Most affordable resale HDB flats you can buy if you are aged 30 and under

PHOTO: Stackedhomes

If you want a BTO flat these days, it can feel like there are flaming hoops to jump through. Coupled with oversubscribed flats and recent Covid-19 construction delays, you may be better off looking for a resale flat instead.

“But wait,” you might say, “Resale flat prices are more expensive, and are at an eight-year high!”

Okay, that’s true.

And let’s not forget, while it seems like a no-brainer to look at the absolute cheapest resale HDB there is, you do have limits on how old a flat you can actually buy based on your age.

As of May 10 2019, the remaining lease of the flat has to be at least 20 years (naturally) and can cover the youngest buyer up till the age of 95 – as long as you want to fully utilise your CPF.

For buyers who do not meet this criteria, the amount of CPF that can be used is pro-rated based on the extent the remaining lease of the flat can cover the youngest buyer up to the age of 95 (more info here).

So in a bid to help younger home buyers looking for house options at this point, we’ve combed through listings and HDB towns, to pick out the most affordable resale flats as of end-April 2021.

To be safe, we looked for HDB flats that had at least 66 years lease remaining and onwards.

Here’s where to look, and how much you’ll need:

| Address | Three-room | Lease remaining (years) | Estate |

| 19 Marsiling Lane | $223,000 | 66 | Woodlands |

| 284 Yishun Ave 6 | $238,000 | 66 | Yishun |

| 641 Yishun St 61 | $242,000 | 70 | Yishun |

| 409 Bt Batok West Ave 4 | $243,000 | 66 | Bukit Batok |

| 415 Bt Batok West Ave 4 | $245,000 | 67 | Bukit Batok |

| 523 Bt Batok St 52 | $245,000 | 66 | Bukit Batok |

| 722 Yishun St 71 | $249,000 | 66 | Yishun |

| 286 Yishun Ave 6 | $250,000 | 66 | Yishun |

| 333 Bt Batok St 32 | $250,000 | 66 | Bukit Batok |

| 505 Bt Batok St 52 | $250,000 | 66 | Bukit Batok |

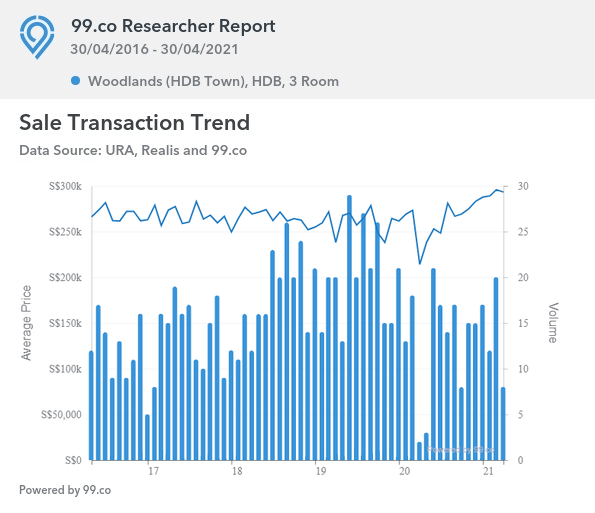

As of end-April 2021, average prices of three-room flats in Woodlands are at $293,250.

As of end-April 2021, average prices of three-room flats in Yishun are at $328,786.

As of end-April 2021, average prices of three-room flats in Bukit Batok are at $304,846.

Important: Note that the remaining lease of the flat must last until the youngest buyer reaches 95 years of age. If this age requirement is not met, you may not receive full financing from the HDB loan.

We will use the median price of $245,000 as an estimate:

Assuming full financing, this is 10 per cent of the price or value, whichever is lower. This must be paid in any combination of cash or CPF. We will assume, for this example, that the price and valuation are almost similar.

This comes to a down payment of about $24,500.

ALSO READ: We bought a house on Carousell - here's what we learnt

This is $3,100, payable in any combination of cash or CPF (see the IRAS website for details on how BSD is calculated)

We will assume the maximum loan quantum of $220,500, for 25 years. The HDB loan has an interest rate of 2.6 per cent per annum. This comes to about $1,000.34 per month.

The total repayment over 25 years will come to about $300,102.38, with total interest repayments of close to $79,602.38.

To meet the Mortgage Servicing Ratio (MSR), the loan repayment must not exceed 30 per cent of your monthly income. Based on the above loan repayment, your minimum income should be around $3,000.

Important: For older properties there may be greater difficulty getting a bank loan. Banks may not provide maximum financing (i.e., you need a bigger down payment).

Assuming full financing, this is 25 per cent of the price or value, whichever is lower. The first five per cent of any property purchase must always be paid in cash, while the next 20 per cent can be paid with cash or CPF.

We will assume, for this example, that the price and valuation are almost similar.

This comes to a minimum cash down payment of $12,250. The next part of the down payment comes to $49,000, payable in any combination of cash or CPF.

As above: $3,100, payable in any combination of cash or CPF

Unlike HDB loans, bank loan rates will fluctuate. The rate is also determined by the loan package you choose.

Nonetheless, we will use the current average interest rate of 1.3 per cent, over a loan tenure of 25 years. Assuming full financing, the maximum loan amount is $188,750.

This comes to a monthly loan repayment of about $737.27. Over 25 years you would repay $221,181.68, with total interest repayments of $32,431.68.

Note that, for the purposes of calculating your servicing ratio, the bank will use an assumed interest rate of 3.5 per cent; even if the actual rate is much lower. So to meet the MSR using the loan above, you would need a monthly income of around $3,150.

| Address | Four-room | Lease remaining (Years) | Estate |

| 360 Tampines St 34 | $250,000 | 74 | Tampines |

| 314 Sembawang Dr | $280,000 | 77 | Sembawang |

| 236 Bt Panjang Ring Rd | $285,000 | 66 | Bukit Panjang |

| 437 Yishun Ave 6 | $287,667 | 67 | Yishun |

| 639 Yishun St 61 | $288,000 | 66 | Yishun |

| 658 Yishun Ave 4 | $288,055 | 66 | Yishun |

| 423 Bt Batok West Ave 2 | $290,000 | 66 | Bukit Batok |

| 119 Pending Rd | $290,000 | 67 | Bukit Panjang |

| 166 Yishun Ring Rd | $290,000 | 66 | Yishun |

| 401 Choa Chu Kang Ave 3 | $290,000 | 71 | Choa Chu Kang |

As of end-April 2021, average prices of four-room flats in Tampines are at $491,287.

As of end-April 2021, average prices of four-room flats in Sembawang are at $413,716.

As of end-April 2021, average prices of 4-room flats in Bukit Panjang are at $440,954.

As of end-April 2021, average prices of 4-room flats in Yishun are at $408,223.

As of end-April 2021, average prices of 4-room flats in Choa Chu Kang are at $430,099.

ALSO READ: Top 5 hottest HDB towns by resale volume (Q1 2021)

We will use the median of around $288,000 as an estimate:

Assuming full financing, this is 10 per cent of the price or value, whichever is lower. This must be paid in any combination of cash or CPF. We will assume, for this example, that the price and valuation are almost similar.

This comes to a down payment of about $28,800.

This is $3,960, payable in any combination of cash or CPF (see the IRAS website for details on how BSD is calculated)

We will assume the maximum loan quantum of $259,200, for 25 years. The HDB loan has an interest rate of 2.6 per cent per annum. This comes to about $1,175.91 per month.

The total repayment over 25 years will come to about $352,773.41, with total interest repayments of close to $93,573.41.

To meet the Mortgage Servicing Ratio (MSR), the loan repayment must not exceed 30 per cent of your monthly income. Based on the above loan repayment, your minimum income should be at least $3,920.

Assuming full financing, this is 25 per cent of the price or value, whichever is lower. The first five per cent of any property purchase must always be paid in cash, while the next 20 per cent can be paid with cash or CPF.

We will assume, for this example, that the price and valuation are almost similar.

This comes to a minimum cash down payment of $14,400. The next part of the down payment comes to $57,600, payable in any combination of cash or CPF.

As above: $3,960, payable in any combination of cash or CPF.

As before, we will use the current average interest rate of 1.3 per cent, over a loan tenure of 25 years. Assuming full financing, the maximum loan amount is $216,000.

This comes to a monthly loan repayment of about $843.71. Over 25 years you would repay $253,113.87 with total interest repayments of $37,113.87.

Note that, for the purposes of calculating your servicing ratio, the bank will use an assumed interest rate of 3.5 per cent; even if the actual rate is much lower. So to meet the MSR using the loan above, you would need a monthly income of around $3,605.

| Address | Five-room | Lease remaining (years) | Estate |

| 683B Choa Chu Kang Cres | $340,000 | 80 | Choa Chu Kang |

| 812 Jurong West St 81 | $340,000 | 68 | Jurong West |

| 851 Jurong West St 81 | $340,000 | 74 | Jurong West |

| 690F Woodlands Dr 75 | $344,000 | 81 | Woodlands |

| 948 Jurong West St 91 | $345,000 | 67 | Jurong West |

| 840 Jurong West St 81 | $348,000 | 71 | Jurong West |

| 481 Sembawang Dr | $350,000 | 78 | Sembawang |

| 813 Jurong West St 81 | $350,000 | 68 | Jurong West |

| 396 Yishun Ave 6 | $351,000 | 67 | Yishun |

| 814 Jurong West St 81 | $356,000 | 68 | Jurong West |

As of end-April 2021, average prices of five-room flats in Choa Chu Kang are at $526,225.

As of end-April 2021, average prices of five-room flats in Jurong West are at $503,262.

As of end-April 2021, average prices of five-room flats in Woodlands are at $486,490.

As of end-April 2021, average prices of five-room flats in Sembawang are at $455,472.

As of end-April 2021, average prices of five-room flats in Yishun are at $545,032.

ALSO READ: Is it worth buying a resale HDB flat for rental income? Top 10 HDB towns by rental yield

We will use the median of around $345,000 as an estimate:

Assuming full financing, this is 10 per cent of the price or value, whichever is lower. This must be paid in any combination of cash or CPF. We will assume, for this example, that the price and valuation are almost similar.

This comes to a down payment of about $34,500.

This is $5,100, payable in any combination of cash or CPF (see the IRAS website for details on how BSD is calculated)

We will assume the maximum loan quantum of $310,500, for 25 years. The HDB loan has an interest rate of 2.6 per cent per annum. This comes to about $1,408.64 per month.

The total repayment over 25 years will come to about $422,593.15, with total interest repayments of close to $112,093.15.

To meet the Mortgage Servicing Ratio (MSR), the loan repayment must not exceed 30 per cent of your monthly income. Based on the above loan repayment, your minimum income should be at least $4,695.

ALSO READ: Buying a resale HDB flat for future upgrading? Here's what you should consider

Assuming full financing, this is 25 per cent of the price or value, whichever is lower. The first five per cent of any property purchase must always be paid in cash, while the next 20 per cent can be paid with cash or CPF.

We will assume, for this example, that the price and valuation are almost similar.

This comes to a minimum cash down payment of $17,250. The next part of the down payment comes to $69,000, payable in any combination of cash or CPF.

As above: $5,100, payable in any combination of cash or CPF

As before, we will use the current average interest rate of 1.3 per cent, over a loan tenure of 25 years. Assuming full financing, the maximum loan amount is $258,750.

This comes to a monthly loan repayment of about $1,010.70. Over 25 years you would repay $303,209.32 with total interest repayments of $44,459.32.

Note that, for the purposes of calculating your servicing ratio, the bank will use an assumed interest rate of 3.5 per cent; even if the actual rate is much lower. So to meet the MSR using the loan above, you would need a monthly income of around $4,318.

| Address | Executive | Lease remaining (years) | Estate |

| 274B Jurong West St 25 | $426,714 | 80 | Jurong West |

| 470 Segar Rd | $430,000 | 80 | Bukit Panjang |

| 274A Jurong West Ave 3 | $430,000 | 80 | Jurong West |

| 682 Choa Chu Kang Cres | $445,500 | 78 | Choa Chu Kang |

| 274C Jurong West St 25 | $448,000 | 80 | Jurong West |

| 468C Admiralty Dr | $450,000 | 79 | Sembawang |

| 275 Choa Chu Kang Ave 2 | $450,000 | 72 | Choa Chu Kang |

| 529 Choa Chu Kang St 51 | $450,000 | 73 | Choa Chu Kang |

| 472 Sembawang Dr | $452,500 | 79 | Sembawang |

| 408 Sembawang Dr | $454,000 | 79 | Sembawang |

This is due to a lower volume of transactions. The above is based on the lowest transactions we’ve found overall, as of end-April 2021.

Important: Due to the higher income of most Executive Flat buyers, you may be asked to take a bank loan instead. Do prepare for the possibility.

We will use the median of around $448,000 as an estimate:

Assuming full financing, this is 10 per cent of the price or value, whichever is lower. This must be paid in any combination of cash or CPF. We will assume, for this example, that the price and valuation are almost similar.

This comes to a down payment of about $44,800.

This is $8,040, payable in any combination of cash or CPF (see the IRAS website for details on how BSD is calculated)

ALSO READ: Single and 35 years old? Here are your HDB options (BTO + resale affordability calculations)

We will assume the maximum loan quantum of $403,200, for 25 years. The HDB loan has an interest rate of 2.6 per cent per annum. This comes to about $1,829.20 per month.

The total repayment over 25 years will come to about $548,758.64, with total interest repayments of close to $145,558.64.

To meet the Mortgage Servicing Ratio (MSR), the loan repayment must not exceed 30 per cent of your monthly income. Based on the above loan repayment, your minimum income should be at least $6,097.30.

Assuming full financing, this is 25 per cent of the price or value, whichever is lower. The first five per cent of any property purchase must always be paid in cash, while the next 20 per cent can be paid with cash or CPF.

We will assume, for this example, that the price and valuation are almost similar.

This comes to a minimum cash down payment of $22,400 . The next part of the down payment comes to $89,600, payable in any combination of cash or CPF.

As above: $8,040, payable in any combination of cash or CPF

As before, we will use the current average interest rate of 1.3 per cent, over a loan tenure of 25 years. Assuming full financing, the maximum loan amount is $336,000.

This comes to a monthly loan repayment of about $1,312.44 . Over 25 years you would repay $393,732.68 with total interest repayments of $57,732.68.

Note that, for the purposes of calculating your servicing ratio, the bank will use an assumed interest rate of 3.5 per cent; even if the actual rate is much lower. So to meet the MSR using the loan above, you would need a monthly income of around $5,606.98.

[[nid:516631]]

It’s possible that the seller’s asking price will exceed the actual valuation; such as if the asking price is $488,000, but the valuation by HDB comes to $460,000. The $28,000 difference would be the COV.

Also note that the valuation is only revealed after you have already agreed on the price. As such, we advise against any assumptions that you won’t have to pay cash; even if you’re eligible for an HDB loan.

As bank and HDB loans are based on the lower of the price or valuation, the COV amount has to be paid in cash. COV can be unpredictable, as HDB does not publish the data for COV.