Buyer's and seller's stamp duty: What you should know

PHOTO: Pexels

Update as of Jan 12, 2022: This article has been updated to include the latest ABSD rates, in light of the recent cooling measures announcement.

Stamp duty – it’s one of the many additional but often-overlooked costs associated with buying property.

Stamp duty refers to the tax relating to the purchase or lease of a property. In Singapore, it is payable to the Inland Revenue Authority of Singapore (IRAS).

Since 2011, stamp duty has been used as one of many property cooling measures to ensure Singapore’s continued stable and sustainable property market.

Here’s what you need to know about Singapore’s stamp duty:

There are three types of duties payable on the sale, purchase, acquisition or disposal of properties in Singapore:

The Buyer’s stamp duty (BSD) is payable on the purchase or acquisition of all properties and is calculated on the property’s purchase price or market value (whichever is higher). Since 2018, the top marginal BSD rate for residential properties has been 4 per cent.

| Purchase price or Market value of property | BSD rates for residential properties | BSD rates for non-residential properties |

| First $180,000 | 1 per cent | 1 per cent |

| Next $180,000 | 2 per cent | 2 per cent |

| Next $640,000 | 3 per cent | 3 per cent |

| Remaining amount | 4 per cent | 3 per cent |

Here’s an IRAS example of the BSD payment due for a condominium unit purchased in 2018 at $2,500,550 (reflective of the market value):

| Market value of the property | BSD rate | Calculation |

| First $180,000 | 1 per cent | = $1,800 (1 per cent x $180,000) |

| Next $180,000 | 2 per cent | = $3,600 (2 per cent x $180,000) |

| Next $640,000 | 3 per cent | = $19,200 (3 per cent x $640,000) |

| Remaining $1,500,550 | 4 per cent | = $60,022 (4 per cent x $1,500,550) |

| BSD payable | = $84,622 ($1,800 + $3,600 + $19,200 + $60,022) |

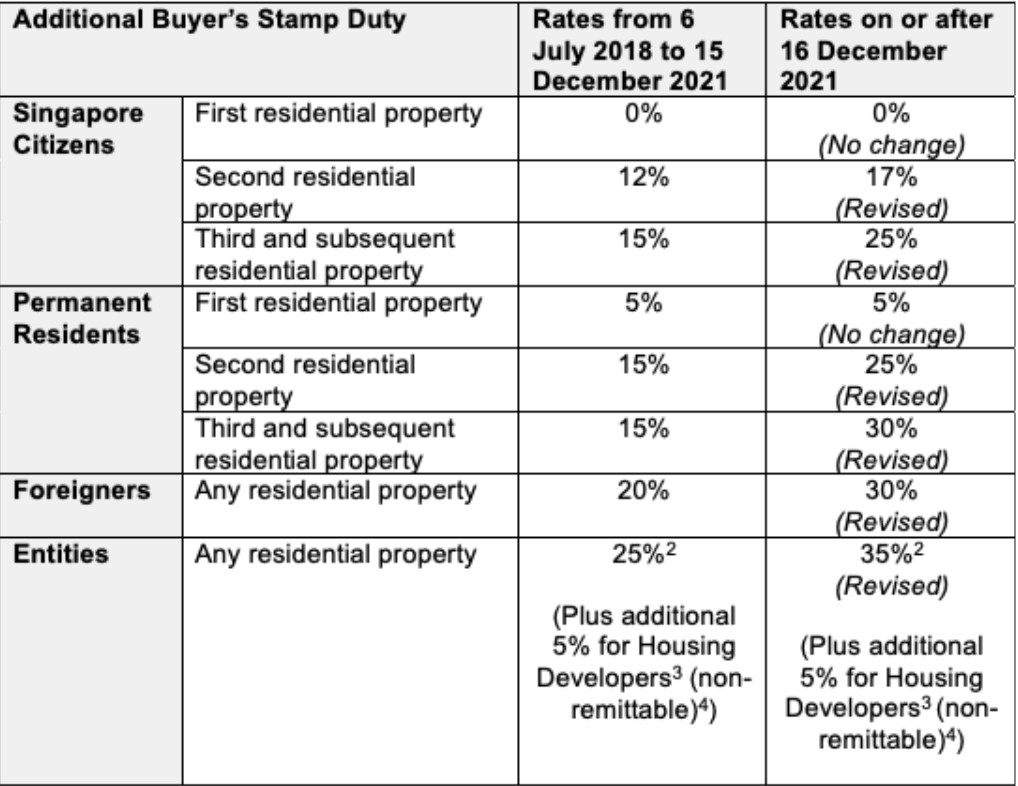

The Additional Buyer’s Stamp Duty (ABSD) is payable for the second or subsequent properties. It is payable in addition to the BSD, where the amount payable varies according to the buyer’s residential profile.

The ABSD rates were last revised on Dec 16, 2021 as a cooling measure to stabilise the residential property market in Singapore and avoid the risk of a more drastic price correction – meant to discourage foreigners and entities from purchasing residential properties.

ABSD applies to different residential profiles as follows:

Nationals and PRs of Iceland, Liechtenstein, Norway or Switzerland, as well as US Nationals are accorded the same Stamp Duty treatment as Singapore Citizens. As such, these individuals may apply for remission of ABSD when buying their first residential property in Singapore.

Remission of ABSD may be applicable for married couples who purchase a second residential property jointly. To learn more, click here.

Seller’s Stamp Duty (SSD) is payable on properties sold within the three-year holding period after buying a property (on or after Feb 20, 2010).

The SSD is taxed on early sellers to avoid a property market with inflated prices as a result of property flipping. It’s a way to curtail the abuse of abundantly available deferred payment schemes (eg. down payment of 20 per cent of the purchase price, pay remaining 80 per cent two years later).

The tax duty is a percentage of the valuation or price of the property being sold (whichever is higher). The earlier you sell, the higher the SSD.

Other property price cooling measures include the Total Debt Servicing Ratio (TDSR) — which allows homebuyers to borrow only up to 55 per cent of their gross monthly income. It has been in the works since 2013 to prevent home buyers from borrowing too much to finance the purchase of a property, as it affects the amount that can be borrowed for subsequent properties.

Property owners or home purchasers can borrow up to 75 per cent of the property value through a bank loan. For the second property, this loan-to-value (LTV) ratio drops to 45 per cent for loan tenures up to 30 years, or 25 per cent if the loan tenure goes beyond 25 years or the owner’s 65th birthday, meaning that buying a second property needs a lot more cash than the first property.

Cash down payments can also be made using CPF savings, but depends on:

Finally, stamp duty is also payable on rental tenancy agreements, to be paid when an individual rents a property or signs a contract to renew or extend their current lease.

The amount payable is dependent on the Average Annual Rent (AAR), which is computed based on the monthly rent and lease period.

So assuming the monthly rent is $3,000 and the lease period is 24 months, the AAR and lease duty rates would be:

AAR: $3,000 x 24 months = $72,000

Lease duty rates: 0.4 per cent x $72,000 = $288