Is BHG retail REIT attractive at a share price of $0.61?

PHOTO: The Straits Times

BHG Retail REIT is a retail REIT with shopping malls in China.

BHG Retail REIT’s share price stands at $0.61 on May 29.

At that price, the retail REIT is valued at a price-to-book (PB) ratio of 0.7 and a distribution yield of around 6 per cent.

Does the retail REIT provide a buying opportunity for long-term investors?

Let’s find out using my 10-step guide to pick the best Singapore REITs.

As a summary, here are the 10 steps I use to pick the best Singapore REITs:

BHG Retail REIT is a pure-play China retail REIT listed in Singapore on December 11, 2015.

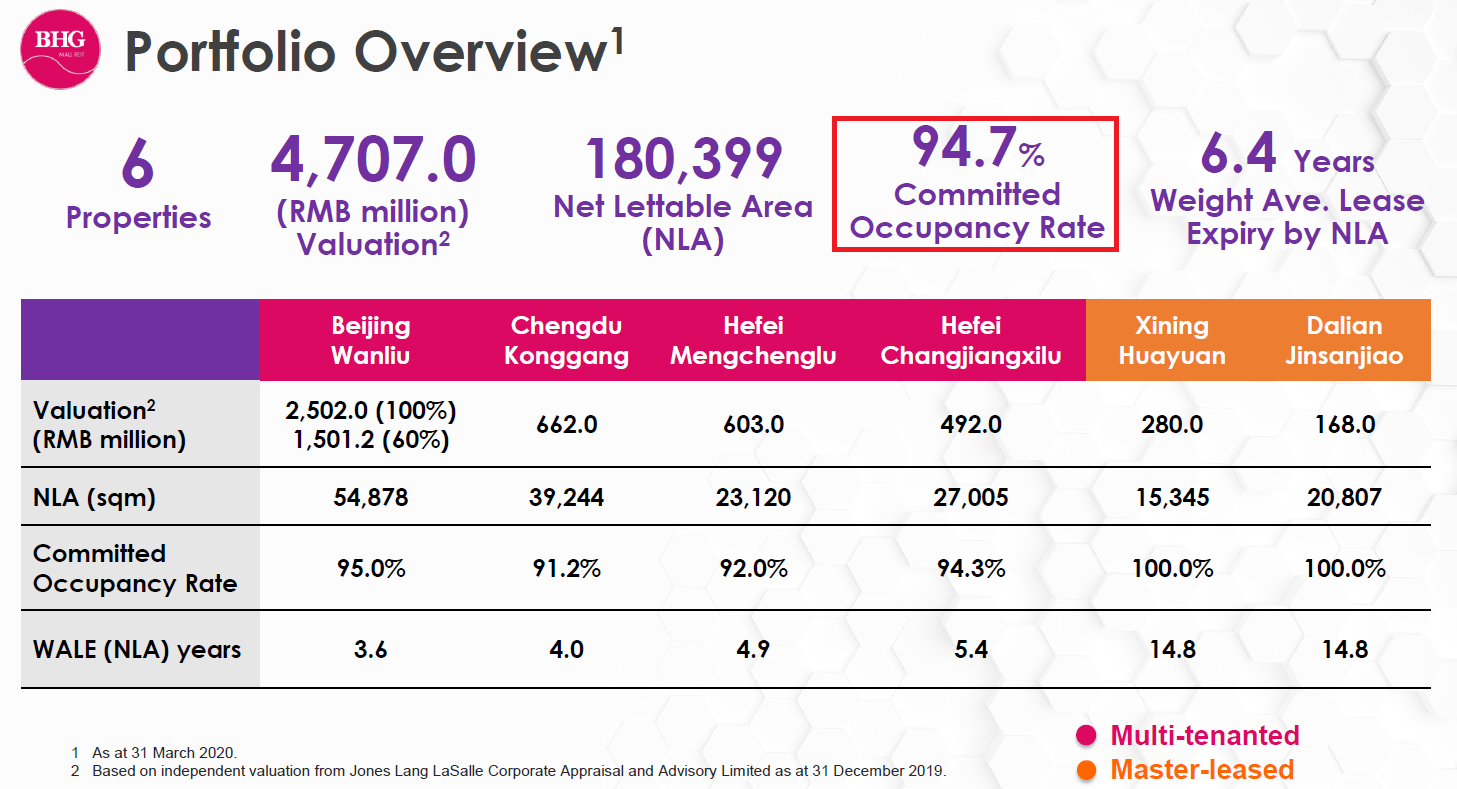

Its portfolio, as of December 31, 2019, was made up of six brick-and-mortar retail properties — Beijing Wanliu (60 per cent stake), Chengdu Konggang, Hefei Mengchenglu, Hefei Changjiangxilu, Xining Huayuan, Dalian Jinsanjiao.

Those properties are located in Tier 1, Tier 2, and other cities of significant economic potential in China.

BHG Retail REIT’s sponsor is an integrated retail group, Beijing Hualian Department Store Co Ltd.

BHG Retail REIT has a financial year that ends on 31 December each year.

Let’s now check on how the REIT has performed in terms of its gross revenue and NPI from 2016 to 2019.

| 2016 | 2017 | 2018 | 2019 | Compound annual growth rate (CAGR) | |

|---|---|---|---|---|---|

| Gross revenue ($' million) |

62.6 | 64.5 | 69.7 | 79.1 | 8.1 per cent |

| Net property income ($' million) |

40.3 | 42.9 | 45.6 | 50.5 | 7.8 per cent |

We can see that BHG Retail REIT’s gross revenue and NPI have stepped up nicely over the last four years.

Verdict: Pass

Next, let’s find out if DPU has been growing consistently over the years as well.

| 2016 | 2017 | 2018 | 2019 | CAGR | |

|---|---|---|---|---|---|

| Distribution per unit (Singapore cents) |

5.32 | 5.47 | 5.16 | 3.87 | -10.1 per cent |

Unfortunately, DPU has fallen from 2016 to 2019.

The decline from 2017 onwards was largely due to an increased number of units that were entitled to distribution as a result of the reduction of distribution waiver (more on that below), as well as the payment of management fees in units instead of cash.

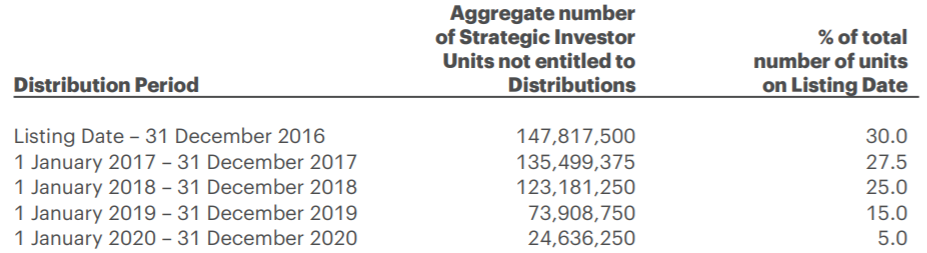

BHG Retail REIT’s strategic investor, Beijing Hua Lian Group (Singapore) International Trading Pte Ltd, has agreed not to receive distributions under the distributions undertaking seen below:

This is to demonstrate its support for BHG Retail REIT and its commitment to the long-term growth and development of the REIT.

The distributions undertaking expires on January 1, 2021.

In its IPO prospectus, BHG Retail REIT warned that there is a possibility for DPU to fall once the distribution waiver is over:

“Following the expiry of the Distributions Undertaking on 1 January 2021, the properties may not be able to generate a level of income for distribution to the unit holders that is commensurate with the levels attained with the support of the Strategic Investor under the Distributions Undertaking due to unforeseen circumstances like material changes in the economic and real estate policies of the areas in which the properties are located and an unexpected supply of competing shopping malls.

"If, after the expiry of the Distributions Undertaking, the properties are not able to generate a level of income that is commensurate with the levels attained with the support of the Strategic Investor under the Distributions Undertaking, there may be a drop in the distributable Income and unit holders may consequently face a drop in their DPU and distribution yield.”

This is something that potential investors should take note of.

Verdict: Fail

Check for: Property yield of between 5 per cent and 9 per cent

For 2019, BHG Retail REIT’s NPI stood at $50.5 million, and it had a portfolio value of $909.0 million.

The figures translate to a property yield of 5.6 per cent, and hence, BHG Retail REIT passes this criterion.

Verdict: Pass

Check for: Gearing ratio below 40 per cent

As of March 31, 2020, BHG Retail REIT’s gearing ratio was a healthy 35.3 per cent, which is also below my threshold of 40 per cent.

Verdict: Pass

Check for: Interest coverage ratio above 5 times

BHG Retail REIT, at the end of March this year, had an interest cover of just 2.8 times, which is not to my liking.

Verdict: Fail

Check for: Healthy portfolio occupancy rate

BHG Retail REIT’s portfolio was around 95 per cent occupied, as of March 31, 2020.

Even though the occupancy rate is lower than the end of 2019’s figure of almost 97 per cent, occupancy is still at a healthy range.

Verdict: Pass

Check for: Positive rental reversions

For 2019, BHG Retail REIT’s manager said, without revealing any figures, that all properties had healthy rental reversion for new and renewed leases.

Verdict: Pass

In terms of growth, most of BHG Retail REIT’s leases above a year come with a built-in rental escalation arrangement, giving the REIT organic growth.

On top of growth through organic means, BHG Retail REIT is also able to grow inorganically through acquisitions of 12 properties under its sponsor’s voluntary right of first refusal (ROFR) agreement.

A ROFR arrangement ensures that a REIT’s sponsor offers its properties to the REIT for purchase consideration first before any other company.

The ROFR agreement for BHG Retail REIT is “voluntary” as its sponsor is not required to provide a ROFR to the REIT since it’s not a controlling unitholder of BHG Retail REIT.

Even then, the sponsor has expressed its strong support for the long-term well-being of BHG Retail REIT, according to the IPO prospectus.

Before BHG Retail REIT’s manager acquires properties, it will consider if the property:

1) Will be DPU-yield accretive;

2) Has a sustainable operating performance; and

3) Possesses the potential for future organic growth.

Such stringent criteria shows prudence on the manager’s part.

BHG Retail REIT is also optimistic that its “long-term strategy is well-positioned to benefit from China’s rising residents’ income and consumption upgrade”.

Verdict: Pass

Check for: Acceptable price-to-book ratio

At BHG Retail REIT’s unit price of $0.61, it has a PB ratio of 0.73x.

Since the latest PB ratio is below 1x, it could mean that BHG Retail REIT is undervalued.

We are unable to compare BHG Retail REIT’s current PB ratio with its historical five-year average since the REIT was listed only in December 2015.

Verdict: Pass

Check for: Distribution yield to be above 5 per cent

At BHG Retail REIT’s unit price of $0.61, it has a trailing distribution yield of 6.3 per cent, which is above 5 per cent.

Verdict: Pass

BHG Retail REIT has a final score of 8/10.

Although BHG Retail REIT scores highly as a REIT, I’m concerned about its falling DPU.

This is especially so when the distribution undertaking expires on January 1, 2021, as discussed earlier.

Therefore, I’d rather place BHG Retail REIT on my watchlist and monitor it for the next couple of years as I believe it has growth potential.

This article was first published in Seedly.