HDB resale prices edge up as transaction volumes rebound in May 2026

HDB resale prices edge up, but a broader trend suggests the resale market has largely stabilised.

PHOTO: AsiaOne file

Singapore's HDB resale market returned to modest growth in May, with both prices and transaction volumes recovering from the slight pullback seen a month earlier.

While the monthly rebound may appear encouraging, the broader trend suggests that the resale market has largely stabilised.

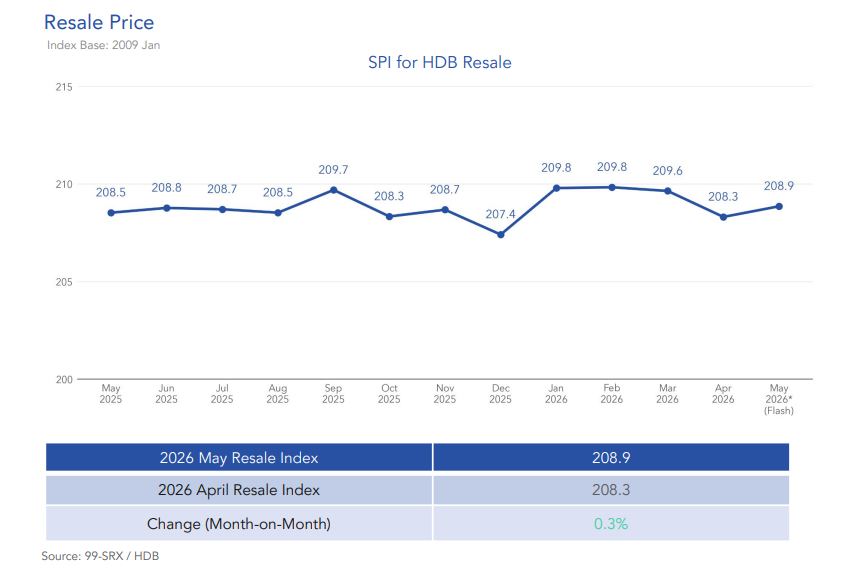

According to the latest 99-SRX Flash Report, HDB resale prices rose 0.3 per cent month-on-month, reversing April's 0.6 per cent decline and bringing the overall resale price index to 208.9.

Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, noted that price fluctuations are consistent with a market that has been range-bound all year.

Since May 2025, overall resale prices have increased by just 0.2 per cent, indicating that monthly fluctuations have largely offset one another.

While prices dipped in April, May's rebound effectively restores the market to its recent trading range rather than signalling the start of another strong upward cycle.

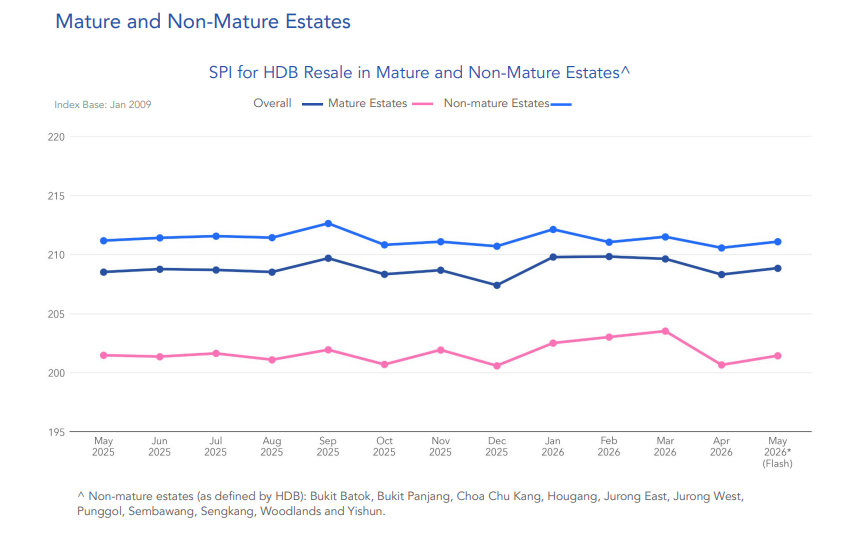

Resale prices in mature estates rose 0.4 per cent month-on-month, slightly outpacing the 0.2 per cent increase recorded in non-mature estates.

However, the difference remains marginal, suggesting that demand continues to be relatively broad-based across the island rather than concentrated in any particular segment.

On an annual basis, prices in both mature and non-mature estates were largely unchanged compared to May 2025.

This further reinforces the view that the HDB resale market has entered a more stable phase after the sharp gains seen in previous years.

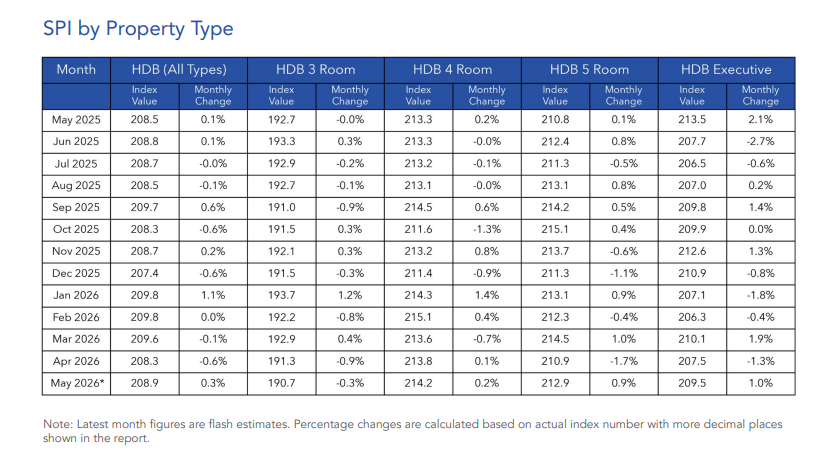

The latest figures show that demand for larger HDB homes remained resilient in May.

Executive flats posted the strongest monthly price growth, rising one per cent, while five-room flats climbed 0.9 per cent.

Four-room flats saw a more modest increase of 0.2 per cent. In contrast, prices for three-room flats slipped by 0.3 per cent, making them the only segment to register a decline for the month.

Interestingly, Executive flats also posted the most decline on a year-on-year basis.

The prices were down 1.9 per cent, while prices for smaller three-room flats slipped by one per cent compared to May 2025.

The four-room and five-room flats edged up by 0.4 per cent and 1.0 per cent, respectively.

The divergence between flat types could reflect current buyer preferences.

Larger flats continue to attract families looking for more space, while smaller units face softer demand amid a growing supply of resale options.

Particularly in the Executive flat segment, which is known for its rarity and larger layout, the price growth appears to be more moderate compared to a year ago.

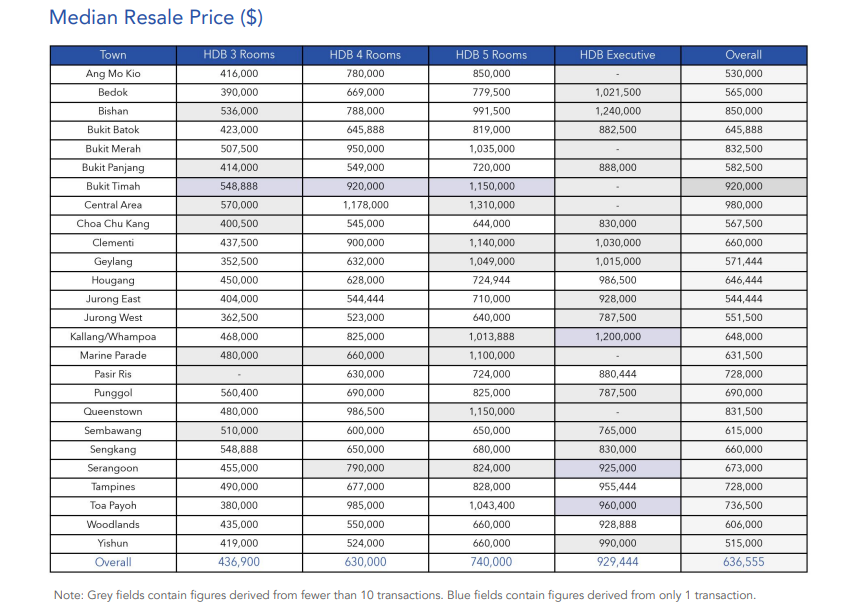

Median resale price by town and flat type:

The relatively muted pace of price growth comes as the HDB resale market enters a very different supply environment from the one seen in 2025.

"The measured trajectory reflects supply catching up with demand: an estimated 13,500 flats reach their five-year Minimum Occupation Period (MOP) in 2026, nearly double the low 2025 figure, and units already entering the market are tempering price growth," Mr Luqman explained.

Many of these newly eligible flats are gradually entering the resale market, giving buyers more choices and reducing the urgency that previously fuelled stronger price increases.

This helps explain why monthly price movements have remained relatively small despite healthy buyer demand.

After falling 0.6 per cent in April and recovering 0.3 per cent in May, the market has essentially been moving sideways over the past year.

The fact that overall resale prices are only 0.2 per cent higher than they were in May 2025 suggests that the additional supply is helping to moderate growth rather than trigger another surge in prices.

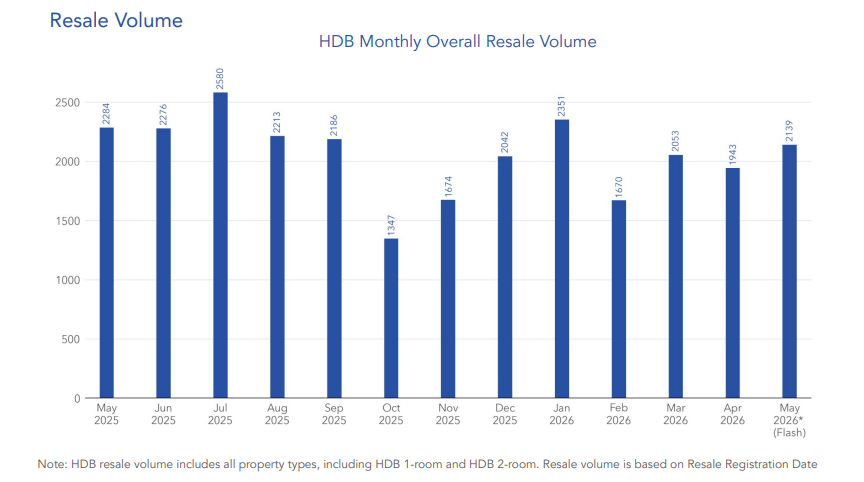

Alongside the modest price recovery, transaction activity also picked up during the month.

An estimated 2,139 resale flats were transacted in May, representing a 10.1 per cent increase from April's 1,943 units.

The rebound may indicate that some buyers who had adopted a wait-and-see approach earlier in the year have returned to the market.

Even so, transaction volumes remained below last year's levels, with May 2026 recording 6.3 per cent fewer resale deals than May 2025.

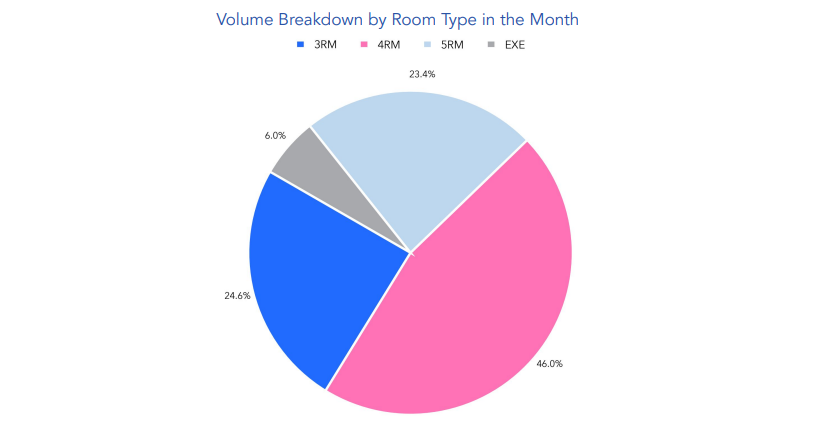

Four-room flats continued to account for the largest share of transactions, making up 46.0 per cent of all resale deals.

They were followed by three-room flats at 24.6 per cent, five-room flats at 23.4 per cent, and Executive flats at 6.0 per cent.

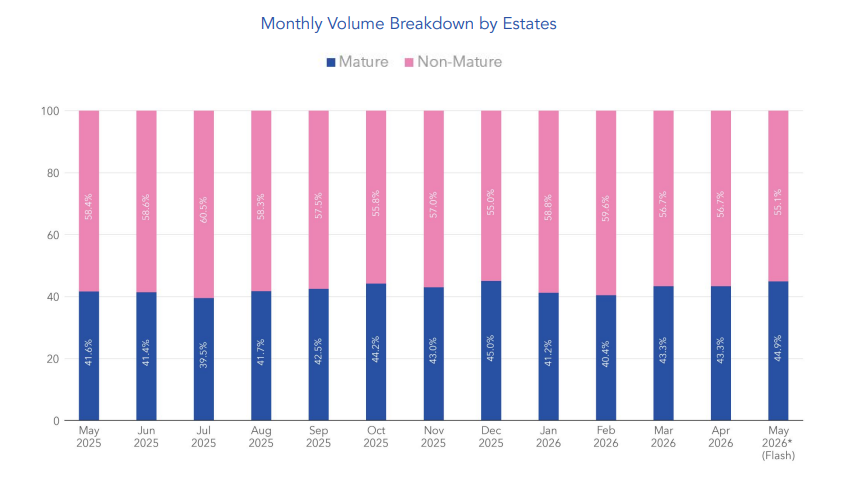

Location-wise, the transaction mix also remained fairly balanced.

Non-mature estates accounted for 55.1 per cent of all resale deals in May, while mature estates made up the remaining 44.9 per cent, indicating that buyers continue to find value across both established and newer towns.

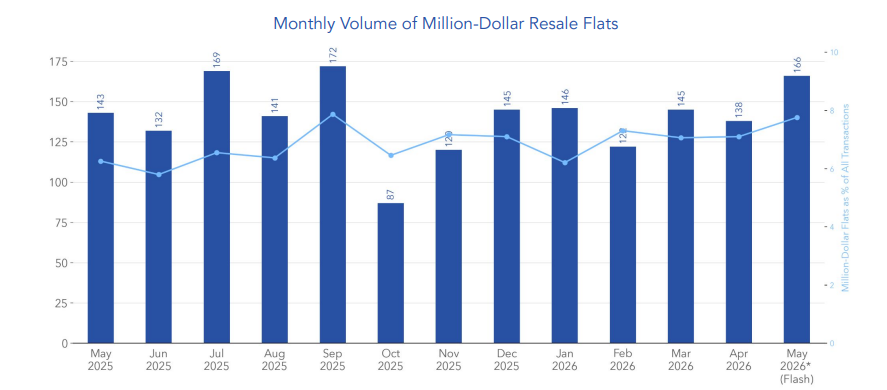

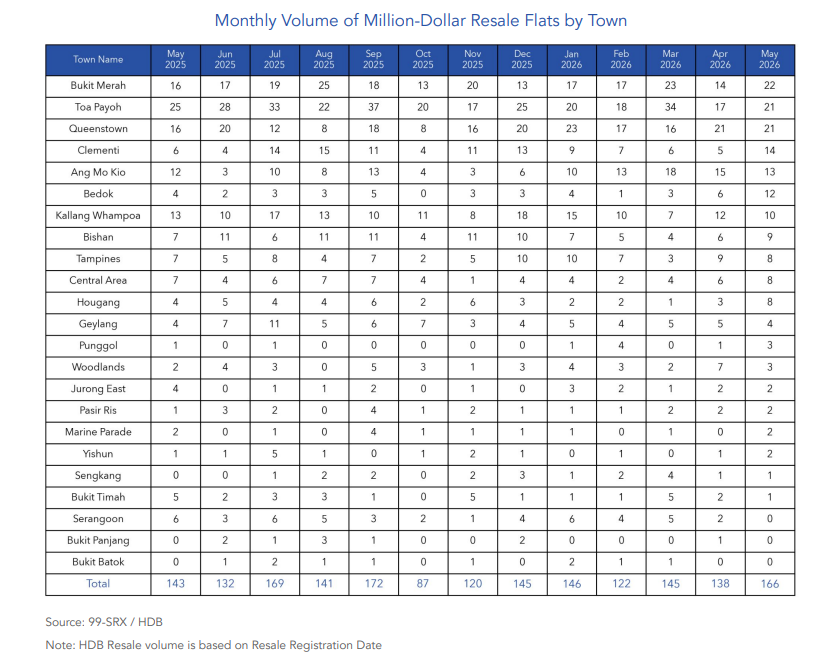

The million-dollar HDB segment also saw activity recover in tandem with the broader market. Mr Luqman noted that "at the top end, the million-dollar segment held its steady 7.8 per cent share, though the count rose to 166 from 138 in April as overall volume recovered".

Notably, the 166 million-dollar resale flats transacted in May marked the strongest showing in the past six months. It was also just six deals shy of the all-time monthly record of 172 transactions set in September 2025.

As has been the case for much of the past year, mature estates dominated the million-dollar segment. Bukit Merah recorded the highest number of such transactions with 22 deals in May, followed by Toa Payoh and Queenstown with 21 each.

The month's highest resale transaction was a five-room flat at The Pinnacle@Duxton, which sold for $1.63 million. Meanwhile, the highest-priced resale flat in a non-mature estate was an Executive flat in Hougang Street 21 that changed hands for $1,232,888.

May's flash figures reinforce the view that Singapore's HDB resale market is settling into a more sustainable phase.

While both prices and transaction volumes recovered from April's slight dip, the broader trend remains one of stability rather than acceleration.

At the same time, transaction volumes have shown signs of rebound without placing significant upward pressure on prices.

The gradual increase in MOP supply appears to be giving buyers more options and helping to keep price growth in check.

Barring any major shifts in demand, the larger pool of resale flats expected to enter the market throughout the rest of 2026 is likely to support this balanced environment, with moderate price movements and healthy transaction activity remaining the dominant theme.

[[nid:737356]]