We own a Normanton Park condo and make $285k per year: Should we sell to invest in stocks and rent or buy a resale unit?

PHOTO: Stackedhomes

Hi Stackedhomes,

My husband and I have been avid readers of your content, and we notice your team has been very detailed in analysing situations to provide sound choices. I hope you can help us as we are quite lost with what to do, and most realtors we speak to have their agendas and I dont blame them.

I am 33 years old, and my husband is 34. We both are self-employed and do not contribute to CPF, We have a combine income of about $285,000 after tax. We have a new born four months old.

We bought Normanton Park in early 2021, and it TOP recently. However, the home is too small for our helper and newborn, as we did not plan for a child back then. If we sold the Condo, we will have excess $600,000 in cash. So my dilemma is, should I invest the $600,000 into a diversified stock and bond portfolio, and rent a 3br condo or should I buy a resale 3BR condo?

What I like about having a $600,000 stock portfolio, is the liquidity and the potential income it pays me, and also the potential to compound the money. While I can do the same in the housing market, I feel that interest rates are expensive, and property prices are less likely to increase at a rate to give me financial freedom.

I would ideally want to live in the bishan-thomson area, because I hope to send my newborn to AITONG SCHOOL which is located at bright hill drive. So if we can take reference to location I think that will be a good place to use as reference to do the analysis.

My monthly expenses for car is $3000, Household expenses is $1,500, helper is 750, personal expenses is 2,500, and expenses on child is about 1000 , total about $8,750 a month combine, this is about $105000 a year.

This excludes loan repayment for Normanton Park. Please advise.

Hi there!

Thank you for writing in and we appreciate your continued support!

We understand the challenge of trying to optimise your cash reserves in the present environment of elevated interest rates, particularly when considering the purchase of a property. It’s understandable that you may be contemplating the most effective means of leveraging your assets to achieve the highest possible profitability.

Opting for investments in stocks and bonds, rather than real estate, represents a distinct adjustment in your investment approach. Each option carries its own distinct advantages and factors to weigh.

For example, stocks and bonds are well-known for their liquidity and the potential for swift wealth accumulation via market appreciation or interest earnings. On the other hand, choosing to invest in property presents a different set of advantages, including the security of a tangible asset, potential capital appreciation, and the possibility of rental income.

We will start by looking at your affordability before we go into the options you’re considering.

You probably know this already, but for others reading this — when it comes to calculating your mortgage loan, there will be a 30 per cent reduction on your taxable income since both of you are self-employed.

| Description | Amount |

| Maximum loan based on ages of 33 and 34, combined annual income (self-employed) of $285K, monthly car loan of $3K and at an interest rate of 4.6per cent | $1,783,644 |

| Cash | $600,000 |

| Maximum affordability based on 25 per cent down payment + BSD of $600K | $2,101,333 |

Let’s now look at the options you’re considering.

We will start by looking at some differences in investing in stocks and shares as compared to property.

Both stocks and shares and property investment offer unique opportunities and challenges. The choice often depends on your financial goals, risk tolerance, investment horizon, and personal preferences. Diversification across both asset classes could be a strategy to consider, as it can potentially mitigate the risks associated with either option alone. It's important to conduct thorough research, consult with professionals, and align your investments with your long-term financial objectives.

Considering that you have a newborn and are planning for your child to enrol in Ai Tong School, we are assuming that you intend to remain in the next property until your child completes primary school, which is a minimum of 12 years.

Should you decide to rent instead, you won't need to immediately relocate to a location within 1km of the school, as there are still some ways to go before the P1 registration. During this interim period, you have the option to rent a place elsewhere, which might be more budget-friendly. Given that you have your own transportation, we can presume that a location less accessible by public transport may not pose a significant inconvenience.

Currently, the most affordable 3-bedroom condo available for rent that's of a decent size is listed at $3,600/month at Orchid Park Condominium. So far this year, there have been 35 3-bedroom transactions in this condo at an average rental rate of $3,834, so we'll assume that you manage to rent it for $3,600. We will assume this to be the rental cost for the next five years.

When examining developments within 1km of Ai Tong School, the most budget-friendly option is Bishan Park Condominium. In the last three months, the average rent for a 3-bedroom unit there was $4,850/month. We can assume this rental rate for the seven years from the time your child turns six to 12 years old, as there is a minimum 30-month stay requirement after the P1 registration for children who gain priority admission based on the proximity of their home to the school.

Cost incurred if you were to rent for the next 12 years:

| Description | Amount |

| Renting at Orchid Park Condominium for 5 years at $3,600/month | $216,000 |

| Renting at Bishan Park Condominium for 7 years at $4,850/month | $407,400 |

| Total cost | $623,400 |

Assuming a 100per cent stock portfolio, let’s assume a Return On Investment (ROI) of seven per cent to project the potential profits if you were to invest the $600,000 in stocks and shares over a period of 12 years.

| Time period | Investment amount | Gains |

| Starting point | $600,000 | $0 |

| Year 1 | $642,000 | $42,000 |

| Year 2 | $686,940 | $86,940 |

| Year 3 | $735,026 | $135,026 |

| Year 4 | $786,478 | $186,478 |

| Year 5 | $841,531 | $241,531 |

| Year 6 | $900,438 | $300,438 |

| Year 7 | $963,469 | $363,469 |

| Year 8 | $1,030,912 | $430,912 |

| Year 9 | $1,103,076 | $503,076 |

| Year 10 | $1,180,291 | $580,291 |

| Year 11 | $1,262,911 | $662,911 |

| Year 12 | $1,351,315 | $751,315 |

Total profits if you were to invest your cash proceeds of $600K while renting a 3-bedder for the next 12 years: $751,315 - $629,400 = $121,915

Because the rental expenses are rather substantial, they significantly reduce the profits generated from your investment in stocks and shares.

Do note that this profit is highly dependent on achieving consistent returns of seven per cent year on year over a 12-year period.

But that's on a 100 per cent stock portfolio. If you have a mix of stocks and bonds, we can assume a lower return (albeit one that's more stable). Let's assume a four per cent rate of return here:

| Time period | Investment amount | Gains |

| Starting point | $600,000 | $0 |

| Year 1 | $624,000 | $24,000 |

| Year 2 | $648,960 | $48,960 |

| Year 3 | $674,918 | $74,918 |

| Year 4 | $701,915 | $101,915 |

| Year 5 | $729,992 | $129,992 |

| Year 6 | $759,191 | $159,191 |

| Year 7 | $789,559 | $189,559 |

| Year 8 | $821,141 | $221,141 |

| Year 9 | $853,987 | $253,987 |

| Year 10 | $888,147 | $288,147 |

| Year 11 | $923,672 | $323,672 |

| Year 12 | $960,619 | $360,619 |

These returns would result in a loss of $360,619 – $629,400 = -$268,781.

While predicting the future direction of the stock market is speculative, there’s an inherent risk to maintaining a heavily stock-weighted portfolio. A potential financial downturn in the next decade could jeopardise your investment significantly more than the scenarios depicted earlier.

Although such an occurrence might be rare, it’s not impossible. This risk becomes even more pronounced if you need to liquidate your portfolio during this downturn, for instance, to buy a home. Furthermore, as you age, your loan eligibility decreases, meaning you might not secure as favorable loan terms as you could have earlier.

So let’s explore what happens if you decide to purchase a three-bedder instead.

There are just a handful of developments located within 1km of Ai Tong School, however, with a budget of $2.1 million for a 3-bedder, your options are further restricted. At the moment, there are two projects with units that fall within your affordability.

| Project | Tenure | Completion year | Unit type | Size (sqft) | Asking price |

| Bishan Park Condominium | 99 years | 1994 | 3b | 1,292 | $1,850,000 |

| The Gardens at Bishan | 99 years | 2004 | 3b | 1,152 | $2,077,777 |

Let’s take a quick look at how these two projects are performing.

| Year | Bishan Park Condominium | YoY | The Gardens at Bishan | YoY |

| 2012 | $797 | – | $954 | – |

| 2013 | $912 | 14.43per cent | $1,093 | 14.57per cent |

| 2014 | $870 | -4.61per cent | $1,016 | -7.04per cent |

| 2015 | $888 | 2.07per cent | $1,024 | 0.79per cent |

| 2016 | $868 | -2.25per cent | $986 | -3.71per cent |

| 2017 | $863 | -0.58per cent | $1,015 | 2.94per cent |

| 2018 | $902 | 4.52per cent | $1,044 | 2.86per cent |

| 2019 | $969 | 7.43per cent | $1,083 | 3.74per cent |

| 2020 | $1,031 | 6.40per cent | $1,129 | 4.25per cent |

| 2021 | $1,080 | 4.75per cent | $1,218 | 7.88per cent |

| 2022 | $1,143 | 5.83per cent | $1,415 | 16.17per cent |

| Annualised | – | 3.67per cent | – | 4.02per cent |

Looking at the table, it’s evident that despite the relatively older age of these two projects, their prices have remained resilient. Their price trends align with the overall market, which experienced a decline following the implementation of three rounds of cooling measures in 2013 but began to recover in 2017.

Their appeal likely stems from their proximity to Ai Tong School and their more affordable pricing compared to newer or freehold developments nearby, contributing to sustained demand.

This also coincides with a recent article we did on older leasehold condos versus freehold ones, in that leasehold developments don’t actually underperform freehold ones of an equivalent age (at least up until they reach a really old age).

However, it’s important to consider that a 12-year holding period is quite long, and by then, these two projects will have aged to over 30 and 40 years old. Given that they are 99 year leasehold projects, it’s not unreasonable to anticipate some degree of stagnation or depreciation in value.

Nevertheless, let’s say you were to purchase a unit at The Gardens at Bishan. There have been three three-bedders that changed hands this year in the development at an average price of $1,912,000. We will assume this to be the purchase price.

| Description | Amount |

| Purchase price | $1,912,000 |

| BSD | $65,200 |

| 25per cent down payment | $478,000 |

| Loan required | $1,434,000 |

Cost incurred if you were to purchase a 3-bedder and hold it for 12 years:

| Description | Amount |

| BSD | $65,200 |

| Interest expense (based on loan of $1,434,000 at 4.6per cent interest, with 30 year tenure) | $703,097 |

| Property tax | $39,720 |

| Maintenance fee (assuming $400/month) | $57,600 |

| Total costs | $865,617 |

Employing the annualised growth rate of private properties observed over the past decade, which stands at 2.21 per cent, we will perform a basic projection. It’s essential to bear in mind that this projection is based on the general market performance and the figures may fluctuate depending on market conditions.

The purpose of this projection is purely to provide a general reference so that you can better understand which strategy is best suited for you, rather than focusing on potential capital gains of individual developments.

| Time period | Property price | Gains |

| Starting point | $1,912,000 | $0 |

| Year 1 | $1,954,255 | $42,255 |

| Year 2 | $1,997,444 | $85,444 |

| Year 3 | $2,041,588 | $129,588 |

| Year 4 | $2,086,707 | $174,707 |

| Year 5 | $2,132,823 | $220,823 |

| Year 6 | $2,179,958 | $267,958 |

| Year 7 | $2,228,136 | $316,136 |

| Year 8 | $2,277,377 | $365,377 |

| Year 9 | $2,327,707 | $415,707 |

| Year 10 | $2,379,150 | $467,150 |

| Year 11 | $2,431,729 | $519,729 |

| Year 12 | $2,485,470 | $573,470 |

Total losses if you were to purchase a 3-bedder and live in it for the next 12 years: $865,617 – $573,470 = -$292,147

Given that the interest rate is higher than the rate of appreciation, the total cost is more than the profits made. Let’s look at how the interest rate will affect the potential profits.

| Interest rate | Cost incurred | Gains/losses |

| 2.5per cent | $529,158 | $44,312 |

| 3per cent | $607,214 | -$33,744 |

| 3.5per cent | $686,626 | -$113,156 |

| 4per cent | $767,295 | -$193,825 |

| 5per cent | $932,007 | -$358,537 |

We can see that it’s only when interest rates decrease to 2.5 per cent that you begin to observe some profitability.

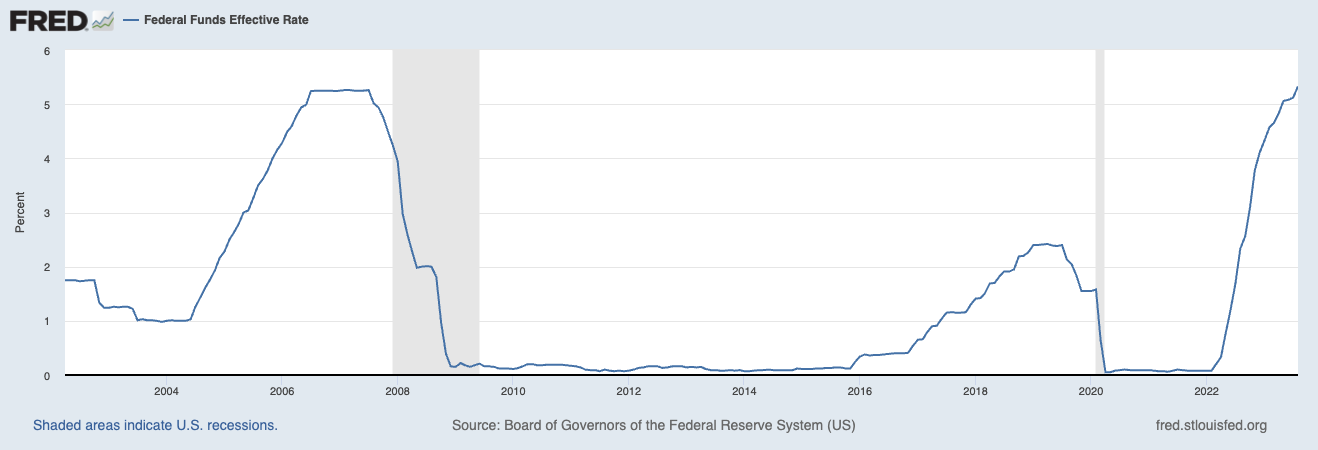

It’s worth noting that historically, interest rates do not tend to stay high for extended periods of time. They’re usually met with some form of economic slowdown which calls for lower interest rates. Here’s a quick look at the historical Fed Funds Rate in the last 20 years:

Do also note that we’ve used a conservative interest rate of 4.6 per cent based on on-the-ground information from banks in calculating your affordability. However, we’re aware that today, you can get a fixed 2-year rate for around 3.4 per cent.

On a $1.434 million loan, this translates to around $4,000 of interest payments per month which is close to your rental cost. So even in the current high-interest rate environment, the interest cost is close to the cost of renting — albeit around 10per cent more.

As such, it could be prudent to wait until interest rates are lower.

Another aspect to consider is the growth rate of the project. If it exceeds 2.21 per cent, as we’ve seen in the table above with both developments having outperformed this rate over the last decade, there is potential for profits even with higher interest rates.

This may be the case for older leasehold condominiums near Ai Tong. Considering the popularity of the school and how built-up the area already is, the lack of affordable condo supply may very well ensure that both Bishan Park Condominium and The Gardens at Bishan remain highly relevant.

Looking at the area, you’ll see that most homes within the 1km radius are landed homes (very low-density). The radius does not cover a wide number of HDBs as well which tend to be very densely populated. Overall, this could explain why both old leasehold condos (and perhaps other condos in the area) were able to outperform the general property market in the past 10 years.

However, as previously mentioned, 12 years is a substantial time frame, and considering these are 99-year leasehold projects, it’s prudent to anticipate that prices may plateau or decrease as they mature.

An alternative you can explore is to purchase a unit to rent out, while renting somewhere that is within 1km of Ai Tong School. Seeing as your holding period is relatively long, buying a freehold/999-year leasehold development could be a good option given that their prices generally tend to hold up in the long run.

Here are some available freehold/999-year leasehold units that fall within your affordability:

| Project | District | Tenure | Completion year | Unit type | Size (sqft) | Asking price |

| Hillview Heights | 23 | Freehold | 1996 | 2b2b | 958 | $1,650,000 |

| The Sunny Spring | 14 | Freehold | 1998 | 3b | 1,195 | $1,880,000 |

| The Tessarina | 10 | Freehold | 2003 | 2b2b | 926 | From $1,888,000 |

Let’s say you were to get a 3-bedder at The Sunny Spring and stay there for 5 years before renting a unit that is within 1km of Ai Tong School. From January till date, there were four 3-bedroom transactions in the development with an average price of $1,715,222. Let’s assume this to be the purchase price. Over the last 3 months, from May to July, the average rent for a 3-bedder in the project is at $4,266, which we will use as the rental price.

| Description | Amount |

| Purchase price | $1,715,222 |

| BSD | $55,361 |

| 25per cent down payment | $428,806 |

| Loan required | $1,286,416 |

The cost incurred if you were to purchase a 3-bedder and live in it for five years before renting it out and renting a place near Ai Tong School for your own stay:

| Description | Amount |

| BSD | $55,361 |

| Interest expense (based on loan of $1,286,416 at 4.6per cent interest, with 30 year tenure) | $630,736 |

| Property tax | $71,468 |

| Maintenance fee (assuming $400/month) | $57,600 |

| Rental income (for 7 years at $4,266/month) | $358,344 |

| Agency fee (payable once every 2 years) | $18,428 |

| Rental expense (for 7 years at $4850/month) | $407,400 |

| Total costs | $882,649 |

Similarly, we will use the annualised growth rate of 2.21per cent to do a simple projection:

| Time period | Property price | Gains |

| Starting point | $1,715,222 | $0 |

| Year 1 | $1,753,128 | $37,906 |

| Year 2 | $1,791,873 | $76,651 |

| Year 3 | $1,831,473 | $116,251 |

| Year 4 | $1,871,948 | $156,726 |

| Year 5 | $1,913,319 | $198,097 |

| Year 6 | $1,955,603 | $240,381 |

| Year 7 | $1,998,822 | $283,600 |

| Year 8 | $2,042,996 | $327,774 |

| Year 9 | $2,088,146 | $372,924 |

| Year 10 | $2,134,294 | $419,072 |

| Year 11 | $2,181,462 | $466,240 |

| Year 12 | $2,229,672 | $514,450 |

Total losses if you were to purchase a 3-bedder and live in it for five years before renting it out and renting a place near Ai Tong School for your own stay: $882,649 – $514,450 = $368,199

Here, apart from the interest expenses, there are additional costs such as agency fees, and the property tax obligation is higher when the unit is rented out. Furthermore, if the rental income doesn’t fully cover the rental expenses, it will necessitate a monthly top-up. Unless the rental income can sufficiently offset the property tax, agency fees, and your rental expenses, it could result in greater losses compared to Option 2.

In this scenario, you’re banking on the property’s capital appreciation to help offset these costs. To ensure a fair comparison, we’ve applied the same annualised growth rate as Option 2, but let’s examine how this growth rate affects the overall gains or losses.

| Annualised growth rate | Capital appreciation | Gains/losses |

| 1.5per cent | $388,850 | -$551,680 |

| 2.5per cent | $685,570 | -$254,960 |

| 3per cent | $846,327 | -$94,202 |

| 3.5per cent | $1,015,902 | $75,372 |

At a growth rate of 3.5 per cent, you’ll begin to realise some gains. Hence, with this choice, making a well-informed property selection is of utmost importance.

Based on our calculations, investing the $600K in stocks while renting a property appears to yield the highest profits over a 12-year period.

However, again, it’s important to note that the potential returns from stocks will vary, depending on your risk tolerance. Investing in a more stable portfolio, and hence achieving a lower return results in a loss that’s closer to what you get if you bought a 3-bedroom today. It might even be worse if the condo outperforms the general property market as it has over the past 10 years.

So when it comes to whether you should invest in stocks/bonds and renting versus buying today, it boils down to a couple of things:

Then there are other intangibles to consider:

We also explored the option of purchasing a property for rental while you continue to rent a place near Ai Tong School. This option is good if you wish to secure a home today with the potential of renting it out in the future to cover costs while you rent a place within 1km to Ai Tong.

It does make sense if interest rates are lower. However, our calculations use a conservative interest rate which resulted in the biggest loss among all the options.

So with all that being said, we think that the best approach now would be to rent for the time being so that you can move into a bigger place now without committing to a high-interest rate loan.

This allows you to sit on the sidelines given we’re at a market high and signs are pointing towards more supply coming up to alleviate the demand from the past few years. 12 years is a long time, and there are many unknowns, so it could be better to rent for the short term now while observing how the markets move before you make yours.

If your priority leans more towards space over amenities, you might want to consider cost-effective options like HDBs. This strategy would also free up more funds for investment in a diversified portfolio of stocks and bonds. Later on, this investment could assist you in purchasing a private property when interest rates are more favourable.

The primary risk with this strategy is the potential rise in property prices. While the future remains uncertain, current high interest rates suggest that a price stabilization in the short term is more probable.

ALSO READ: We are in our 20s making $11.5k per month: Should we buy an EC or BTO flat?

This article was first published in Stackedhomes.