A review of 4 undervalued real estate investment trusts

PHOTO: Pixabay

With the recovery in stock market since the March sell down, we have seen a slew of Real Estate Investment Trust (“REITs”) that manage to stage a strong recovery in its share price.

This has resulted in some of the REITs being overvalued as they are trading above their book value, example: Keppel DC REIT (Price to Book Ratio: 2.49 times), ParkwayLife REIT (Price to Book Ratio: 1.85 times) and Mapletree Industrial Trust (Price to Book Ratio: 1.83 times).

In this article, we will be looking at 4 REITs that are undervalued and currently trading below their book value.

The 4 REITs are: Sasseur REIT (Price to Book Ratio: 0.86 times), IREIT Global (Price to Book Ratio: 0.81 times), Dasin Retail REIT (Price to Book Ratio: 0.67 times) and CapitaLand Retail China Trust (Price to Book Ratio: 0.70 times).

Sasseur REIT is the first retail outlet mall REIT listed in Asia. Sasseur REIT offers investors the unique opportunity to invest in the fast-growing retail outlet mall sector in the People’s Republic of China (the “PRC”) through its initial portfolio of four quality retail outlet mall assets strategically located in fast growing cities in China such as Chongqing, Hefei and Kunming, with a net lettable area of 312,844 square metres.

Sasseur REIT is established with the investment strategy to investing principally, directly or indirectly, in a diversified portfolio of income-producing real estate which is used primarily for retail outlet mall purposes, as well as real estate related assets in relation to the foregoing, with an initial focus on Asia.

Sasseur REIT's Entrusted Management Agreement (“EMA”) rental income for 1H FY2020 came in at RMB268.1 million (S$53 million), which is a drop of 10.4 per cent year-on-year as a result of a slowdown of retail sales amid the Covid-19 pandemic.

As a result of the fall in sales figure, the variable component of the rental income has suffered a 38.1 per cent year-on-year drop.

Despite that, the fall in rental income was cushioned by the fixed component of EMA rental income, which saw a 3.9 per cent year-on-year growth.

The amount available for distribution to Unitholders in 1H FY2020 was $34.2 million, 12.1 per cent lower compared to $38.9 million for 1H FY2019.

The decrease was mainly attributable to lower sales, one-off reversal of trust expenses and the decrease is partially offset by lower finance costs and tax expense.

Sasseur REIT has seen a minor dip in its total assets to $1.76 billion as of June 30, 2020. This was due to the drop in cash and short-term deposits and other assets. However, the drop was cushioned by the increase in the value of its investment properties.

Sasseur REIT’s total liabilities has fallen to $677.3 million as of June 30, 2020. This was contributed from the decrease in the amount of other liabilities despite the increase in loans and borrowings.

As a result of the increase in net assets, Sasseur REIT’s Net Asset Value (“NAV”) per share has seen a slight increase from 89.2 cents as of Dec 31, 2019 to 90.3 cents as of June 30, 2020.

However, Sasseur REIT’s aggregate leverage has risen by 0.3 percentage points to 28.1 per cent as of June 30, 2020 as a result of a sharper fall in its total assets when compared against the fall in its total liabilities.

IREIT Global (“IREIT”) is a Singapore real estate investment trust with the investment strategy of principally investing, directly or indirectly, in a portfolio of income-producing real estate in Europe which is used primarily for office, retail and industrial (including logistics) purposes, as well as real estate-related assets.

IREIT completed its Initial Public Offering (“IPO”) and was listed on the Main Board of the Singapore Exchange Securities Trading Limited on Aug 13, 2014.

IREIT’s current portfolio comprises five office properties in Germany, strategically located in Berlin, Bonn, Darmstadt, Münster and Munich and four properties in Spain, located in Madrid and Barcelona.

For 1H FY2020, IREIT Global’s gross revenue came in at €17.9 million (S$28 million), which is a year-on-year increase of 2.6 per cent, and mainly coming from both the new lease at Münster South Building which commenced in July 2019 and positive effects from the finalisation of prior years' service charge reconciliation.

However, with the 11.6 per cent year-on-year increase in property operating expenses, IREIT Global’s net property only registered a 1.4 per cent year-on-year increase to €15.6 million in 1H FY2020.

Therefore, IREIT Global’s income to be distributed to unitholders remain largely flat at €11.6 million for 1H FY2020.

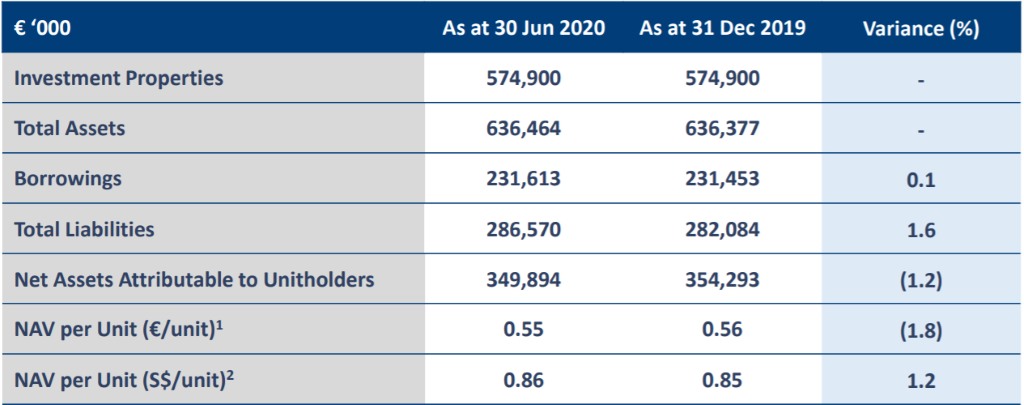

The appraised value of the German portfolio remained unchanged at €574.9 million as at June 30, 2020, despite the Covid-19 virus outbreak, and this has contributed to the stability of the REIT in terms of total assets and NAV.

In terms of total liabilities, IREIT Global saw an increase of 1.6 per cent as at June 30, 2020 due to the increase in short-term borrowings, which was offset by the partial repayment of long-term borrowings.

Therefore, with total assets remain unchanged and the increase in total liabilities, net assets attributable to unitholders fall by 1.2 per cent when compared against the figure on Dec 31, 2019.

The NAV per unit (€/unit) as at June 30, 2020 came in at €0.55, a drop of €0.01 as at Dec 31, 2019.

Despite the drop in NAV in Euro terms, IREIT Global has saw an increase of 1.2 per cent in NAV in Singapore Dollar terms due to favourable exchange rate as a result of the depreciation of Singapore Dollar.

Dasin Retail Trust is a China retail property trust providing direct exposure to the fast-growing Guangdong-Hong Kong-Macau Greater Bay Area listed on the Main Board of the Singapore Exchange Securities Trading Limited on Jan 20, 2017.

Dasin Retail Trust’s principal investment mandate is to invest in, own or develop land, uncompleted developments and income-producing real estate in Greater China (comprising People’s Republic of China (“PRC”), Hong Kong and Macau), used primarily for retail purposes, as well as real estate-related assets, with an initial focus on retail malls.

The portfolio of Dasin Retail Trust comprises seven retail malls strategically located in Foshan, Zhuhai and Zhongshan Cities in PRC.

Dasin Retail Trust is managed by Dasin Retail Trust Management Pte. Ltd. (“Trustee Manager”).

The Trustee-Manager’s key objectives are to provide Unitholders of Dasin Retail Trust with an attractive rate of return on their investment through regular and stable distributions to Unitholders and to achieve long-term sustainable growth in DPU and net asset value per Unit, while maintaining an appropriate capital structure for Dasin Retail Trust.

Revenue for 1H FY2020 was 5.2 per cent higher year-on-year by approximately $1.8 million mainly due to the contribution from Doumen Metro Mall which was acquired in September 2019, partially offset by lower rental income from Ocean Metro Mall, Shiqi Metro Mall, Xiaolan Metro Mall and Dasin E-Colour arising from the impact of Covid-19 as well as rental rebates provided to the tenants.

For 1H FY2020, the major unitholders of the trust have waived a portion of their entitlement to the distribution.

As a result, Distribution Per Unit (“DPU”) stands at 1.92 cents. If there are distribution wavier in place, DPU could potentially drop by 30 per cent to only 1.35 cents.

As at June 30, 2020, Dasin Retail Trust’s total assets amount to $1.90 billion, a fall of 2.8 per cent when compared against the figure as at Dec 31, 2019.

The fall can be contributed from the drop in valuation of its investment properties and a lower cash and cash equivalent. However, the drop was partially offset by the increase in other assets.

Dasin Retail Trust’s total liabilities saw a dip of 0.4 per cent when compared against the figure as at Dec 31, 2019.

The dip can be seen from the drop in other liabilities and was partially offset by an increase in the trust’s loan and borrowings.

This has resulted in a decrease in net assets to $836 million as at June 30, 2020. Coupled with the increase in the number of issued and issuable units, Dasin Retail Trust saw a drop in NAV per unit to $1.28, compared to an NAV of $1.37 as at Dec 31, 2019.

CapitaLand Retail China Trust (“CRCT”) is Singapore’s first and largest China shopping mall real estate investment trust, with a portfolio of 13 shopping malls.

It was listed on the Singapore Exchange Securities Trading Limited on Dec 8, 2006.

CRCT was established with the objective of investing on a long-term basis in a diversified portfolio of income-producing real estate used primarily for retail purposes and are located primarily in China, Hong Kong and Macau.

CRCT's geographically diversified portfolio of quality shopping malls, with a total gross floor area of approximately 1.0 million square metres, is located in eight Chinese cities.

The malls are CapitaMall Xizhimen, CapitaMall Wangjing, CapitaMall Grand Canyon and CapitaMall Shuangjing in Beijing; Rock Square (51.0 per cent interest) in Guangzhou; CapitaMall Xinnan in Chengdu; CapitaMall Qibao in Shaghai; CapitaMall Minzhongleyuan in Wuhan; CapitaMall Saihan and Yuquan Mall in Hohhot; CapitaMall Xuefu, CapitaMall Aidemengdun in Harbin and CapitaMall Yuhuating in Changsha.

As at June 30, 2020, CRCT's total asset size is $3.8 billion, increasing more than fivefold from the Trust's listing.

CRCT’s gross revenue came in at RMB510.9 million for 1H FY2020, a decrease of RMB43.5 million, or 7.8 per cent lower than 1H FY2019.

The decrease was attributable to the various rental relief measures that are undertaken by the REIT itself.

Furthermore, the absence of CapitaMall Erqi’s contribution following the pre-termination of lease of its anchor tenant in 4Q FY2019 and the completion of divestment in May 2020 also resulted in the fall in gross revenue.

As a result of the rental relief measures, increase in property expenses, absence of capital distribution and finance costs, CRCT’s distribution amount to unitholders came in at $37.0 million, a decrease of $14.1 million, or 27.7 per cent lower than 1H FY2019.

CRCT’s gearing ratio has dipped by 2.2 percentage points from 35.8 per cent as of March 31, 2020 to 33.6 per cent as of June 30, 2020.

The dip can be attributed to the disposal of CapitaMall Erqi in May 2020, which resulted in the strengthening of the REIT’s balance sheet.

As a result of a lower earnings in 1H FY2020, CRCT’s interest coverage ratio suffered a slight dip of 0.3 times to about 4.0 times as of June 30, 2020. However, this figure is still higher than the stipulated regulation of 2.5 times.

With the fall in benchmark interest rate, CRCT’s average cost of debt has fallen by 0.1 percentage points as of June 30, 2020.

The fall in the cost will have a positive impact in terms of a lower finance cost moving forward.

For the 4 REITs that mentioned above, they have witnessed a certain degree of negative impact in their latest financial performance due to the Covid-19 pandemic.

The lockdown has impacted their rental income as footfall at their respective shopping malls has fall drastically. Therefore, investors might value these REITs at a discount due to the nature of the properties.

In addition, most of their investment properties are located outside of Singapore and therefore the REITs will be faced with the fluctuation in currency exchange as they receive rental income in foreign currency and distribute out in Singapore Dollar.

This could also potentially result in the REITs being undervalued as they could see a potential loss in rental income due to currency exchange fluctuation.

This article was first published in Investor-One.