The real financial cost of critical illnesses in Singapore

Battling a critical illness can be tough. It is a long-term affair and can put a large stress on one’s finances and emotional health.

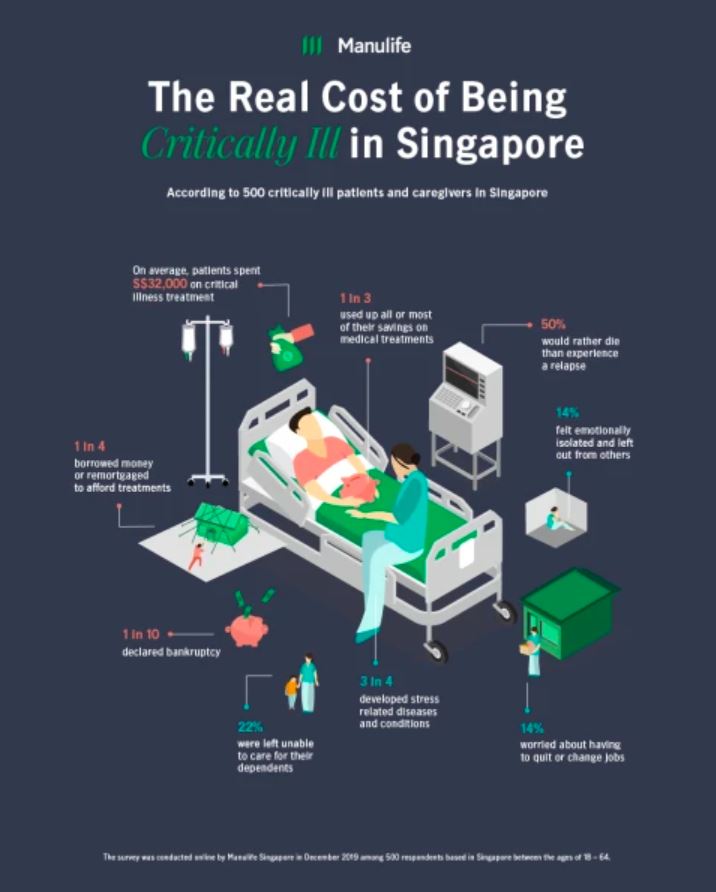

From the medical bills involved in the treatments for critical illnesses to facing difficulties with paying for necessities, it is no surprise that one in three of critical illnesses patients have spent all or most of their savings battling critical illnesses.

Ranked as the second most expensive country to live in, it is inevitable that the costs of healthcare in Singapore are costly as well. For those battling critical illnesses, it is not solely the one-time costs that they have to bear.

There are also long-term costs of treatment for critical illnesses involved. Between the emotional trauma and challenges and the financial distress one faces when critically ill, patients, as well as their loved ones, often find financial concerns the biggest challenge.

In a 2020 study conducted by Manulife, it was found that on average, critically ill patients spend S$32,000 on treatment while 15 per cent spent in excess of $50,000 or more.

With such a hefty sum spent on just their treatment, it leaves them with little to no money left for other expenses. Perhaps, this could be why 25 per cent of patients have had to borrow money or remortgage to pay off their bills.

But it’s not simply the cost of treatments that patients worry about. It is also the fear that they may end up losing their jobs once diagnosed. As the medical bills to pay in the future increase and yet, they face a declining source of income, it has been reported that six percent of patients have declared bankruptcy due to critical illnesses.

While Singaporeans may be eligible for subsidies and grants offered by the government, the reality is that such subsidies are typically insufficient.

The costs of critical illnesses can indeed be overwhelming. However, there is a solution that can help alleviate a significant amount of your financial burden.

As its name suggests, critical illness insurance provides coverage for life-threatening illnesses such as heart attack, stroke, cancer, and more.

As such medical emergencies incur a much higher cost than usual medical expenses, critical illness insurance plans provide payouts to help cover such costs. Currently, you have the option to purchase a standalone critical illness insurance plan or have it as an add-on to your life insurance plan.

Some insurers offer a multi-pay plan whereas others offer an accelerated plan. Read on to better understand their differences and which you should purchase.

For those new to critical illness insurance, these terms may sound foreign to you. However, in a bid to help you better understand such terms, we have included their key differences.

The main difference between the two is the number of claims and payouts offered. Easily inferred from the name, “multi-pay”, a multi-pay critical insurance plan offers multiple payouts whereas an accelerated plan only offers one.

For an accelerated plan, upon your diagnosis, your insurer will pay you a lump sum if you are diagnosed with a critical illness covered in your policy. After which, your insurance plan will be terminated.

On the other hand, multi-pay plans will provide coverage for recurring critical illnesses. Similar to an accelerated plan, upon your diagnosis, you will receive a payout from your insurer if you are diagnosed with a critical illness covered in your policy.

However, for multi-pay plans, your plan will not be terminated. As such, should you be diagnosed with another critical illness covered by your policy or suffer a relapse, you will be able to make another claim.

Having said that, do read the terms and conditions of your policy carefully to understand the percentage of the Sum Assured you will get to claim and the minimum period of time before you can make your next claim.

Due to the higher number of payouts offered under a multi-pay critical illnesses insurance plan, the premium that you will have to pay will generally be higher.

For a 35-year-old individual with a sum assured of $100,000, the costs of the various plan are as follows:

Whether you should get a multi-pay or accelerated plan is entirely up to your priorities. For individuals who prefer and can afford higher coverage and payouts, the multi-pay critical illnesses insurance plans are for you.

As previously mentioned, you will be able to make multiple claims under the multi-pay plan. This allows you to be covered for more than one critical illness.

As such, in the case where a critical illness can be genetically inherited, it is often recommended to get multi-pay plans as it has a high possibility of recurring. Nevertheless, in cases where your budget does not permit you to opt for a high coverage plan, you can consider getting a cancer insurance plan such as the MSIG Cancer Insurance instead.

Providing coverage for cancer only, the premiums that you will have to pay will be much lower. Thus allowing you to cut your expenses on insurance. Apart from cancer insurance, insurers in Singapore also offer heart attack and stroke insurance plans.

With such a financial safety net in place, in the unfortunate event that you are diagnosed with a critical illness covered by your policy, you may have a peace of mind that your finances would not take a blow. As such, you would not need to trouble your family to help you with finances.

Furthermore, the extra amount that you have saved with a critical insurance plan can be then used for long-term daily medical necessities that your policy does not cover but is required for your treatment.

Apart from enjoying more extensive coverage under the multi-pay plan, you will also be able to enjoy higher payouts in the long run.

Take Singlife with Aviva’s MultiPay Critical Illness Plan IV for instance.

|

Critical Illness (CI) Benefit |

Maximum total payout: 600 per cent of the sum assured |

|---|---|

| Upon diagnosis of the following: | |

| (a) Early or Intermediate Stage CI | 100 per cent of the sum assured (per claim) |

| (b) Severe Stage CI | 300 per cent of the sum assured less any claim paid for the early and intermediate stage of the same CI Group (per claim) |

|

Recurrent CI benefit |

Maximum total payout: 300 per cent of the sum assured |

|---|---|

| Upon diagnosis of the following: | |

| (a) any one of the 6 specified Severe Stage CIs covered (after the CI Benefit has ceased) | 100 per cent of the sum assured (per claim) |

| (b) any one of the 6 Recurrent CIs covered | 100 per cent of the sum assured (per claim) |

Under this plan, you will be entitled to up to 900 per cent of your sum assured, depending on your diagnosis. In comparison, accelerated plans such as those by FWD only offer a one-time 100 per cent lump sum cash payout.

As for individuals who have a tighter budget and prefer a much more straightforward plan, you can consider getting an accelerated plan instead.

As such plans provide lower payouts and cover a single critical illness, the premium is also much lower, making it suitable for those on a tighter budget.

Having said that, it is imperative to note that the premium you pay will depend on the following factors.

In general, the older you are, the more expensive the premium. This is due to the fact that older individuals often face a higher risk of contracting critical illnesses such as dementia and heart attacks as compared to younger individuals.

For those who smoke, have pre-existing conditions, a family history of a critical illness, have a high risk job, and lead a relatively high risk and unhealthy lifestyle, your insurance premium will be much higher. The basis of a higher premium is simply because you have a higher risk of contracting a life-threatening disease and would incur higher medical bills.

In the short-run, the lump sum payout will cover your medical bills should you be diagnosed with a critical illness. In the long-run, the lower premium paid will allow you to save a significant amount if you do not contract a critical illness.

Such a plan is also more suited for those with a lower risk medical history. For those with a lower risk family and individual medical history, the probability of contracting a critical illness is much lower, albeit not zero. Thus, the likelihood of needing multiple payouts due to relapse or contracting multiple critical illnesses is much lower.

You will also get an additional payout of up to 20 per cent of your sum assured upon diagnosis of 24 Special Conditions. Reach out to our advisors at PolicyPal if you want to learn more or are interested in purchasing any of these plans. It is one of the cheaper multi-pay critical illness plans on the market.

The other multi-pay plan is ManuLife Ready CompleteCare with the "cover again" add-on. ManuLife Ready CompleteCare offers a payout of up to 500 per cent of the sum assured for 36 critical illnesses and lets you claim up to six times per policy as long as each of the conditions are different. There is also a lump sum benefit of $25,000 when diagnosed with one of the 18 Special Conditions.

While some critical illness plans on the market focus on one illness to cover, such as cancer, there are plans that cover a multitude of illnesses. These plans can be a good option for people who want more robust coverage that covers all the bases of their health concerns.

| Amount Insured | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|

| $50,000 | $110.47 | $135.85 | $190.39 | $497.25 |

| $100,000 | $150.67 | $179.08 | $273.39 | $760.5 |

| $200,000 | $200.85 | $247.00 | $390.52 | $1,170.00 |

FWD's Big three Critical Illness Insurance can be a suitable peace of mind critical illness plan for people who want coverage for the three major illnesses affecting Singaporeans: Cancer, heart attacks and stroke. With 90 per cent of critical illness claims arising from these three conditions, FWD's Big three plan provides no-frills coverage for the most likely health events.

We found that FWD's premiums average to 50 per cent less than other standalone critical illness plans on the market. For an additional fee, you can also choose a heart condition and neurological disorder add-on that provides coverage for a variety of illnesses and necessary procedures including heart disease, bacterial meningitis, pacemaker insertion and primary lateral sclerosis.

Big three will provide a one-time full payout for detection of any stage of cancer or in the event of a heart attack of a specified severity and stroke that results in a permanent neurological deficit. FWD also provides a market beating $20,000 death benefit if you die while the policy is in force.

Another useful feature is that because this is a standalone policy and not a policy attached to a life insurance product, you can choose to renew your plan annually. You can renew your policy up until you turn 85 and you only have to answer one health declaration to purchase the policy without any medical examination required.

| Amount Insured | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|

| $50,000 | $127.46 | $156.75 | $219.68 | $573.75 |

| $100,000 | $173.85 | $206.62 | $315.45 | $877.50 |

| $200,000 | $231.75 | $285.00 | $450.60 | $1,350.00 |

FWD's Big three Critical Illness Insurance can be a suitable peace of mind critical illness plan for people who want coverage for the three major illnesses affecting Singaporeans: Cancer, heart attacks and stroke. With 90 per cent of critical illness claims arising from these three conditions, FWD's Big three plan provides no-frills coverage for the most likely health events.

We found that FWD's premiums average to 50 per cent less than other standalone critical illness plans on the market. For an additional fee, you can also choose a heart condition and neurological disorder add-on that provides coverage for a variety of illnesses and necessary procedures including heart disease, bacterial meningitis, pacemaker insertion and primary lateral sclerosis.

Big three will provide a one-time full payout for detection of any stage of cancer or in the event of a heart attack of a specified severity and stroke that results in a permanent neurological deficit. FWD also provides a market beating $20,000 death benefit if you die while the policy is in force.

Another useful feature is that because this is a standalone policy and not a policy attached to a life insurance product, you can choose to renew your plan annually. You can renew your policy up until you turn 85 and you only have to answer one health declaration to purchase the policy without any medical examination required.

| Amount Insured (Cancer) | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|

| $100,000 | $42.80 | $75.33 | $260.22 | $719.04 |

MSIG's CancerCare Plus is a critical illness insurance plan that provides $100,000 of cancer coverage and an accelerated benefit of $50,000 for early stage cancer. This means that upon early-stage diagnosis, you'll get 50 per cent of the sum assured and upon a major cancer diagnosis, you'll get the other 50 per cent.

It is most affordable for millennial customers, with premiums that range between 47 - 64 per cent less than MSIG's competitors. It is easily accessible, since you can buy this plan online and with just three simple health declarations. You can purchase this plan if you're between the ages of 20 and 64, but it's automatically renewable until you turn 84.

While CancerCare Plus is affordable for most age groups, it does cost above average for older consumers (ages 50 - 64). Furthermore, the level of coverage may be underwhelming for people who are looking for high levels of coverage across all stages of cancer. Thus, this plan is best suited as a contingency plan for young, healthy individuals.

| Amount Insured (Cancer) | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|

| $100,000 | $42.80 | $75.33 | $260.22 | $719.04 |

MSIG's CancerCare Plus is a critical illness insurance plan that provides $100,000 of cancer coverage and an accelerated benefit of $50,000 for early stage cancer. This means that upon early-stage diagnosis, you'll get 50 per cent of the sum assured and upon a major cancer diagnosis, you'll get the other 50 per cent.

It is most affordable for millennial customers, with premiums that range between 47 - 64 per cent less than MSIG's competitors. It is easily accessible, since you can buy this plan online and with just three simple health declarations. You can purchase this plan if you're between the ages of 20 and 64, but it's automatically renewable until you turn 84.

While CancerCare Plus is affordable for most age groups, it does cost above average for older consumers (ages 50 - 64). Furthermore, the level of coverage may be underwhelming for people who are looking for high levels of coverage across all stages of cancer. Thus, this plan is best suited as a contingency plan for young, healthy individuals.

With cancer being the top cause of death in 2019, it is best that we protect both ourselves and our wallets by purchasing critical illness insurance, be it a multi-pay or accelerated plan.

Having seen the financial distress that critically ill patients and their caregivers face, it is evident that a critical illness insurance plan can greatly lessen the financial burden one faces in the event that they are diagnosed with a critical illness. Without having the financial burden on both you and your family, it can no doubt allow you to have peace of mind.

Want to be protected? Find out more about the plans using our comprehensive analysis of critical illnesses insurance plans in Singapore!

This article was first published in ValueChampion.