Your savings account sucks, here are some that don't - 2020 edition

PHOTO: Unsplash

Believe it or not, masses of Singaporeans are still using a POSB savings account and “enjoying” the standard POSB interest rates of 0.05 per cent p.a. on their hard-earned savings.

You know what? That’s equivalent to paying hundreds of dollars every year (in inflation) just to use the services of the bank.

You really don’t need to suffer this injustice, though, because there are plenty of banks in Singapore vying for your business with more attractive interest rates on their savings accounts.

These days, you can quite realistically get 1.5 per cent to 2 per cent p.a. (or more!) in interest.

Here’s our pick of the best savings accounts in Singapore with the best interest rates for 2020.

| Savings account in Singapore | Realistic interest rates | How to maximise interest rate |

| UOB One account | 0.25 per cent to 2.5 per cent p.a. | Credit card spend + salary credit OR bill payment |

| OCBC 360 account | 0.6 per cent to 1.2 per cent p.a. | Credit card spend + salary credit + increase monthly balance + invest $20,000 |

| DBS Multiplier account | 0.7 per cent to 1.8 per cent p.a. | Salary credit + credit card spend + invest |

| POSB SAYE account | 2 per cent p.a. | Save fixed amount every month + don’t touch for 2 years |

| Standard Chartered BonusSaver account | 0.3 per cent to 1.3 per cent p.a. | Salary credit (>$3,000) + credit card spend + bill payment |

| Bank of China SmartSaver | 1.45 per cent to 3.4 per cent p.a. | Salary credit (>$6,000) + credit card spend + bill payment |

| Maybank Save Up programme | 0.43 per cent to 3 per cent p.a. | Pick 3 banking categories (loans, credit card spending, etc.) |

| Citi MaxiGain Savings Account | 0.177 per cent to 0.727 per cent p.a | Stash away at least $15,000 ($70,000 for higher interest) + don’t touch for 1 year |

| CIMB FastSaver account | 0.5 per cent p.a. to 0.8 per cent p.a. | Stash away spare cash (any amount) |

If you’re wondering why I put “realistic” interest rates, you clearly haven’t been burned by the professional liars known as banks.

Banks typically advertise crazy high interest rates to lure you into opening a bank account. They’re counting on you not doing the homework, because if you did, you’d realise that the high rates only apply to, say, account balances above $500,000. Who even has that much?!

So to keep things real, I’ve projected the following savings accounts interest rates conservatively – based on what’s actually within reach for typical working adults in Singapore.

UOB may be known for its complicated T&Cs, but surprisingly, the UOB One account is one of the simplest high interest savings accounts to use.

As of August 1, 2020, UOB will be revising their interest rates downwards to reflect the terrible economic times we’re going through.

The good news is that they’re not revising their requirements to earn bonus interest, so you don’t have to change your habits in order to grasp at whatever interest there is left to earn. In fact, they’ve expanded the range of credit cards you can use to meet the compulsory minimum spending requirement.

Pick this account if you want to earn an okay interest rate without thinking too hard, because the only requirement is spending at least $500 a month on a UOB credit card.

The following UOB credit cards can be used to satisfy the UOB One account’s spending requirements: UOB One Card, UOB Lady’s Card+, UOB YOLO, UOB One Debit Mastercard or Visa Card, and Mighty FX Debit Card.

To boost your interest, you can either credit your salary or pay 3 bills by GIRO. This is great for those without a regular paycheck such as freelancers, retirees or homemakers.

$500 credit card spend [compulsory]: 0.25 per cent p.a.

$500 credit card spend [compulsory] + $2,000 salary credit: 0.75 per cent p.a.

$500 credit card spend [compulsory] + pay 3 bills by GIRO: 0.75 per cent p.a.

Initial deposit: $1,000

Minimum balance (monthly): $1,000

Bonus interest cap: $75,000

The OCBC 360 account is more complicated than the UOB One, but also more flexible in that there is no one mandatory requirement.

OCBC 360’s interest rates have been revised downwards as of July 1, 2020. They have also done away with their bonus interest for spending on an OCBC credit card.

Because of its tiered interest system, this account is best for people with lots of cash on hand. That’s because you earn lower interest on the first $35,000, while balances from $35,001 to $70,000 get a higher interest rate.

To really maximise your returns, you should insure or invest with eligible products as well. The minimum insurance premium or investment amounts vary depending on the product.

The minimum amount ranges from $2,000 a year in insurance premiums to $20,000 worth of investment in structured deposits, unit trusts and single premium insurance. If you wish to invest in bonds and structured products to meet this requirement, you need to put in at least $200,000.

If you don’t have that much cash on hand and/or aren’t willing to commit that much, it’s easier to earn bonus interest with the UOB One account or DBS Multiplier.

By the way, the account also offers extra interest on your first $70,000 if you maintain a balance of at least $200,000, but that’s overkill as you could get higher interest by parking that extra money elsewhere.

$1,800 salary credit: 0.6 per cent p.a.

$1,800 salary credit + increase monthly balance by $500: 0.8 per cent p.a.

$1,800 salary credit + increase monthly balance by $500 + investment: 1.4 per cent p.a.

Initial deposit: $1,000

Minimum balance (monthly): $3,000 (fall-below fee waived for 1st year)

Bonus interest cap: $70,000

The DBS Multiplier account gives you bonus interest for banking with DBS in multiple categories. Income crediting is compulsory, but apart from that you can choose from credit card, investment, insurance and home loan.

The interesting thing is that from Feb 1, 2020 onwards, dividends will be considered “income” instead of “investments”, so those who don’t have a regular pay-check have another way to fulfil the compulsory criteria.

On the downside, from Aug 1, 2020 onwards, the interest rates will be revised downwards. There have been no major changes to how you earn this interest, though, so if you already have this account you can just keep on doing what you’re already doing.

I like that there’s no minimum amount for anything, though you must make sure your total transactions (including salary) add up to at least $2,000 a month.

So even if you’re earning less than $2,000 a month, you can still get a decent interest rate.

DBS looks at the total amount in transactions to award interest, so the more you transact, the more interest you can get.

Income credit [compulsory] + credit card spend: 0.7 per cent to 1.1 per cent p.a.

Income credit [compulsory] + credit card spend + investment/home loan: 1.3 per cent to 1.8 per cent p.a.

You can technically earn more interest if you transact more than $15,000 a month, but, uh, you probably wouldn’t be reading this if you were that well-off.

Initial deposit: None

Minimum balance (daily): $3,000 (fall-below fee waived for account holders up to age 29)

Bonus interest cap: $25,000 (or up to $100,000 if you transact in more categories)

A good supplement to the DBS Multiplier account is the POSB SAYE (Save As You Earn) account, which less of a traditional savings account and more of a tool to instil some discipline in your savings.

You need to set up a standing order to credit a fixed amount every month (anything from $50 to $3,000) from your DBS Multiplier into the SAYE account. Then resist the urge to touch it for 2 years.

POSB SAYE interest rate: 2 per cent p.a. (if conditions are met)

Initial deposit: –

Minimum balance (daily): –

Bonus interest cap: –

Similar to the DBS Multiplier and UOB One accounts, the Standard Chartered BonusSaver account also gives you extra interest for crediting your salary and using their credit cards.

This account starts with 0.05 per cent p.a. credit your salary (minimum $3,000) and you get an extra 0.4 per cent p.a. Then spend $500 on StanChart cards to get an extra 0.3 per cent p.a. (or 0.8 per cent, if you spend $2,000 and up that month).

The above-mentioned rates are based on Standard Chartered’s latest update to its terms and conditions, effective July 1, 2020 onwards.

Since April 1, 2020, bonus interest for bill payments has been lowered to 0.1 per cent p.a. (previously 0.25 per cent p.a.).

Bonus interest for investments and insurance has been revised to 0.85 per cent, and investments and insurance now count as two separate categories, so you have the chance to earn 0.85 per cent x 2 if you satisfy the requirements for both (before July 1, 2020, investments/insurance counted as one category offering 1.28 per cent p.a).

$3,000 salary credit: 0.4 per cent p.a.

$3,000 salary credit + $500 credit card spending: 0.7 per cent p.a.

$3,000 salary credit + $500 credit card spending + pay 3 bills by GIRO (min. $50): 0.8 per cent p.a.

Initial deposit: $3,000

Minimum balance (daily): $3,000

Bonus interest cap: $100,000

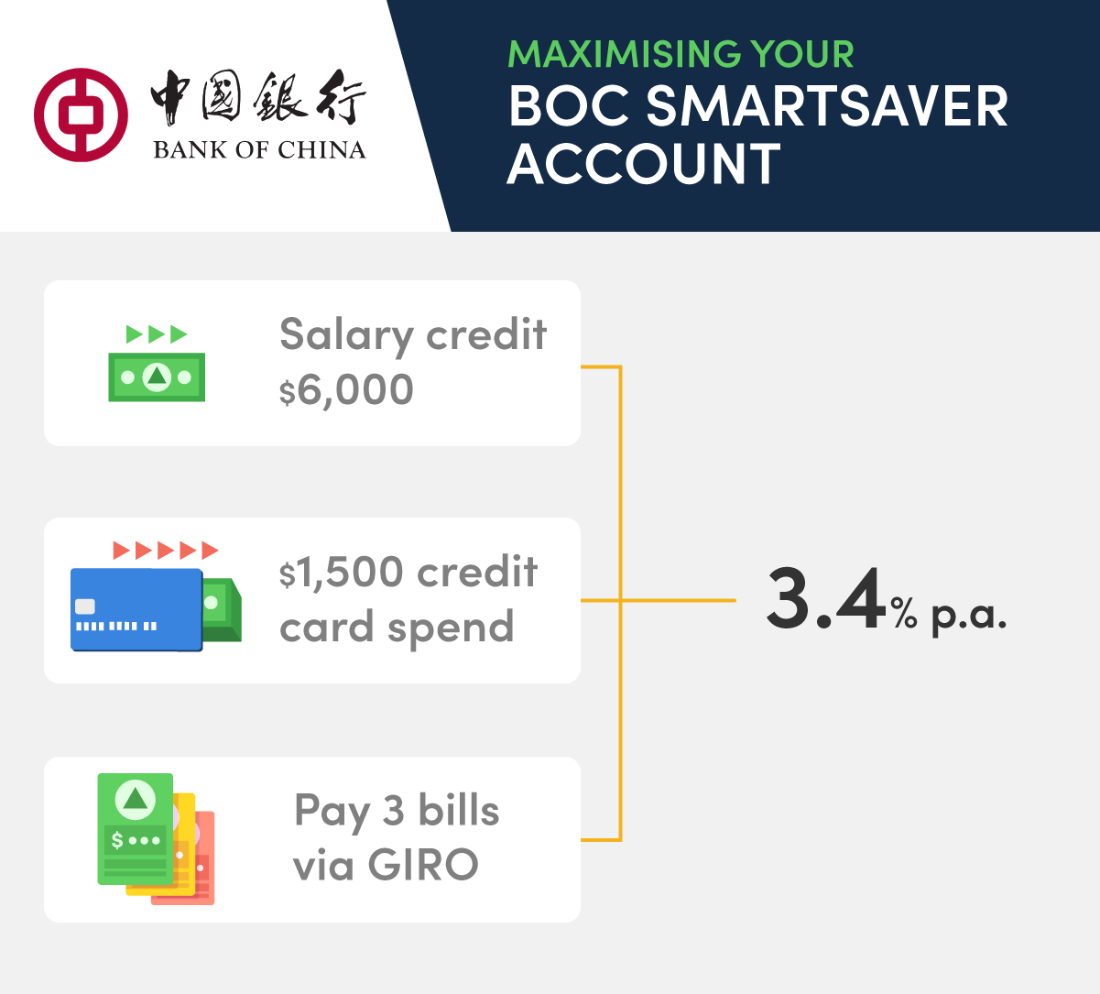

If you’re OK with the inconvenience of banking with Bank of China, their SmartSaver account is actually a very good choice for high earners.

They offer probably the highest interest rates in Singapore for those who take home a monthly salary of at least $6,000. And the best thing is you don’t have to jump through too many hoops either.

Assuming the base interest rate is 0.25 per cent p.a., what you can get realistically is as follows.

$6,000 salary credit: 1.45 per cent p.a.

$6,000 salary credit + $500 credit card spend: 2.25 per cent p.a.

$6,000 salary credit + $1,500 credit card spend: 3.05 per cent p.a.

$6,000 salary credit + $1,500 credit card spend + pay 3 bills by GIRO (min. $30): 3.4 per cent p.a.

Initial deposit: $1,500

Minimum balance (monthly): $1,500

Bonus interest cap: $60,000

Already crediting your salary and consolidating all your credit card spending on a multiplier bank account? It’s possible to “cheat” on your primary account with Maybank if you’re on the market for bank loans.

The Maybank Save Up Programme lets you choose from 10 (!) different actions to get bonus interest.

These include bill payment or crediting salary, credit card spending, home loans, car loans, insurance and investments.

While it sounds like there’s a lot you can do to earn bonus interest, in reality only four actions let you earn bonus interest for the whole year, namely — home loans, car loans, insurance and investing at least $50,000 in unit trusts.

Investing $50,000 in structure deposits earns you 3 months’ worth of interest, and all the other actions will get you a measly one month.

I personally don’t think this is worth the trouble unless you really satisfy 2 categories that give you 12 months’ worth of interest — for example, if you’re already servicing a home loan and car loan from Maybank.

Any fewer than 2, and your interest drops to around 0.5 per cent p.a., which you can get for just crediting your salary with other banks.

Maybank has also reduced the high interest cap to just $50,000 of your deposits, which is low compared to the other accounts on this list.

(FYI, if you have at least $50,000 in savings, you can become a Maybank Privilege customer and get preferential rates on the Save Up Programme.)

Pick 3 categories to get about 2.75 per cent p.a + base interest of 0.1875 per cent to 0.279375 per cent

Initial deposit: $500

Minimum balance (monthly): $1,000

Bonus interest cap: $50,000

The Citi MaxiGain Savings Account is a powerful “stash and forget” kind of savings account – as long as you have at least $70,000 to stash away.

Another attractive benefit is that having $70,000 in your Citi MaxiGain account entitles you to Citi Priority benefits, which includes perks such as preferential rates, birthday deals and one-for-one deals. This means that it has one of the lowest barriers to priority banking.

The MaxiGain’s base interest rate is pegged at 50 per cent of the 1-month SIBOR, an interbank interest rate that fluctuates daily.

That sounds rather scary, especially since SIBOR has crashed recently. The current published 1-month SIBOR is a miserable 0.254 per cent, so that means if you open the account now, you can expect only about 0.127 per cent p.a. base interest.

How MaxiGain works is you just leave the money in there and let time do its work. Bonus interest automatically climbs each month, starting from 0.05 per cent p.a. and growing by 0.05 per cent every month until it reaches the maximum of 0.6 per cent p.a. This is provided that your balance in the month does not fall below the previous month’s.

Assuming that SIBOR is currently 0.254 per cent, you’ll be getting up to (50 per cent of 0.254 per cent) + 0.6 per cent = 0.727 per cent p.a. by the last month of a year.

If you do not deposit $70,000, but only put in the minimum deposit of $10,000, you will still be able to earn 0.6 per cent p.a. bonus interest (0.05 per cent every month stacked up).

To be fair, in “normal” times when SIBOR is healthy, this is quite a sweet deal. But given the dismal SIBOR rates right now, this is the worst time to sign up for this account.

Citi MaxiGain interest rate: 0.177 per cent p.a. to 0.727 per cent p.a

Initial deposit: None

Minimum balance: $10,000

Bonus interest cap: $150,000

Let’s say you have some “overflow” from your primary savings account and you want to keep it somewhere without having to jump through hoops. What do you do with it?

CIMB FastSaver used to be one of the most attractive and straightforward high interest accounts ever, paying out 1 per cent interest on everything up to $50,000. Alas, all good things come to an end, and from July 15, 2020, onwards that sweet, sweet 1 per cent will be halved.

From July 15, 2020, you will earn 0.5 per cent interest on everything up to $50,000. The good news is that they still don’t charge any fall-below fees, so using the account is still as fuss-free as ever.

CIMB FastSaver interest rate: 0.5 per cent p.a. on first $50,000 / 0.8 per cent p.a. on $50,001 / 1.5 per cent p.a. on $75,001 / $100,000

Initial deposit: $1,000

Minimum monthly balance: $1,000 (in order to earn interest)

Bonus interest cap: $100,000

This article was first published in MoneySmart. All content is displayed for general information purposes only and does not constitute professional financial advice.