Singapore's most defensive stocks for the first half of 2020

An SGX sign is pictured at Singapore Stock Exchange on July 19, 2017.

PHOTO: Reuters

The first half of 2020 (“1H20”) saw sharp economic contractions across the world with lockdowns containing the spread of COVID-19 to 10 million people with a 4.9 per cent mortality rate.

The social and economic costs of containment saw extraordinary policy responses across the globe. This included the ramping up of healthcare services and supplies, social quarantines and economic confinements, with strong fiscal and monetary stimulus.

The coincidence of these big economic measures meant they were highly synchronised, with $11 trillion in global fiscal stimulus (13 per cent of global GDP) and fast moving Federal Reserve-led, extraordinary monetary policy initiatives.

The urgency with which the Federal Reserve brought short-term US Dollar volatility back from near 2008 highs, generated stability in bellwether US Treasuries Yields, and by extension, demand for global stocks.

The monetary transmission mechanism appeared to offer some offset to the global stock market in the face of the hard economic challenges of the measured slowdown.

From the end of 2019 through to the March 23 intraday low, the FTSE World Index in USD terms declined 33.3 per cent, before rebounding 39.0 per cent from March 23 to June 30, to generate an overall decline of 7.0 per cent for the 1H20. Two of the best performing sectors in 1H20,

[[nid:491682]]

Technology and Healthcare, make up as much 33 per cent of the weightage of the FTSE World Index, in addition to making up 42 per cent of the S&P 500 Index.

By comparison, Technology and Healthcare makes up a much less 6 per cent of the weightage of the FTSE ASEAN All-Share Index, which declined 19.9 per cent in USD terms in 1H20.

Similar to Singapore, Banks and Real Estate are by far the biggest Sectors of the FTSE ASEAN All-Share Index. Globally, the top quartile of listed banks by market value generated a median decline of 21 per cent in total return (in SGD terms), with the top quartile of global Real Estate stocks generating a median decline of 16 per cent.

This saw the 1H20 declines of the both the Straits Times Index (“STI”) and the FTSE ASEAN All-Share Index anchored between the global performance of the two sectors.

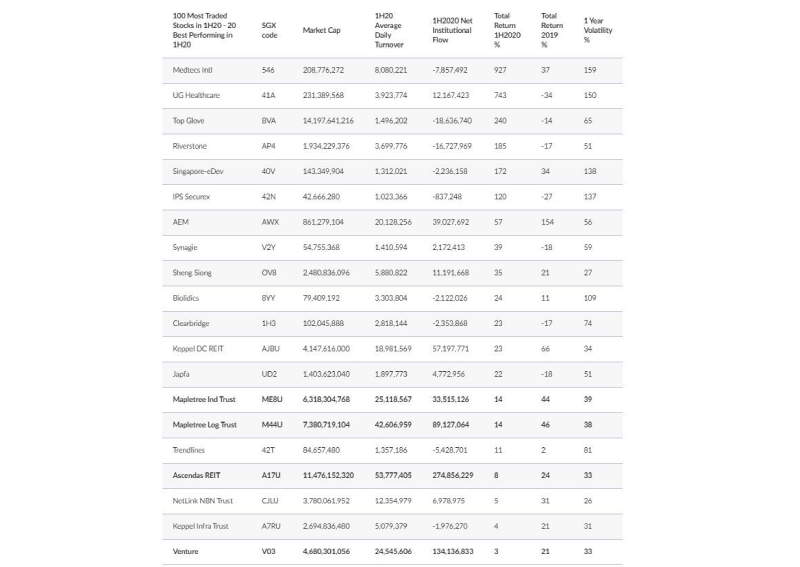

While the foundations of the heavyweight Bank and Real Estate sectors are clearly evident, Singapore’s stock market is also highly diversified. Of Singapore’s 100 most traded stocks by turnover in 1H20, the 20 most defensive performances, included four current STI constituents and are tabled below.

Similar to the aforementioned global benchmarks, Technology and Healthcare stocks were amongst the strongest performers in the stock market.

As detailed in the table, the strongest segments of the Healthcare Sector were the manufacturers and distributors of medical equipment and supplies, also observed across the global Healthcare Sector.

Likewise in Technology, the pick-up in global digitalisation supported stocks with exposure to internet enterprises and cloud providers, including Keppel DC REIT, Mapletree Industrial Trust and NetLink NBN Trust in Singapore.

Small cap stocks also featured in the 20 stocks with as many as four stocks ranking in the top 100 stocks by turnover, yet currently maintaining market capitalisation of less than $100 million.

Three of the six REITS that make up the STI were amongst the 20 most defensive performers tabled above - Mapletree Industrial Trust, Mapletree Logistic Trust and Ascendas REIT.

Increased market volatility impacted REITS in 2020, seeing increased trading activity by active investors looking more to REITs for momentum than stable returns.

Retail Investors returned as net buyers of the wider group of Singapore REITs and added to REIT ETF positions, after the major market lows on March 23, possibly on valuations rather than yields.

The upshot of this was that REITs continue to represent 26 per cent of the total stock market turnover in the first half of 2020, while maintaining 12 per cent of the $817 billion in total stock market capitalisation.

Businesses deemed as suppliers of essential products or essential services have continued to operate through 1H20.

Venture Corporation is amongst Singapore’s largest manufacturing companies and as tabled above was the STI’s best performing company in 1H20 with a defensive 3 per cent total return.

The company noted that by the end April, most if not all of its operating entities received exemptions to operate without headcount or working hours constraints.

As such, the supply side of its businesses had resumed operations while continuing to comply with all safety and precautionary measures for employees who work on sites.

In its 1Q20 Business Update management noted (click here for more) Venture Corporation noted some realignment of the global supply chain seems inevitable, and this presents opportunities for the Venture Group, with potential beneficiaries of these opportunities are its entities in Singapore and Malaysia.

From a pure data perspective, context for the sharp contractions in 1H20 GDP, employment, and the key sectors of retail, services and industrials, will come in 2H20 and into 1H21 on the proviso social and economic containments continue to be lifted.

[[nid:491021]]

The optimistic adage of its not how hard you fall, but how high you bounce will be one perspective applied to the next six months of global economic releases.

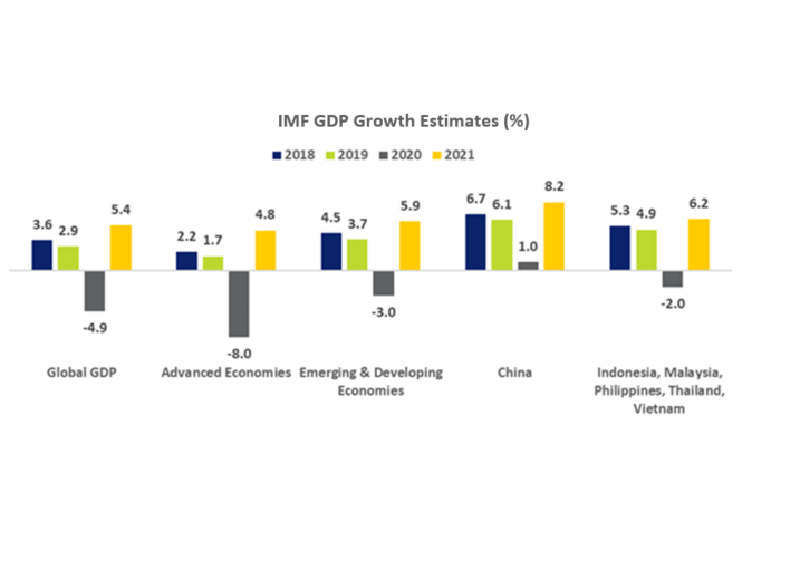

While the IMF estimate global GDP to decline 4.9 per cent in 2020, it is expected to rebound 5.4 per cent in 2021. As illustrated below, advanced economies are leading both the swings in GDP declines in 2020 and estimated GDP growth in 2021.

At -4 per cent to -7 per cent, Singapore’s GDP growth forecast for 2020 is in-line with the global and advanced economy estimates. Unity, Resilience, Solidarity and Fortitude Budgets are now providing fiscal stimulus measures equivalent to around 20 per cent of Singapore’s GDP, which is among the largest proportions across the world with the global average at 13 per cent.

Looking forward, the key economic risk not just for the United States, but indeed the World, was conveyed by Federal Chair Powell on May 17 in a 60 minutes interview - if GDP is to move back up, after the very low numbers in the June quarter, and unemployment is to come down, the big thing the country has to do is avoid a second wave of the virus over the next couple months.

Hence, a current market focus is the spike of Covid-19 cases in the United States, in addition to the Federal Reserve not dismissing Yield Curve Targets to further its supportive measures.

This article was first published in Investor-One.