Private housing prices rise in Q1, led by suburban condo sales

A view of the Boon Keng skyline at night.

PHOTO: AsiaOne/Jasper Lim

Singapore's private property market continued to see modest price growth in the first quarter of 2026, but overall activity eased compared to the previous quarter.

Commenting on the latest figures, Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, noted that the price index is rising at a measured pace.

"This more moderate price growth is positive for market sustainability, as it gives prospective buyers more room to evaluate their options without feeling pressured to rush into a purchase for fear of being priced out," he explained.

While the headline numbers point to stability, the underlying trends show a more mixed picture across different segments.

Prices are still rising, particularly in the non-landed suburban market, but overall transaction volumes have pulled back, while supply in the pipeline continues to build.

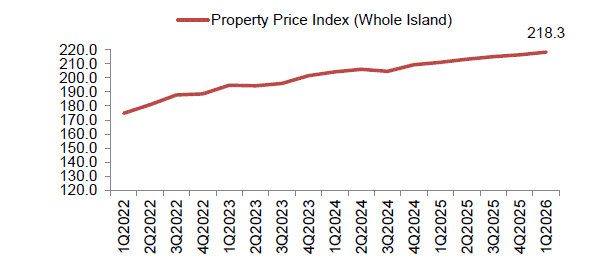

Data from URA showed that overall private home prices rose by 0.9 per cent quarter-on-quarter in Q1 2026, building on the 0.6 per cent increase in the previous quarter. This final figure also came in higher than the earlier flash estimate of 0.3 per cent growth.

These price movements remain broadly in line with 2025's average quarterly increase of 0.8 per cent, suggesting that overall price momentum is still holding up despite a more cautious market environment.

However, not all segments moved in the same direction.

Prices of landed homes actually fell by 0.4 per cent in Q1 2026, reversing the 3.4 per cent increase in the previous quarter.

This marks the first decline for the segment since the start of 2025.

The price decline may be partly attributed to the lower landed home sales activity, down by around 17 per cent from the previous quarter.

At the same time, the slowdown could point to a mismatch in price expectations between buyers and sellers.

Additionally, external factors — such as ongoing geopolitical tensions like the Middle East conflict — may have weighed on sentiment in the landed housing segment.

In contrast, non-landed homes led overall price growth, rising by 1.3 per cent in Q1 2026 after a slight dip in the previous quarter.

This also marks the segment's strongest quarterly performance in five quarters.

The main driver came from the suburban market.

| Segment | Q-o-Q Change (per cent) | ||||

| Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 | Q1 2026 | |

| Non Landed | 1 | 0.7 | 0.8 | -0.2 | 1.3 |

| CCR | 0.8 | 3 | 1.7 | -3.5 | 0.6 |

| RCR | 1.7 | -1.1 | 0.3 | 0.7 | 0.8 |

| OCR | 0.3 | 1.1 | 0.8 | 1 | 2.2 |

Prices in the Outside Central Region (OCR) climbed 2.2 per cent, accelerating from 1.0 per cent previously.

This increase was likely supported by transactions towards the end of March, including those at fast-selling developments like Pinery Residences being reflected in the data.

Meanwhile, the Rest of Central Region (RCR) recorded a more moderate 0.8 per cent increase, while the Core Central Region (CCR) saw a modest 0.6 per cent rebound after a steep decline in the previous quarter.

The overall trend continues to reflect a familiar pattern in today's market.

Demand is still concentrated in more affordable, mass-market segments, particularly in suburban areas.

| Segment | Number of Units Sold |

| New Home Sales (ex. EC) | 2,013 |

| Resale Transactions | 3,225 |

| Sub-sales | 175 |

| Total | 5,413 |

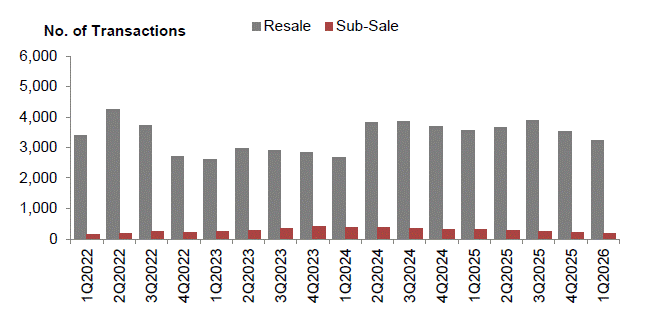

Overall private home sales (excluding ECs) fell by 19 per cent quarter-on-quarter to 5,413 units in Q1 2026, down from 6,699 units in Q4 2025.

The decline was broad-based, with transaction volumes easing across new sales, resale activity, and sub-sales.

This slowdown suggests that buyers may be taking a more measured approach, likely influenced by pricing levels, interest rates, and a more uncertain economic backdrop.

Developer activity slowed in Q1 2026, with both launches and sales easing from the previous quarter.

Developers sold 2,013 private residential units (excluding ECs), marking a 32 per cent quarter-on-quarter decline from the 2,940 units transacted in Q4 2025.

On the supply side, a total of 1,844 new units were launched, down from 2,632 units previously.

| Project | Region | Total Units | Sold Units |

| Newport Residences | CCR | 246 | 185 |

| River Modern | CCR | 455 | 416 |

| Nara Residences | OCR | 540 | 144 |

| Pinery Residences | OCR | 588 | 543 |

While the strong momentum seen at the end of 2025 has tapered, the encouraging response to several new launches — such as Pinery Residences and River Modern — suggests that underlying demand remains supported by genuine buying interest and confidence in the market's longer-term fundamentals.

In the EC segment, developers sold 1,168 new EC units in Q1 2026, marking the highest quarterly sales volume in more than eight years, since 1,415 units were transacted in Q3 2017.

In terms of new supply, 1,320 EC units were launched during the quarter, making it the highest quarterly launch figure since Q3 2015.

This strong performance was largely driven by robust take-up at Coastal Cabana and Rivelle Tampines, both of which benefit from proximity to MRT stations and established amenities in Pasir Ris and Tampines West.

Notably, pricing has also reached new highs, with the median unit price for new ECs climbing to an all-time high of S$1,836 psf in Q1 2026, based on caveats lodged.

[[nid:733283]]

As new launch activity eased, the resale market became more prominent in Q1 2026.

Resale transactions accounted for the largest share of overall activity, reflecting a continued preference among some buyers for completed homes, where prices may be more negotiable, and there is no waiting time for construction.

There were 3,225 resale transactions in the quarter, slightly lower than the 3,529 units recorded in Q4 2025.

Despite the dip in absolute numbers, resale deals made up a larger proportion of the market, accounting for 59.6 per cent of all transactions, up from 52.7 per cent in the previous quarter.

[[nid:733391]]

Mr Luqman noted that, according to the 99-SRX flash report, resale prices were still up 4.9 per cent year-on-year in March 2026, suggesting that the market has not weakened materially despite softer transaction volumes compared with a year earlier.

In terms of profitability, the median capital gain for condo resale transactions stood at S$400,000 in March, while the median unlevered return was 30.3 per cent.

"Although both measures eased from February, they remain substantial, indicating that many existing owners are still sitting on meaningful gains.

"This reduces the likelihood of broad-based distressed selling, even as buyer demand becomes more selective," he explained.

Over in the sub-sale segment, activity continued to decline in Q1 2026.

There were 175 sub-sale transactions recorded, down from 230 units previously.

These sub-sale transactions represent 3.2 per cent of total transactions, compared to 3.4 per cent in the previous quarter.

Notably, this marks the fourth straight quarter of decline in sub-sale volumes, suggesting that most homeowners are holding onto their properties for the long term.

This trend could contribute to a more stable and less volatile market environment.

On the rental front, the market showed early signs of stabilising after a period of softness.

Private home rental prices rose by 0.3 per cent quarter-on-quarter in Q1 2026, reversing the 0.5 per cent decline in the previous quarter.

While the increase remains modest, it suggests that rental prices may be finding a floor following the cooling seen over the past two years.

Leasing activity also picked up slightly.

Based on URA Realis data, private residential leasing volume increased by four per cent quarter-on-quarter to 20,861 rental contracts.

At the same time, median rents edged up from $5.05 psf per month in Q4 2025 to $5.13 psf per month in Q1 2026, indicating a gradual firming in rental rates.

Across segments, non-landed homes led the recovery, with rents rising 0.4 per cent, while landed home rents saw a marginal 0.1 per cent increase, a notable turnaround from the 3.0 per cent decline in the previous quarter.

Regionally, performance remained uneven.

The OCR stood out with a 1.0 per cent increase, rebounding from a 2.0 per cent decline previously.

Rental prices in the Core Central Region grew by 0.5 per cent, while the Rest of Central Region recorded a slight 0.2 per cent decline, pointing to varied demand dynamics across different parts of the market.

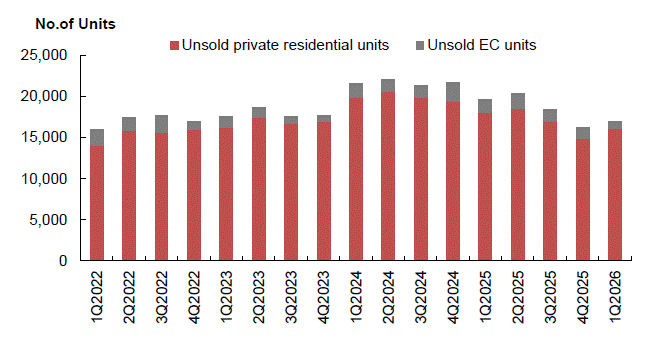

A total of 1,271 private residential units (including ECs) were completed in Q1 2026, adding to the existing housing stock.

On the upcoming supply, as of the end of Q1 2026, there were 42,561 units (including ECs) with planning approval, of which 17,032 units remained unsold.

In addition, another 13,265 unsold units have yet to receive planning approval.

Taken together, this translates to roughly 30,300 units that could potentially be launched in the near term, either later this year or in 2027.

This upcoming supply also includes about 4,600 units (including 635 EC units) from the Confirmed List of the Government Land Sales programme in 1H2026.

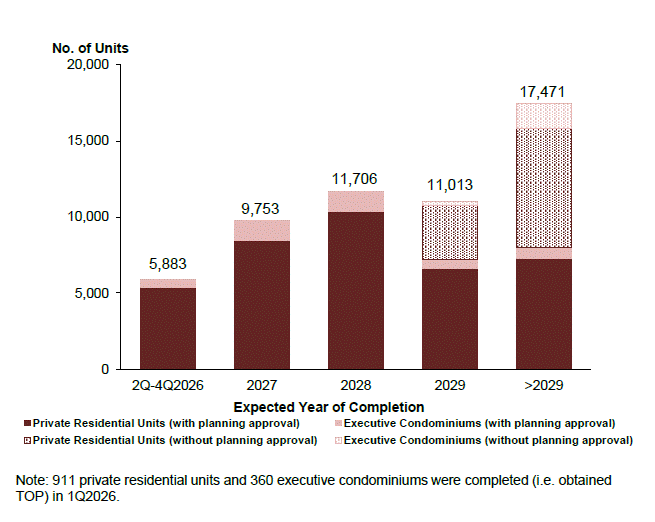

Based on the expected completion dates reported by developers, about 55,800 private housing units are expected to be completed in the coming years.

Of these, about 27,300 units are slated for completion by 2028, with another 28,500 units expected from 2029 onwards.

This steady flow of new supply could help moderate price growth over time, particularly if demand softens.

At the same time, the URA has flagged that the macroeconomic outlook has become more uncertain, and households are advised to remain prudent when purchasing property or taking on mortgage commitments.

[[nid:733569]]