Late Wednesday (Dec 15) night, the Singapore government announced a package of measures to cool the property market, with the changes taking effect from Thursday (Dec 16).

The additional buyer's stamp duty (ABSD) rates were raised by five to 15 percentage points, the total debt servicing ratio (TDSR) threshold was tightened to 55 per cent, and the loan-to-value (LTV) limit for loans from the Housing Board (HDB) was lowered to 85 per cent.

In addition, public and private housing supply will be increased, to cater to demand.

Here are some quick takes from property analysts on the fresh cooling measures:

Higher ABSD

ABSD rates for the first residential property purchase by Singapore citizens and permanent residents (PRs) remain unchanged at 0 per cent and 5 per cent respectively. But the ABSD rates for all other individuals and entities were raised by five to 15 percentage points.

For instance, Singaporeans buying their second residential property must now pay 17 per cent ABSD, up from 12 per cent previously. Foreigners buying any residential property are subject to a 30 per cent rate, up from 20 per cent. Entities are subject to 35 per cent ABSD, plus a non-remittable additional 5 per cent for housing developers.

Huttons Asia senior director (research) Lee Sze Teck:

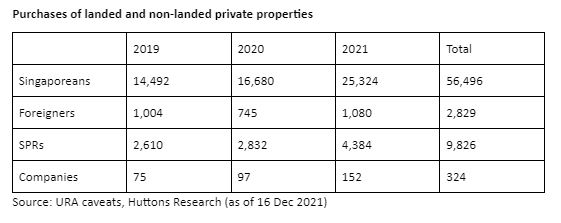

"The increase in ABSD, a form of wealth tax, is aimed at slowing down the flow of hot money into the property market. Singapore is a well-known safe haven because of its political stability and strong rule of law. Despite travel restrictions, the number of foreigners (including Singapore PRs) have shown a sharp increase in 2021 compared to 2020. The jump in the number of companies buying private properties is worrying."

"While first time buyers do not see an increase in tax payable, they will benefit from the slower price appreciation which ensures affordability."

"Quite a number of HDB upgraders sell off their HDB flats when they buy a new private property as they do not have the cash to pay ABSD upfront. Hence HDB resale volume could drop in the next 3 to 6 months as upgraders assess the situation. If conditions in the private market are stable and HDB resale prices maintain their growth momentum, upgraders are likely to cash out and upgrade to a private property."

Edmund Tie head of research and consulting Lam Chern Woon:

"The higher ABSD rates for Singaporeans and PRs purchasing their second (and beyond) property will impact property investment demand over the next few months."

"Despite the gradual easing of travel restrictions, the higher ABSD rates for foreigners will also moderate the recovery of foreign homebuying demand.

"Given the higher upfront taxes, investors will have to factor in an increasingly longer investment time horizon in decision making, and the eventual recovery will depend to a large extent on how the Covid pandemic has played out then."

OrangeTee & Tie senior vice-president of research and analytics Christine Sun:

"The new measures may impact investors more than owner-occupiers. Investors usually own more than 1 property and therefore will be affected by the increased ABSD."

"The measures may also affect PRs and foreign purchases. The number of condominiums bought by PRs and NPRs have been rising over the past few months. With VTLs and borders reopening further, we are expecting more PRs and foreigners to return to Singapore, and they may contribute to a higher demand for housing. Therefore, the latest round of measures may slow down demand."

PropNex Realty chief executive officer Ismail Gafoor:

"In our view, the 10 percentage-point increase in ABSD to 30 per cent for foreigners appear to be too harsh, seeing that foreign buyers have not been very active in the market this year, owing to the travel restrictions. Looking at the caveats lodged, foreigners accounted for only about 4.5 per cent of non-landed new private home sales this year - the majority of the demand was from Singaporeans."

Tighter TDSR

The TDSR threshold was tightened to 55 per cent, from 60 per cent previously. That means new mortgages cannot cause borrowers' total monthly loan repayments to exceed 55 per cent of their monthly income. The TDSR threshold for refinancing existing property loans granted before Dec 16, 2021 remains at 60 per cent.

Edmund Tie head of research and consulting Lam Chern Woon:

"The tighter TDSR limits of 55 per cent is a welcome move to improve the prudency of home purchases, especially amid an impending rate increase environment. The application of the new TDSR limits to mortgage equity withdrawal loans will also moderate the wealth effects from the recent property upswing."

ERA Singapore head of research and consultancy Nicholas Mak:

"The tightened TDSR will impact acquisitions of all types of properties and other loans."

"TDSR is now officially part of the cooling measures. When the TDSR framework was introduced in 2013, the government said it was not a cooling measure tool. Last night's announcement officially made it an instrument of cooling measures."

ALSO READ: Unable to meet TDSR and MSR limits? Here are 6 things you can do

Huttons Asia senior director (research) Lee Sze Teck:

"The tightening of TDSR to 55 per cent is a pre-emptive move to encourage financial prudence in case of a sudden increase in interest rates. In particular, purchases by Singaporeans have spiked in 2021. This will ensure households are not financially stretched/burdened should there be an increase in interest rates."

Realstar Premier founder William Wong:

"It is already common for buyers of landed housing to not get the maximum loan when making their purchases. So some of them may be affected by the TDSR reduction, but this will only be a very small group."

Reduced LTV limit for HDB loans

The LTV limit for HDB-granted loans was lowered to 85 per cent, from 90 per cent previously. This reduces the maximum amount potential homebuyers can borrow from HDB. The LTV limit for loans obtained from financial institutions to purchase HDB flats remains unchanged at 75 per cent.

Edmund Tie head of research and consulting Lam Chern Woon:

"The unchanged LTV limits for homebuyers taking mortgage loans (from banks) is a relief for first-time buyers starting their homes, where they currently need to fork out 25 per cent of the property price in cash or CPF. The government continues to practice a policy stance to shield first-time homebuyers from new cooling measures, especially when intentions of genuine family formation are at play."

Huttons Asia senior director (research) Lee Sze Teck:

"The reduction in LTV ratio for HDB loans to 85 per cent has little impact. Most buyers will opt for a loan from the banks as the interest rate is much lower than HDB's interest rate."

Timing of announcement

On July 5, 2018, the day the previous round of measures were announced, thousands of homebuyers thronged project showflats in the night as they rushed to put down deposits for units. Some developers also hastily launched sales earlier than planned.

ERA Singapore head of research and consultancy Nicholas Mak:

"The announcement was released at 11.40pm last night, to prevent a repeat of developers opening up their showflats in the night."

Huttons Asia senior director (research) Lee Sze Teck:

"This is the first time the government announced cooling measures which take effect within the next hour, giving buyers, sellers, developers and agents little to no time to react.

"It is a smart move considering that we are in the midst of a pandemic with a new variant and crowds or mass gatherings could increase the chances of another wave of infections. It will also reduce impulse buying just to avoid the new measures."

Overall impact and extent of the changes

OrangeTee & Tie senior vice-president of research and analytics Christine Sun:

"As the mid to high-end segments have a larger portion of investors and foreign buyers, those segments could be more affected by the measures, whereas mass-market housing has more first-time buyers, who will see a smaller impact."

"The cooling measures are meant to ensure homebuyers remain prudent in their property purchases and do not overstretch their finances. Although there are already measures put in place in the past, such as TDSR or MSR (mortgage servicing ratio), to ensure they do not overleverage, there could still be some pockets of buyers who may be overstretching their finances.

ALSO READ: Seller's Stamp Duty: Things to know before selling your property within three years

''This may include some families who have sold their flats and bought two private properties. Others may have taken up a maximum loan and did not leave enough buffer. Therefore, these measures will help to address some of these issues."

"There will likely be a knee-jerk reaction. We may see volumes slowing down for about six months. Prices may stabilise and rise at a much slower pace next year. "

CBRE head of research, Southeast Asia, Tricia Song:

"The cooling measures will help improve affordability for first-time homebuyers, prevent affluent buyers from buying additional properties for investment for future generations, and also reduce the risk of a hard landing when interest rates rise in the near future."

"In view of the limited new-launch pipeline in 2022, we expect new home sales to trend down from the current 13,000 units to a normalised 9,000 to 10,000 units, while prices could be flat or increase by 1 to 3 per cent in 2022. Secondary volumes should also normalise as prices stabilise, especially when owners with more than one property will incur higher ABSD when replacing the property."

ERA Singapore head of research and consultancy Nicholas Mak:

"The new cooling measures are very conservative."

PropNex Realty chief executive officer Ismail Gafoor:

"It is likely that developers may well take a breather and sit out the next one to two months to assess the impact of these measures on the market, and may decide to hold off launches till after Chinese New Year. This will also give prospective buyers some time to understand how the measures will affect them and reassess their buying options."

Huttons Asia senior director (research) Lee Sze Teck:

"As with all cooling measures, there will be a knee-jerk reaction immediately as everyone tries to understand and assess the impact. Sales in December 2021 are expected to slow down. New home sales could ease to between 400 and 600 in December, and project launches could be held back. Nevertheless, new home sales are still expected to be around 13,000 for 2021. Volume could ease in the next one to two quarters in 2022."

"While the cooling measures are expected to slow down price appreciation, there is little pressure on most developers to reduce prices."

"The en bloc market which just picked up pace in the last couple of months is likely to slow down. The risks to developers have been increased by 10 percentage points to 35 per cent should they fail to sell within five years. This is onerous on developers, and en bloc hopefuls have to temper their expectations to increase their chances of a successful collective sale. Developers will be more cautious in bidding for land, which will have a trickle-down effect on selling prices."

Realstar Premier founder William Wong:

"Generally the impact of the new measures will be felt more by the condo segment, and to a smaller extent HDB flat buyers."

"We expect slower activity in the property market for the next three months or so."

Edmund Tie head of research and consulting Lam Chern Woon:

"We expect property sales to moderate to about 11,000-12,000 units in 2022 from an expected stellar performance of over 13,000 units this year."

This article was first published in The Business Times. Permission required for reproduction.