Should you invest with robo advisors?

With the improvement in artificial intelligence, it was only a matter of time before robots started managing money. Today, robo advisors are becoming commonplace among retail investors.

Even traditional banks such as DBS are beginning to embrace the power of artificial intelligence as a wealth management platform.

But should you trust a "robot" to manage your hard-earned money? With that in mind, I map some of the advantages and downsides of using a robot-assisted wealth management tool.

WHAT REALLY ARE ROBO ADVISORS?

Robo advisors are digital platforms that personalise the investor's portfolio using an algorithmic-driven approach with little human supervision.

The process is really quite simple. Investors register for an account on the robo advisor's platform. They then answer a few questions that help the robo advisor understand the individual's financial goals and risk tolerance.

Using an algorithm, the robo advisor then advises the clients on a suitable portfolio for them.

Usually, robo advisors have a fixed list of Exchange Traded Funds (ETFs) or funds that it can choose from to build the client's portfolio. These funds, in turn, invest in a variety of assets, such as stocks, bonds, or real estate.

One thing to note, these funds are actually mostly managed by humans! So robo advisors simply help to allocate your wealth to the funds that it thinks suits your needs and goals.

WHAT ARE THE FEES INVOLVED?

[[nid:466479]] Robo advisors usually charge just a basic annual advisory fee that is a small percentage of the total assets under management.

For instance, Morgan Stanley's Access Investing charges a fee of 0.35 per cent per annum, while DBS digiPortfolio charges an annual fee of between 0.75 per cent and 0.85 per cent.

But to be clear, this does not include the fees related to owning shares of mutual funds and exchange-traded funds. I will explain more on this later.

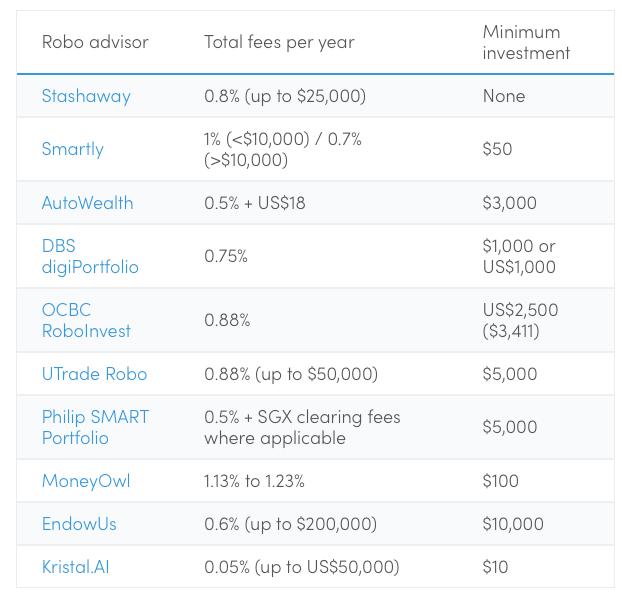

The table below shows the fees charged by the prominent robo advisors in Singapore.

WHY INVEST WITH ROBO ADVISORS?

The beauty of robo advisors is that it removes emotional misjudgments and other possible conflicts of interest from the decision-making process.

The robo advisors use a methodological process that is immune to emotion and is not influenced by commission-related fees.

They are also really simple to use. The set up is usually a seamless process and the minimum outlay to invest can be fairly small.

They also offer regular statements that will give investors up-to-date information on how their investments are performing and keep track of all additional cash flows.

In addition, robo advisors can automate the rebalancing of the portfolio for the client. This removes the hassle of actively managing your portfolio and reallocating it manually every few quarters.

POTENTIAL PAIN POINTS

But as with any product, there are also things not to like about robo advisors.

Robo advisors only offer a few different fixed portfolios. It is not possible to deviate from these fixed portfolios. After answering a few questions, the robo advisor will recommend one of the fixed portfolios that they have built. Investors cannot deviate from these fixed portfolios and are not able to access funds that are not offered on the platform.

On top of that, the robo advisor's advisory fee is an additional cost. As mentioned earlier, investors have to pay the advisory fee, on top of the total expense ratio of the funds that they invest in through the robo advisor.

Although the robo advisory fee is usually less than a percentage point, it quickly adds up over the years.

[[nid:469532]]

IS IT RIGHT FOR YOU?

Ultimately, the fewer potential conflicts of interest and the fee-based structures make robo advisors a robust wealth management tool that has the client's interest at the forefront.

However, they still have their limitations. If you want a more personalised portfolio, the limited number of portfolio constructions in a robo advisor platform may not be sufficient.

Many of the robo advisors also only offer ETFs on their platform. As a result, it may not be useful for investors who want exposure to more aggressively-managed active funds, which have the potential for higher returns.

All things considered, I believe investors who want a simple stress-free passive investment strategy can consider using robo advisors. More savvy investors who are willing to do some research on funds should have a more hands-on approach to save costs and gain access to better-performing funds in the market.

This article was first published in The Good Investors. All content is displayed for general information purposes only and does not constitute professional financial advice.