Retiring with $6,000 monthly: How much do I need to earn now?

PHOTO: Pexels

A recent survey by OCBC turned up an interesting finding. Younger Singaporeans desire to live it up during retirement with a lifestyle that would cost a cool $6,000 a month.

Of course, there's nothing wrong with aspiring to a luxurious (some would say excessive) retirement. However, is this sum practical for the average Singaporean?

How much would you have to earn today in order to have a retirement budget of $6,000 every month?

Let's do some number crunching to find out.

Let's assume the following:

Okay, you just have to accrue $1.8 million by the time you retire, easy-peasy. So how much do you need to earn in order to reach this figure?

Assuming you're starting at age 30, that means you have 35 years to build up your retirement savings. You can reach $1.8 million by putting aside at least $4,286 every month for the next 35 years.

Add another, say, $4,000 to meet your basic monthly expenses, and that means your take-home pay would have to be at least $8,300 (rounded up). Which therefore means, your gross salary has to be at least $10,375 per month.

For those of you lucky 30-year-olds who are already earning this salary (and can maintain this level of income for the next 35 years straight), you can stop reading and go enjoy your fancy wine while admiring the sunset from your balcony.

For the rest of us, we have some more numbers to crunch, so buckle up.

Compared to pure saving, investing your money is the smarter (some may say only) way to attain the retirement income you want. So how much would you need to invest to hit $1.8 million by age 65?

Again, we need to make some assumptions:

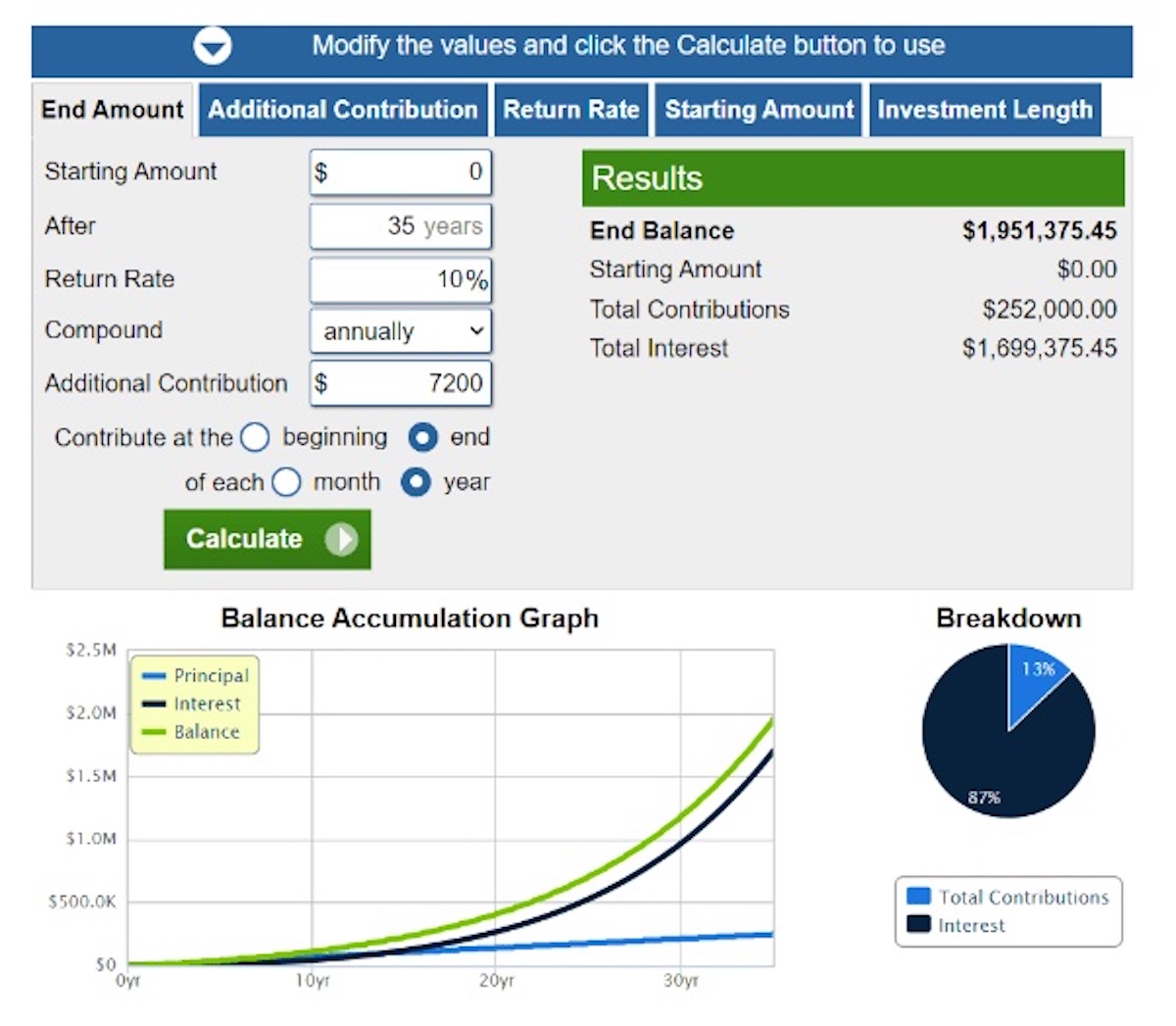

Using this online investment calculator, we see that Investing $7,200 per year (or $600 per month) for 35 years, at a compounding growth rate of 10 per cent will net us $1.95 million at the end.

This is more than enough to fund our luxe retirement lifestyle.

Investing $600 each month is definitely a lot more doable, so does it mean that the young Singaporeans that indicated a preference for the high life in OCBC's survey are actually on to something?

There are two key assumptions we have to look more closely into.

One, the investment timeline — the longer you invest, the faster your money grows. Two, that your investment portfolio achieves a real rate return of least 10 per cent per year.

Let's take a look at each of these in turn.

Here's a side-by-side comparison between someone who started investing at age 30 versus someone at age 35. All other factors remain the same.

| Starting at 30 (35 years to invest) | Starting at 35 (30 years to invest) | |

|---|---|---|

| Yearly investment | $7,200 | $7,200 |

| Portfolio growth rate | 10 per cent | 10 per cent |

| Portfolio value at age 65 | $1.95 million | $968,357 |

As you can see, starting to invest just five years later results in a final portfolio value that is a staggering 51 per cent lower!

This, then, should clearly illustrate the power of compounding interest, but if you need a visual, here's how the growth of your portfolio looks when plotted on a graph:

Notice how the curve gets sharper the more time passes?

The takeaway: Starting early is the most important factor when investing your money, so if you're serious about wanting that $6,000 retirement (or even any sort of viable retirement), start investing now.

We'll preface this section by saying that a 10 per cent yearly growth rate — which a century's worth of historical data tells us is realistic — may not be achievable for everyone.

This is because in reality, the stock market doesn't go up by a neat 10 per cent each year. To wit: the S&P 500 is down nearly 18 per cent from a year ago, at the time of writing.

Therefore, an element of luck is involved, if your investment timeline happens to fall within a bear market cycle, your returns will likely be lower — which means a smaller retirement nest egg.

Also, we need to take inflation into account. Singapore's average inflation rate over the past 10 years (2012 to 2021) is 1.06 per cent.

That seems insignificant, but in practice, inflation has a nasty habit of spiking from time to time, manifesting in sharply increased costs of living.

This can affect your retirement lifestyle in the short term (forcing you to downgrade from business class to economy class).

Because inflation is a fact of life, your retirement portfolio has to take that into account. This means that you should be aiming for a yearly portfolio return of 12 per cent instead of 10 per cent — allowing a two per cent margin for inflation.

What about your CPF contributions, which you duly pay into every month? Well, it's complicated.

You see, it depends on what you believe is the best use of your CPF monies — leaving it for retirement, or using it to fund your property, which you can then use for rental income in retirement. Both choices have their pros and cons, so we'll leave it to your discretion.

What's for sure is that you will have some amount of CPF Life payouts starting from age 65 or 70, which you can use to supplement your retirement income.

There is one other thing we've not addressed: inflation erodes purchasing power, which means $1 today will be worth less than $1 by the time you retire.

Which means that if you really want the kind of lifestyle that $6,000 today affords, you might find yourself needing closer to $12,000 or more.

As if trying to plan for retirement in the most expensive city in the world is not already stressful enough.

Our advice? Temper your expectations, and focus on what is really important. Set up a retirement plan with a qualified professional, and start building your retirement nest egg now.

ALSO READ: Is it enough to retire with $6,000 in monthly expenses given the current inflation rate?

This article was first published in ValueChampion.