Saving up for retirement: How much time do I have to save up?

PHOTO: Pixabay

Put aside all the “propaganda” you see online today on investing, trading and fanciful financial products. The first step towards financial freedom should always start with savings.

To answer this question, allow us to visualise your life in front of you.

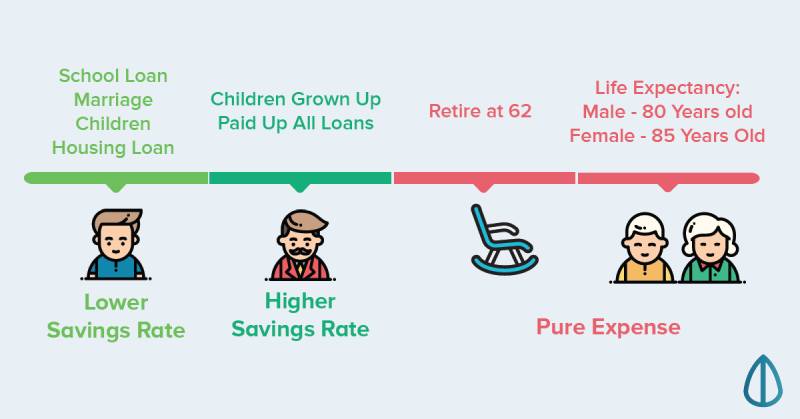

Instead of coming out with an absolute amount of savings, we base the savings amount on your individual yearly expense. This amount varies for each individual depending on the lifestyle which one chooses to lead.

To give a good projection of how much one needs to save, we took into account these factors:

| The age that one starts working | Years to save up for retirement (retire at 62) |

Years to enjoy retirement | |

|---|---|---|---|

| Male Diploma Graduate (after NS) |

22 | 40 | 18 |

| Male Fresh Graduate | 26 | 36 | 18 |

| Female Diploma Graduate | 20 | 42 | 23 |

| Female Fresh Graduate | 24 | 38 | 23 |

Using a male fresh graduate as an example. A male fresh graduate will have the least time to save (36 years to save up 18 years worth of expense).

From there, we work backwards to give a projection of how much you should have saved by a certain age.

To get an exact number, simply use:

(How much you need to survive per year) X (Number of years)

| Age (Male Fresh Graduate) |

Savings Rate | Annual Expenses Saved |

|---|---|---|

| 26-30 | Low Salary Clearing Loans (Very Low) |

At least 6 Months |

| 31-35 | Marriage Housing Loan (Low) |

At least 1 Year |

| 36-40 | Kids Education Housing Loan (Low) |

3-6 Years |

| 41-45 | Kids Education (Low) |

4-8 Years |

| 46-50 | Realised you need to SAVE for retirement! (High) |

6-10 Years |

| 51-55 | Debt free (High) |

7-12 Years |

| 56-62 | Retirement Planning (High) |

At least 18 Years |

| Target at age 62: | At least 18 | |

Taking life expectancy into account, females tend to live longer than their male counterparts.

With this, female face a steeper saving slope due to the need to save an additional 5 more years worth of expense.

| Age (Female Fresh Graduate) |

Savings Rate | Annual Expenses Saved |

|---|---|---|

| 22-25 | Low Salary Student Loans (Very Low) |

At least 6 Months |

| 26-30 | Low Salary Student Loans (Very Low) |

At least 2 Years |

| 31-35 | Marriage Housing Loan (Low) |

At least 6 Years |

| 36-40 | Kids Education Housing Loan (Low) |

8-11 Years |

| 41-45 | Kids Education (Low) |

9-13 Years |

| 46-50 | Realised you need to SAVE for retirement! (High) |

11-15 Years |

| 51-55 | Debt free (High) |

12-17 Years |

| 56-62 | Retirement Planning (High) |

At least 23 Years |

| Target at age 62: | At least 23 | |

Do take note if you fall within the below demographic:

97per cent of middle to high-income earners above the age of 25 years old are saving between 30per cent to up to 49per cent of their salary. How much of your salary are you saving?

Assuming your determination to save up brought you down so “far” this article, here’s a simple exercise to determine your saving rates.

Taking into account that different individual has different

A good exercise to determine your best saving rate is

This article was first published in Seedly. All content is displayed for general information purposes only and does not constitute professional financial advice.