How to avoid overpaying your insurance in 3 steps

PHOTO: Pexels

Is your insurance too expensive?

The simple answer is yes… if you’re struggling to keep up with the premium payments. One often hears that you should spend 10 per cent to 20 per cent of your take-home pay on insurance — and anything beyond that is overspending.

But with all things in life, there’s the rule of thumb and there’s the reality of your finances.

Let’s say you earn a salary of $5,000 per month, with about $4,000 left aside after deducting CPF contributions. Although we’d love for it to be the case, it doesn’t mean that you have a cash flow of $4,000 to burn willy-nilly.

After factoring utility and credit card bills, groceries, food, entertainment, investments, the occasional grab ride and savings — the amount left to spend is considerably lower.

With those costs in mind, spending $800 (or 20per cent of your take home pay) solely for insurance may not be as financially wise as you might think.

Let’s chuck away the 10 per cent to 20 per cent ‘rule’ for now and dive deep into the actual money you can comfortably spend on insurance. After all, insurance shouldn’t be a burden for you to bear and consequently restrict your daily spending.

Now, let’s start from the beginning. What happens once you get your long-awaited salary? Carry out your responsible adult duties and break it down across the different spending categories, of course.

In this example, let’s explore how a person with a take home pay of $4,000 after CPF deductions would do to manage their money well.

| Expenses | Amount | Proportion of Income |

| Transport | $400 | 10 per cent |

| Groceries | $350 | 8.75 per cent |

| Household Bills | $400 | 10 per cent |

| Loan Payments | $350 | 8.75 per cent |

| Dine Out | $300 | 7.5 per cent |

| Savings | $800 | 20 per cent |

| Entertainment / Leisure | $600 | 15 per cent |

| Investments | $400 | 10 per cent |

| Parent’s Allowance | $200 | 5 per cent |

| Cash Flow Balance | $200 | 5 per cent |

Based on the above example, you’ll find that while this person had $4,000 in his budget to start with, he’s only able to comfortably afford an insurance plan that costs up to $200 or 5 per cent of his take-home salary, assuming that he/she is not going to compromise on savings or investment.

This is considerably lower than if we were to apply the purported “10 per cent to 20 per cent” rule to this budget breakdown.

Even by allocating the minimum 10 per cent of his income for insurance, it would’ve exceeded his comfortable budget and could possibly even affect his cash flow.

Note that the biggest budget allocation here (besides to pay off the necessary expenses) would be his savings, which takes precedence over the rest as it’s instrumental in building up your emergency fund over time and eventually, to grow your wealth.

You’ll find that as you get older, the odds for critical illnesses, strokes, heart attacks and death increase.

[[nid:510926]]

Depending on your profile (age, smoker or non-smoker, male or female, etc.) and how persistent your insurance agent is, you may find the urge to splurge on multiple insurance products to protect yourself against those potential liabilities.

While it’s tempting to lock in that premium while you’re in your prime, it’s more prudent to spend on the coverage you need for your age without impacting your cash flow.

Start off with only the essentials by opting for a lower-tier Integrated Shield plan (IP) and add on other insurance products (i.e. cancer insurance, critical illness coverage, disability coverage, etc.) when the need arises or when your income increases.

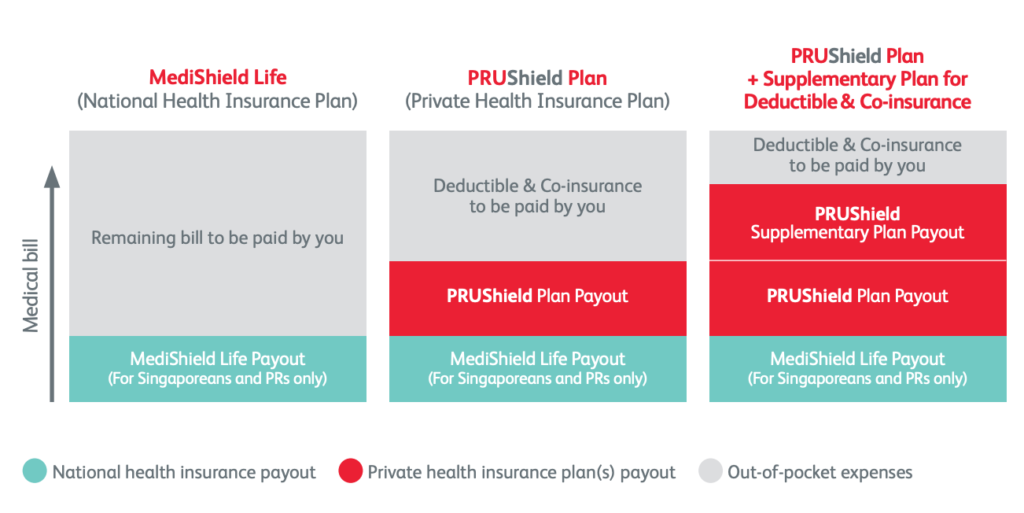

IP plans do the job of filling the gaps in your MediShield Life, such as pre- and post-hospitalisation costs.

Another perk is that your IP premiums can be paid via your MediSave, up to the Additional Withdrawal Limits:

Take for example the Great Eastern Supreme Health B Plus IP, a great B1 ward low-range option that offers the highest annual claim limit of $500,000 at a premium that costs as low as $70 a year (for age 31 to 35).

Or, if you’re more comfortable with an A ward stay (albeit in a public hospital), there’s plenty of cost-effective plans to choose from.

One great option would be the Prudential PRUShield Plus plan which starts at only $82 a year for a $600,000 annual claim limit (for age 31 to 35).

Simply put, calculate the necessary insurance coverage for your needs, and opt for affordable policies that offer sufficient coverage and a high annual claim limit to avoid any out-of-pocket expenses. This prevents you from buying more than you can comfortably afford.

Find the best Integrated Shield plans in Singapore right here.

As we’re only interested in the must-haves here to avoid bursting your budget, the insurance product known as term life insurance definitely falls under the ‘essential’ category — particularly if you have dependents.

Similar to whole life insurance, term life insurance provides a payout to your dependents if something were to happen to you. This way, you’ll always have peace of mind knowing that your loved ones are financially protected.

[[nid:512180]]

Due to its no-frills nature, it is designed solely for protection purposes and doesn’t offer any maturity benefit (unlike whole life insurance) — hence why it’s premiums are lower as well.

One cost-effective term life insurance plan you can consider is the FWD Future First plan with an annual premium of $561*.

As we learned in step 2, you can always increase your coverage as you age or hit certain milestones (like getting married or becoming a parent).

Most importantly, you’re buying insurance with sufficient coverage and you’re able to afford the premium payments without restricting cashflow.

Find the best term insurance plans in Singapore right here.

*Indicative annual premiums generated from CompareFirst.sg, based on the following profile:

With a plethora of different insurance plans out there, you’re bound to find one that is both affordable and offers sufficient coverage for your current needs.

Prioritise the must-haves first (IP plan + term life insurance plan) before exploring higher-tier options and/or other insurance products as your income steadily grows. This way, your insurance plans will always fit comfortably within your budget.

This article was first published in SingSaver.com.sg.