65.3 per cent.

However, the latest occupancy rate is much better than Singapore’s industry average of around 41 per cent for medium and large hotels.

The average occupancy of Far East Hospitality Trust’s serviced residence portfolio performed better, improving 3.4 percentage points year-on-year to 83.6 per cent. The strong performance was on the back of long pre-existing leases and lease extensions into February and March.

Verdict: Pass

Check for: Positive rental reversions

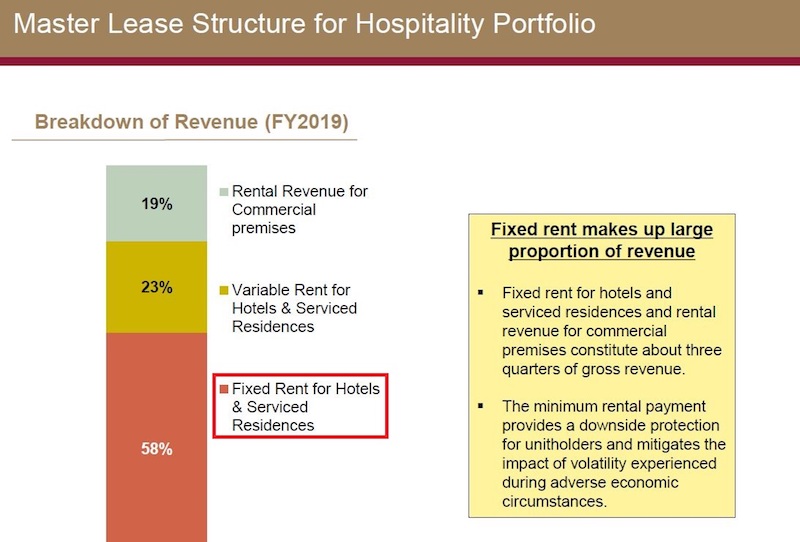

The majority of Far East Hospitality Trust’s gross revenue is from fixed rent.

The rent falls under master leases that have a tenure of 20 years from 2012, with an option to renew for an additional 20 years.

Therefore, in my opinion, the rental reversion criterion is not applicable to Far East Hospitality Trust since there’s no option to renew leases on an ongoing basis every three years or so, unlike other REITs.

Verdict: Not Applicable

One way for Far East Hospitality Trust to grow is through acquisitions. In its 2019 annual report, the trust said:

“The REIT Manager actively pursues acquisition opportunities in the market that provide attractive cash flows and yields to enhance the returns to Stapled Securityholders to boost future income and capital growth.”

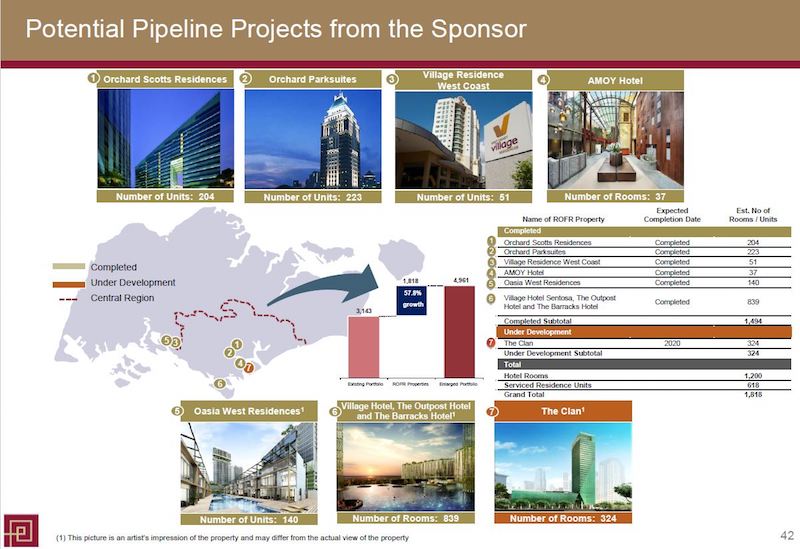

On that front, Far East Hospitality Trust has an acquisition pipeline of seven properties under the right of first refusal (ROFR) agreement with its sponsor, Far East Organisation.

The ROFR arrangement ensures that Far East Organisation offers the properties to Far East Hospitality Trust for purchase consideration first before any other company.

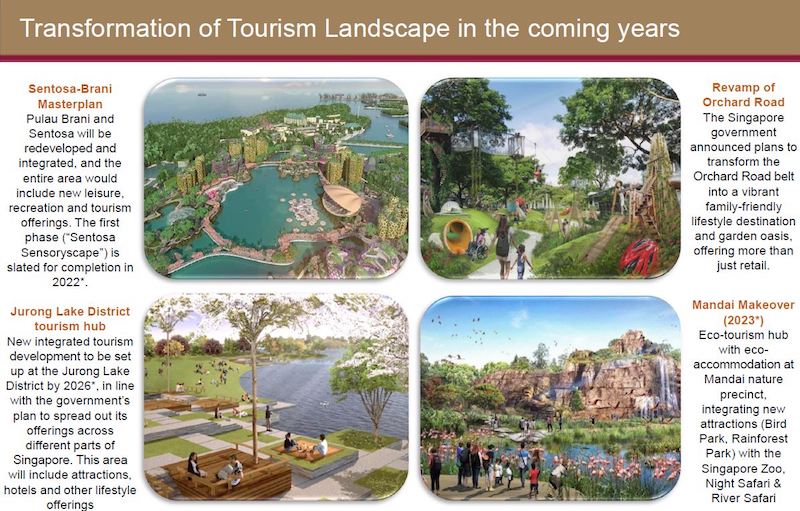

Over the longer term, Far East Hospitality Trust could also benefit as the tourism industry recovers from the Covid-19 pandemic and transforms itself to attract more visitors to Singapore.

Verdict: Pass

Check for: Acceptable price-to-book ratio

At Far East Hospitality Trust’s current unit price of $0.54, it has a price-to-book (PB) ratio of 0.63x, which is below the five-year average PB of 0.72x.

Verdict: Pass

Check for: Distribution yield to be above 5 per cent

At Far East Hospitality Trust’s unit price of $0.54, its distribution yield stands at 7.1 per cent, based on 2019 DPS.

Potential investors should note that Far East Hospitality Trust’s 2020 DPS is likely to fall due to the business impact from the Covid-19 pandemic.

Verdict: Pass

Far East Hospitality Trust has a final score of 6/9.

Even though the trust may look cheap right now, I won’t be investing in it given its slow growth in gross revenue and NPI, and falling DPS from 2015 to 2019.

However, I’m keen to find out if Far East Hospitality Trust’s growth factors actually translate to higher DPS post-pandemic.

Therefore, I’d place Far East Hospitality Trust on my watchlist.

This article was first published in Seedly. All content is displayed for general information purposes only and does not constitute professional financial advice.