What to look for in an older condo before you buy

PHOTO: Stackedhomes

New launch condos have a lot of psychological appeal, until you hear the horror stories – like Laurel Tree and Sycamore Tree condos going unfinished , or the $32 million lawsuit over defects at The Seaview.

[embed]https://www.facebook.com/todayonline/posts/10153098565287572[/embed]

Or maybe you’d love to have a new launch condo, but for some reason you have to move in immediately; and a 30+ year old development is the only viable location.

While on the other hand, older condos usually have more spacious living areas and regular layouts. Plus you can customise the space to exactly how you’d like it (not that you can’t do it for a new launch, but some might feel that it is such a waste).

Whether it’s by choice or otherwise, picking an older condo development is a complex process. From lease decay to the state of facilities, there are thousands of variables that can lead to inconvenience, poor rent, or capital losses upon resale.

Here’s how to research an older development and avoid pitfalls:

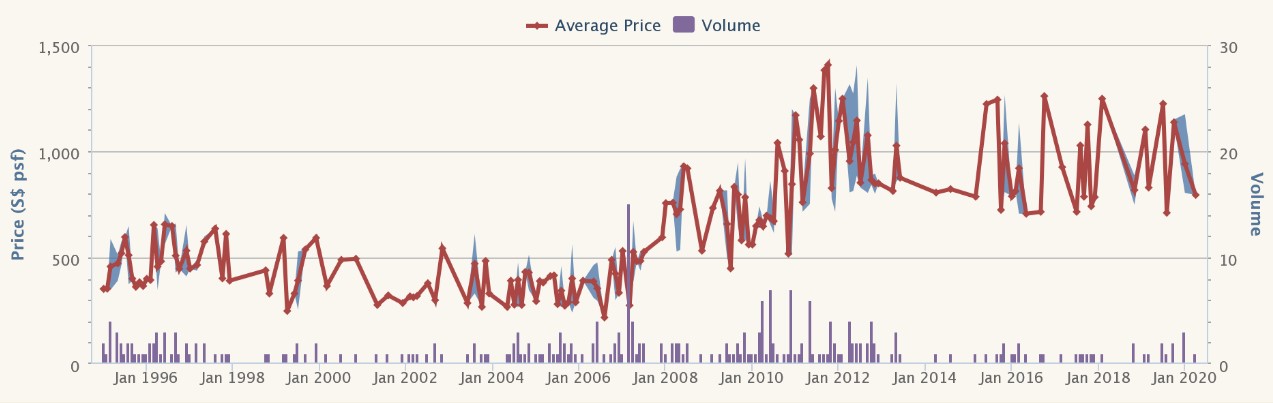

One big advantage of buying an older development is the long transaction history. Make full use of this to identify if you’re getting a fair price. But beyond that, you should also take note of price patterns.

Here’s an unusual pattern from People’s Park Complex:

Notice how volatile the prices are: transactions in June and Sept 2015 were around $1,242 psf, but similar sized units plunged to around $925 psf in March 2017. By October of the same year, prices were back up to $1,125 psf).

You could say that it is because of low transactions, but have a look at a similar old development in the area (Pearl Bank before it had gone en bloc) and you’ll find it isn’t anywhere near as volatile.

As to why, that’s a question to put to the seller’s agent; volatile prices can reflect situations like en-bloc struggles, new developments in the neighbourhood that affect the condo, or even problems with units in a specific stack (i.e. the sharp dives may reflect the sale of units in a “problem” block, where there are maintenance issues due to age).

Another thing to note is consecutive declines in price. For example, this is the price movement at Sembawang Cottage:

Note that these alone may not indicate a bad buy; they may be due to certain episodic issues that are soon corrected (e.g. a recently failed en-bloc attempt). But do present such questions to sellers, and look for a satisfactory answer.

If you have doubts about their explanation, drop us a message on Facebook ; we may have information that can help to verify it.

Some banks don’t like to give out full financing (75 per cent of the property price or value, whichever is lower), for properties dating back to 1980 or earlier. You may have to fork out a much bigger down payment (e.g. the financing may fall to 55 per cent).

While some banks may still offer full financing, those banks may not have the lowest home loan interest rates. As such, you could end up paying more than you initially expected.

As for future resale value, note that banks will not finance properties with 30 years or less on the lease. So while you may still be able to get financing, subsequent buyers of your property may not. This can decimate resale value, as your future buyers will have to pay in cash.

This isn’t so that you can plan for an en-bloc windfall, although it does help to estimate the chances (but never count on an en-bloc in your financial planning).

The main issue here is the Sellers Stamp Duty (SSD) . This is:

The SSD still applies in the event of an en-bloc sale.

Also remember the en-bloc sale proceeds may not take into account the full value of your renovations; and they certainly don’t account for the inconvenience of moving again so soon, the lost opportunity cost of not buying somewhere else, etc.

Coupled with having to pay the SSD, it can add up to a frustrating waste of time and money.

Now there is a waiting time of 24 months between each en-bloc attempt. So if the last en-bloc was three years ago and nearly succeeded*, there’s a risk that a successful en-bloc may happen too soon after you buy.

Unfortunately, there’s no requirement for en-bloc attempts to be lodged anywhere; so you have to take the seller’s word on this. You can also drop us a message , and we’ll try to ascertain the details if possible.

*80 per cent of the development’s ownership must agree to the en-bloc for it to proceed.

Some of the things to do here are:

It’s possible for a 99-year leasehold development to be sitting on freehold land. In this instance, the owner of the freehold land – be it an individual or entity – has simply leased out their land for 99-years. At the end of the lease, the land will revert back to them.

An example of this would be Spring Grove Condominium, which is a 99-year leasehold condo, sitting on freehold land owned by the United States government .

Take note that this sort of arrangement affects en-bloc potential. You can’t know for sure what the ultimate owner wants to do with the land. If they decide to use the land for their own developments, then any en-bloc deal may be impossible, as they won’t offer another 99-year lease.

Old developments do have a higher rental yield, for no reason other than the lower initial price tag. However, you should also take into account rentability. This is how easy or quickly you can find a tenant.

Remember that tenants can be put off by poorly maintained facilities, or dated and run-down appearances. If you wouldn’t rent such a unit, then neither will they – whatever the potential rental yield may be.

This article was first published in Stackedhomes.