Property market predictions in 2021: Have cooling measures been effective?

PHOTO: Stackedhomes

In the Savills blog, executive director Alan Cheong recently examined the correlation between Singapore’s GDP, and rising property prices. In this recap, we’ve picked out the crucial points that we feel are most useful to home buyers/investors right now; along with some thoughts and on-the-ground observations.

This was the first area we looked at, since it’s often asked whether home prices should have any relation to GDP. Savills highlighted the following advantages, in aligning the two:

*We’re aware there are arguments about the relationship between GDP and productivity, but it’s outside the scope of this recap

There are downsides to this approach as well. One notable example is that it sometimes helps to have home prices high when the GDP falls, given our high home ownership rate.

If you lose your job in a bad economy and need to downsize, for instance, it’s helpful if home prices are high, so you can sell your condo for more. This could work for Singapore given that 90 per cent of the population are home owners, with a property asset.

ALSO READ: Buying property in Singapore? 3 hottest residential estates in Q3 2021

The Savills article notes the current correlation is “already quite good”.

The tracking error, or the degree of difference between nominal GDP and the URA PPI, was at 6.92 per cent between 2000 and 2020. It was at 6.34 per cent between 2013 and 2020.

While there’s no full proof way to identify what causes private property prices to deviate from the wider economic situation, Savills did say that over the decades, the causes have shifted from the economic to the psychological.

Some of the factors they identified as relevant are:

(Everything in parentheses is our addition)

Policy measures are probably the most visible and dramatic factor; and authorities use them to try and reign in (or let loose) prices to better match the wider economic reality.

However, Savills notes that certain policy intervention methods, such as ABSD, do not “self-correct when markets reverse course”. For example, the ABSD rate doesn’t go down if property prices fall.

This can lead to measures that overcompensate, and distort the market. The example given was between 2012 to 2017, when property prices fell behind GDP growth due to cooling measures.

In addition, the cooling measures can cause “adaptive expectations”. As we’ve also found in recent cases, people may react to fears of cooling measures by accelerating their purchase (they want to buy before new measures kick in).

Cooling measures that “price out” segments of the population can also increase underlying demand, as an emotional effect. Part of the appeal of a $15,000 handbag, for example, is how unaffordable it is.

The Savills article notes that each time a cooling measure kicks in, prices “flatline for a period thereafter” and then rise again. When they do rise, they tend to shoot up faster than actual economic growth.

The reasons why prices recover so quickly after cooling measures are:

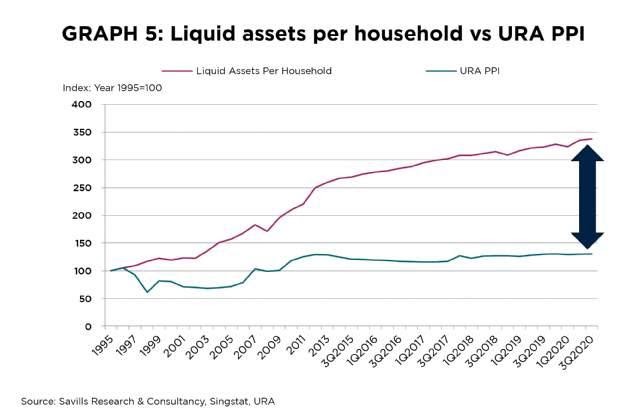

Liquid assets among our households grew at around 3.8 per cent per annum, between 2013 and 2020. In the same time, nominal GDP only rose about 2.6 per cent.

Because Singaporeans store up wealth faster than the wider economy grows, we can still see demand and home prices rising even in rough economic conditions. The article suggested this is overall a negative – it can lead to further cooling measures being used to restrain demand, and even more market distortions.

The number of older Singaporeans (50 to 69 years old) owning private property was around 87,503 in 2000. As of 2020, the number has grown 2.5 times, to 221,274.

When these older Singaporeans retire and downgrade, they will drive up the cost of their right-sized homes (e.g., resale flats or smaller condo units). At the same time, they could provide sufficient wealth to their children, to result in a demand for two residential properties in the next generation.

(Singapore’s shrinking population also contributes to this, as the accumulated wealth is distributed between fewer children).

The article pointed out that many of the “intuitive” variables, which we would assume correlate well to developer sales, actually don’t. From 2004 to 2020, factors such as:

All didn’t show “significant” correlation to developer sales. Rather, it was developer launches (from 2000 to 2020) that showed the best correlation:

Overall, it suggests to us that developers can move units, almost regardless of how well the wider economy is doing!

This could be a further enticement to impose cooling measures, as we can see even mega-developments selling out despite the biggest GDP contraction on record last year.

The article notes that cooling measures have been created “to lower demand by reducing affordability”. In the immediate sense, this widens the inequality in property ownership – the wealthy can buy their homes right now, while the less affluent take an even longer time to afford an upgrade.

[[nid:531885]]

When the latter can finally afford a property, they could race to meet their aspirations by stretching their finances. Also, if the concept of cooling measures becomes normalised (as we at Stacked think it has been), it creates a constant demand.

If you don’t buy now, it could be less affordable when (not if) the next round of cooling measures kicks in. This mindset would be a worrying development, and we agree it’s a contributing reason as to why Singaporeans buy regardless of wider economic issues.

The original article is on Savills and goes into much more detail, but these are what we feel are key points of interest to buyers.

As always, we suggest you stick to the parameters of affordability when buying. Try not to let fear of cooling measures, or relatives getting rich with their homes, be the main drivers.

This article was first published in Stackedhomes.