You can now buy part of a $300m bungalow - but you can't live in it

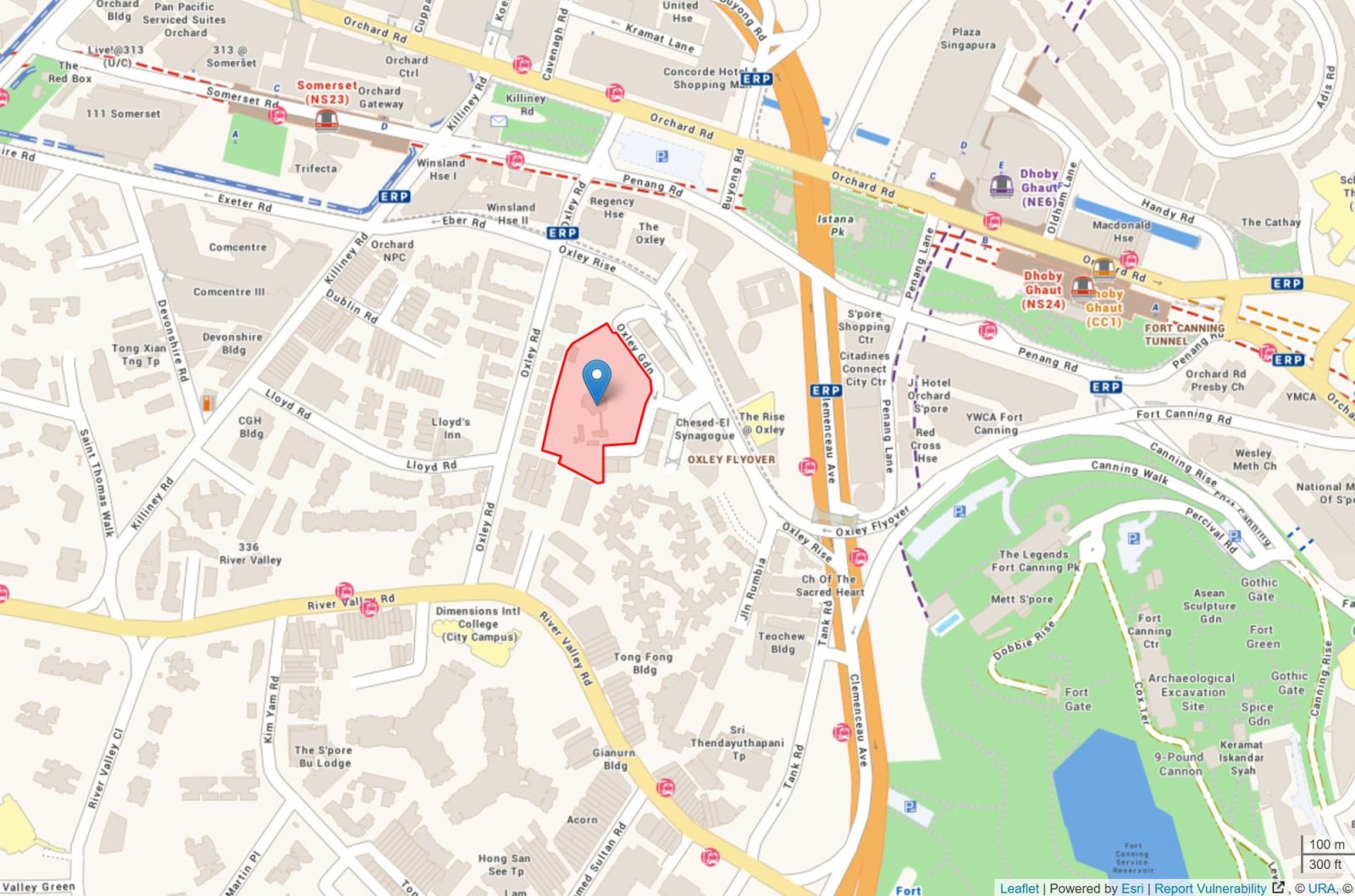

Including an access road bordering its eastern boundary, the site at 5 Oxley Rise has a total land area of 151,204 sq ft.

PHOTO: Urban Redevelopment Authority

You’ve probably heard of a 99-1 property ownership arrangement, but how about owning a one-seventh stake of a sprawling bungalow in prime District 9?

This unusual sale is the result of a court-ordered receiver’s sale. What makes this even more tantalising is the type of property this partial sale involves.

The property is 5 Oxley Rise, a sprawling 151,204 sq ft plot that features a grand two-storey bungalow with single-storey outhouses. The site also includes an access road bordering its eastern boundary.

This hilltop bungalow plot is just minutes away from the Orchard Road shopping belt and Dhoby Ghaut MRT station.

The property is on an exceptionally large freehold parcel within this prime district. Even by the standards of most Good Class Bungalows (GCBs), the size of the plot at 5 Oxley Rise is one of the largest unsubdivided plots.

But this is no Good Class Bungalow. In fact, about 117,229 sq ft of the plot (or about 78per cent of the entire site) is zoned for two-storey mixed landed housing, based on the latest Master Plan.

According to a press release on Feb 25, ERA Singapore has been appointed as the sole and exclusive marketing agent by the Joint and Several Receivers, Joshua James Taylor and Chew Ee Ling of Alvarez & Marsal (SE Asia), for the sale of the one-seventh interest in the property.

[[nid:506837]]

The bungalow was last put up for sale in 2022 at an asking price of $300 million, and if it had been sold back then, it would have been one of the most valuable residential plots ever publicly offered in Singapore.

The property was previously the residence of Cheong Eak Chong, one of Singapore’s pioneer real estate developers. He was the founder of Hong Fok Corporation and the Tian Teck Group. Hong Fok developed the iconic Concourse Skyline and The Concourse on Beach Road, as well as the International Building on Orchard Road.

After the patriarch’s passing in 1984, the property was reportedly inherited by his seven sons; each received a one-seventh interest. This inheritance structure is what created the fractional ownership arrangement.

However, the fact that a one-seventh stake in the property is under receivership hints at the financial background of one of the inheritors. In a receivership sale, a court-appointed receiver takes control of an asset to sell it to recover funds, often on behalf of a lender.

So, it seems that one of the owners of a one-seventh stake may have fallen into financial distress, which led to the court-ordered receivership sale. Details of the private co-ownership arrangement and the identity of the seller have not been disclosed.

Responding to queries sent by Stacked, ERA says: “The 1/7 interest is offered on a ‘View to Offer’ basis. 1/7 interest is currently under receivership, which we are mandated by the Receiver to sell this interest. The other 6/7 interest is not part of this tender exercise; hence, we are not able to comment.”

In straightforward terms, the buyer becomes a co-owner of the land, but not an occupier with clear rights to use, alter, or monetise the property independently. That is, the owner of the share cannot move in, redevelop the site, lease the site, etc. without the consent of the other owners.

What they can do is participate in decisions. This includes:

No price has been given for the one-seventh stake in the property. And we can’t assume that the value of the ownership stake would be $43 million, even though the property was last on the market for $300 million in 2022.

In general, minority interests like these almost always trade at a discount. This is due to the lack of control, as opposed to conventional ownership.

Most families that own such high-value landed assets typically resolve internal financial issues privately. If one member needs cash, for example, we usually see a quiet buyout by another family member (or other restructuring behind closed doors).

Allowing a one-seventh stake in a $300 million bungalow to be sold publicly is very unconventional. Speculatively, this might mean that a private solution couldn’t be reached, at least not in time. So now, a potentially external (non-family) co-owner may end up sitting alongside the family.

An external buyer’s intentions could range from eventually selling the stake back to the family, using it as leverage in negotiations, or perhaps even a starting point to buy over the entire property. At this stage, there’s no way to know what will materialise.

Meanwhile, the sale of the one-seventh stake in 5 Oxley Rise is on an “as-is-where-is” basis. The tender for the sale closes on Thursday, 9 April.

[[nid:575376]]

This article was first published in Stackedhomes.