October 2023: COE quota forecast to remain level come November

PHOTO: sgCarMart

As COE premiums tower over at record heights — and as the LTA continues to make one-off changes — it appears unlikely that the quota will rise in November.

After $100,000, then $120,000 became the new normal to pay for a COE, will $140,000 now be the standard moving forward?

Every half-year period has seemingly brought with it revisions to the COE supply calculation methodology, all of them, to help take the relentless, upwards pressure off premiums. The latest one, in fact, was the most drastic.

It involved an unprecedented one-time adjustment of approximately 6,000 additional COEs that the LTA is still bringing forward from impending de-registrations, to be distributed gradually over the next few quota periods.

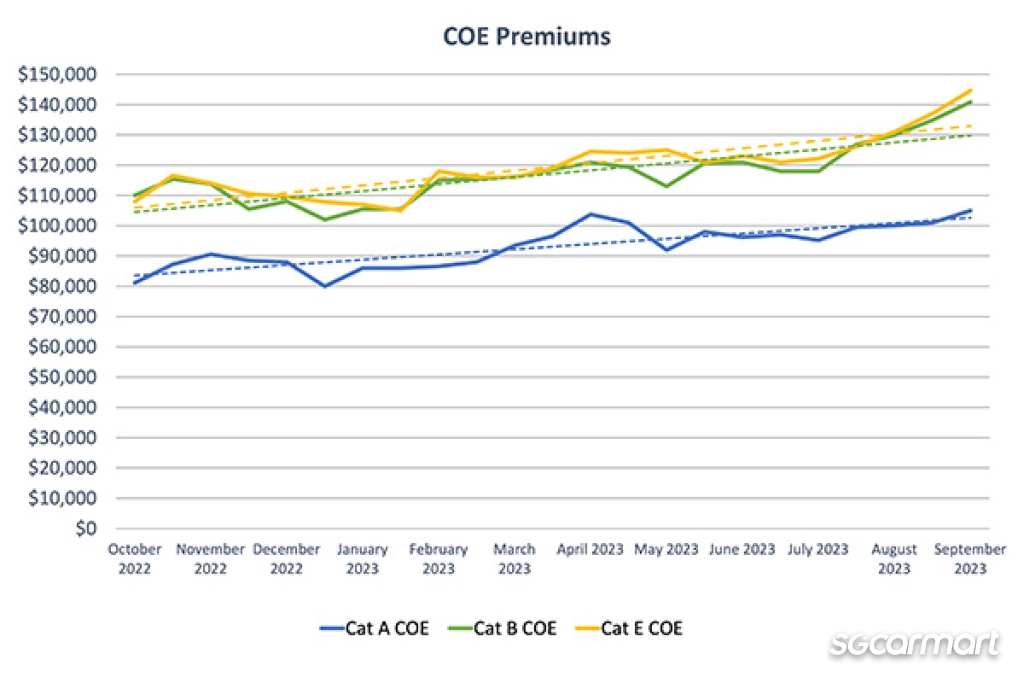

Alas, none of that has seemed to work. Despite a short (and very slight) reprieve in July, persisting climbs in August, and especially September, have left COE premiums in all categories towering over at staggering new heights.

When averaged out over July to September, it's worth noting that on paper, the overall increase in COE premiums doesn't look too absurd when compared to the period of April to June. Cat A climbed "just" 1.8 per cent, while the open Cat E crept up a more significant 6.2 per cent. Cat B saw the largest increase, with a 7.7 per cent increase.

These numbers do not reflect, however, the fact that all categories have continued to break new (and unfathomable) records. At the time of writing, Cat A stands at $105,000, Cat B, at $140,889, and Cat E, at an even more eye-watering $144,640 — all of which are all-time highs.

The black-boxed nature of the car market in Singapore still makes it hard to nail down exactly what is keeping the pedal on the gas for insane COE prices.

Still, industry-insiders and observers have outlined a few reasons for the most recent surge — including a rush to meet year-end sales targets by some dealers, as well as uncertainty (back in mid-September) about the future of rebates and incentives for EVs and cleaner-energy models. These were initially slated to expire by year-end.

Regarding the latter, we now know that the EV Early Adoption Incentive (EEAI) will be extended to 2025, but with a lower maximum rebate. The Band A2 rebate quanta for the Vehicular Emissions Scheme (VES) will also be lowered — both to come into effect in 2024.

Still, yet another surprise announcement just last Friday by the LTA appears to indicate that it is bracing the market for even more impact as a result of these amended incentives — it's taking an additional 300 COEs from the aforementioned pool of 6,000, and inserting them into Cat A for the month of October 2023.

To our knowledge, this is only the second time that the LTA has altered the quota mid-way through a three-month period - and as you'll soon see, convolutes the process of forecasting even further...

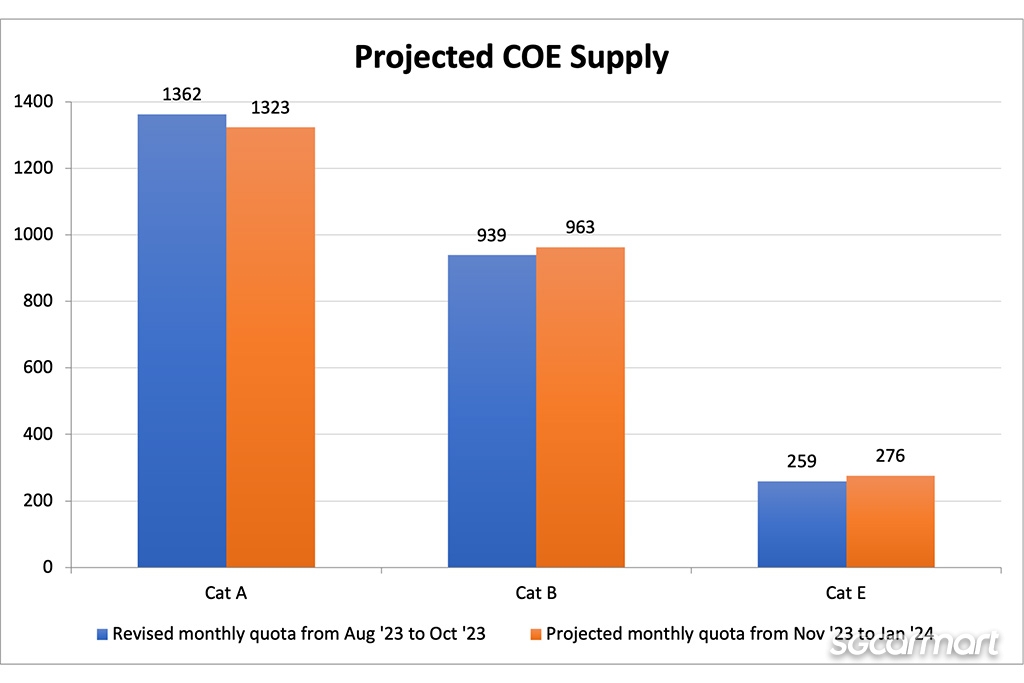

The current COE quota period we're in — spanning August to October — marks the second quarter to be benefitting from the one-time bumper adjustment of 6,000 COEs that the LTA announced back in May. To recap, this sum is being drawn from the impending de-registrations of cars with five-year non-extendable COEs, and will be spread out over a few quarters — including the November 2023 to January 2024 period.

Our previous forecast estimated that the August to October period would be getting an additional 1,027 COEs — with 65 per cent apportioned to Cat A, and 35 per cent apportioned to Cat B. While this number came very close to the official figure of 1,025 additional COEs announced back in July by the LTA, more went to Cat A than Cat B (700, versus 325).

As mentioned, however, we must now consider the fact that an additional 300 COEs are being added to Cat A for the month of October — bringing the total number of additional COEs for the August-October period to 1,325.

This also means that although the LTA had declared a monthly average of 1,262 for Cat A back in July, the figure for three-month period is now effectively 1,362.

Here's where you'll have to bear with us, as the calculation methodology is complicated further.

Till date, the LTA has not explicitly stated the number of quarters it intends to spread the total pool of 6,000 COEs out over — but considering the 856 allocated to the previous quarter, and the 1,325 now allocated to the prevailing period, we're working on the assumption that a total of six quarters will benefit from the boost (each quarter getting in the ballpark of a 1,000 additional COEs).

That leaves us with a remainder of 3,819 COEs at the end of October, to be spread out over four remaining quarters (again, rough estimates) — which in turn, gives us 955 additional COEs for the November 2023 to January 2024 period.

Dividing this figure out by the averaged-out proportions derived from the current and previous quarters will leave us with a 70 per cent allocation towards Cat A, and 30 per cent allocation towards Cat B.

In turn, using these numbers for the next period suggests that the COE supply for private passengers is effectively set to remain level on the whole — with a drop in Cat A mitigated only slightly by gentle increases for Cat B and Cat E.

Percentage-wise, Cat E is forecast to rise the most significantly — by seven per cent from the current monthly average of 259, while Cat B is projected to rise more gently — by two per cent rise — from its prevailing monthly average of 939. Conversely, supply in Cat A is set to slide by two per cent from its current (bolstered) monthly average of 1,362. Interestingly, the supply for Cat A in November would have risen slightly, if not for last Friday's announcement.

Again, we need to caveat that no one knows for sure how exactly the LTA intends to redistribute the COEs to each quarter — and indeed, how it will split the supply between Cat A and Cat B. Things may just change again, especially if the Singapore Motorshow returns in January and sparks a boost in orders.

Sgcarmart does its best to use a pool of popular models from authorised dealers to analyse the general price trends of new cars.

It may be hard to believe given today's COE prices, but based on our sample, there was a gentler three per cent increase in new car prices over the past quarter, when compared to the tri-monthly average between April to June 2023. (June saw a 5.4 per cent increase.) The number is coherent with how COE prices have tracked, suggesting that dealers are moving their car prices dutifully in step.

Again, any increase at all is bad news for today's car buyers; the price of the Toyota Corolla Altis Elegance, which we're using as the benchmark for family cars once more, is now retailing at more than $170,000 with COE.

But apart from our bread-and-butter Cat A cars, it's worth turning your attention to our compact and mid-sized luxury sedans too.

Germany's two arch-rivals — the BMW 3 Series and Mercedes-Benz C-Class — are now well above the $300,000 mark. And while we're still not there yet, might we one day enter the era of seeing their larger siblings (and our favourite mid-sized executive sedans) — the 5 Series and E-Class — near the half-million-dollar mark?

These were cars you'd expect to attain some distance below $300,000 in the past. Instead, the all-new, eighth-generation 5 Series was recently launched at a hair's breadth under $400,000. Meanwhile, your entry point to the E-Class range — the E300e Avantgarde — is currently being sold by Cycle & Carriage at $407,888.

One final interesting phenomenon to note is the fact that we are continuing to see dealers rework their lineups, ostensibly to fit the current market.

For example, Volkswagen Singapore has stopped listing the price of the Category A-friendly Volkswagen Golf in its entry-level Life trim; the attention appears to have shifted in favour of the more premium Life Plus and R-Line.

Meanwhile, Eurokars has officially stopped selling the highest-end Astina trim of the Mazda 3 Sedan (only the Hatchback is offered exclusively as the Astina), as well as the mid-tier Luxury trim of the Mazda CX-5.

Over the three-month period between June 2023 to August 2023, these were the five most listed used cars on Sgcarmart.

| Model | Year of registration | Average depreciation (approx.) |

| Honda Vezel 1.5A X | 2016 | $15,665/year |

| Mazda 3 1.5A Sunroof | 2017 | $13,450/year |

| Honda Civic 1.6A VTi | 2018 | $15,687/year |

| Mercedes-Benz C-Class C180 Avantgarde | 2017 | $20,988/year |

| Nissan Qashqai 1.2A DIG-T | 2017 | $14,537/year |

We previously mentioned that the annual depreciation figure for the Honda Vezel 1.5A X, registered in 2016, had finally breached the $15,000 line when averaged out across the three months — and it now appears that the $16,000 line is just around the bend. For the month of August, the average annual depreciation figure of the crossover was $15,810.

Other cars that made a splash outside of the top five this month include the Hyundai Elantra, registered in 2018, and the Toyota Corolla Altis Elegance, registered in 2017.

Elsewhere, the volume of listings for the top five models — which had jumped significantly across the last two three-month periods — remains high, suggesting that consumers are continuing to turn to the used car market.

ALSO READ: Open category COE hits record high of $152,000 as large car premiums break records