Ultimate Robo advisors Singapore guide. Key facts you need to know (2020)

PHOTO: Unsplash

Robo advisors are digital platforms that use algorithms to automate your investment portfolios. The usage of algorithms instead of active human management is the key reason that fees are generally lower than that of actively managed funds.

One can get started investing through a Robo Advisor pretty quickly, usually, your account can be set up in 10-15 minutes.

When you sign up through the Robo online platform, all you need to do is input your risk profile (aggressive, conservative, balance, etc) and the Robo advisor will start to make a recommendation on your portfolio structure using their algorithm.

The next step is usually to fill in your personal particulars and providing a scanned copy of your IC as well as your banking and funding details.

Once the funds are received by the Robo advisors, they will automatically invest it for you with periodic rebalancing. SIMPLE! (more details below). For those looking for a quick example, I have written a Guide to Syfe and how to open an account in less than 10 minutes.

We present to you the ultimate Robo Advisors Singapore guide in this article.

On average, Robo advisors in Singapore have management fees ranging from 0 per cent -1 per cent of the asset under management (AUM) compared to your standard funds where fees are typically in excess of 1 per cent, at times averaging close to the 2-3 per cent range.

The low-cost nature of Robo advisors, coupled with their low minimum initial investment requirement is what makes this an ideal platform for the man-in-the-street to get started on their investment journey.

The majority of Robo advisors in Singapore uses Exchange Traded Funds (ETFs) as their investment platform. An ETF is a basket of investments, including stocks, commodities, bonds, etc that trade on an exchange, just like a stock. ETFs are generally passive in nature which tracks a particular index/theme.

The advantage of buying an ETF vs. individual stocks can at times be summarised as having a diversified exposure at a low cost (total expense ratio is typically around 0.4 per cent)

However, as can be seen, there are some Robo advisors that invest in funds as well as a hybrid of stocks/ETFs. Typically, funds tend to have a higher total expense ratio (TER) as compared to ETFs due to the former's active management nature.

Hence this is an area to pay attention to when investing in a Robo advisor.

Total charges = Robo advisor's management fee + ETF/Fund management fee (usually not actively disclosed)

It would hence be erroneous to evaluate the fee structure of Robo advisors based on just their management/advisory fee structure and come to the conclusion that one platform is cheaper than the other.

We will need to understand their underlying investment platform (ETFs, funds, stocks, etc) and assess the expense nature of investing in these asset classes as well.

We will be providing an analysis of the individual Robo advisors base on their fee structure as well as their underlying investment platform.

But first, let's start with some of the basics….

In the first step, Robo advisors will construct a portfolio for you based on a few key variables such as your goals, investment horizon, risk profile, financial situation, etc.

In the second step, the investor will be allocated to one of the Robo advisor's portfolio based on the investor's investment profile.

In the third step, the investor can then fund the account through a lump sum investment or monthly recurring investment, similar to a regular savings plan.

In the fourth step, the Robo advisors will periodically re-balance the portfolio if required. You can easily monitor the performance of the portfolio on the spot.

We list down some of the benefits of Robo advisors which we think matters to investors the most. We highlight the 4 key BENEFITS of using a Robo advisor that investors should be aware, in our view.

As explained, Robo advisors typically have much lower advisory fees compared to a typical mutual fund. Robo advisor fees range from zero (less than $50,000 invested in Kristal.AI) to about 1.0 per cent ($10,000 or less invested with Smartly).

This is compared to mutual funds that typically charge advisory fees easily in excess of 1.0 per cent, at times trending towards the 2 per cent-3 per cent range. Even after including ETFs management charges, some of the more price-competitive Robo advisors still have all-in charges less than 1.0 per cent.

Typically to create your own personalised portfolio, that will require a substantial initial investment amount that is out-of-reach for most beginner investors.

[[nid:469873]]

We see one of the key benefits of a Robo advisor as to the ability to create a personalised portfolio based on the risk profile of an individual.

This is also done at a fraction of a cost (low minimum investment sum) compared to typical mutual or institutional funds where the minimum sum could trend to the millions.

Not only does one get introduced to a personalised portfolio suitable to his/her risk profile, but the investments also tend to be diversified across asset classes (equities, bonds, commodities).

This is an advantage over simply investing in a single asset-class ETF/stock.

We see the ability of Robo advisors to provide constant rebalancing of your portfolio to maintain your targeted asset class mix (eg: 60 per cent equity/ 40 per cent bond) as one of the key benefits.

While one could create their own "personalised" portfolio without the need of Robo advisors (use 60 per cent of your available funds to buy equity-related products and 40 per cent to buy bond-related products) periodic re-balancing will become a hassle on a DIY basis.

Robo advisors provide an automated basis for such re-balancing work to be done on a periodic basis. This is a much simpler process compared to manually re-balancing your own portfolio.

The complicated account set-up process is often the key hurdle for the novice investor to get themselves started on their investment journey. Setting up a Robo advisor account is pretty simple and straight-forward, with no requirement for document submission.

You can simply sign up online by creating your online account and transfer the funds seamlessly from your bank account to your investment account.

We list down some of the cons of Robo advisors which we think matters to investors the most. We highlight the 3 key DOWNSIDES of using a Robo advisor that investors should be aware, in our view.

Most of the Robo advisors are algorithm-driven, hence portfolio customisation is limited at best and cannot deviate significantly from the algorithm's parameters.

If you are a savvy investor who wishes to choose your own securities or ETFs, there are limited options. Kristal.AI is, however, one such Robo advisor that allows you to customise your own portfolio based on certain thematic ETFs.

Besides the typical advisory fees charged by the Robo advisors themselves as well as management fees incurred by the management of the ETFs, hidden fees such as currency conversion fees could eat into the returns of your portfolio.

Most of the Robo advisors invest in USD denominated ETFs. A significant depreciation of the USD against SGD will negatively impact the returns of a Singapore-based investor.

There are also withholding taxes incurred on the investor level for dividend/income funds that are domiciled in the US. This will further reduce the net returns of your bond portfolio.

Despite the low-cost nature of Robo advisors, recurring fees will be incurred for AUM. One would have to question if such recurring expenses accruing to the Robo advisors are justified vs. a DIY approach.

Most beginning investors will, however, lack the knowledge or time to create and monitor the performance of their portfolio. Hence, despite the recurring fees of Robo advisors, it might still be a worthwhile proposition to use one.

For someone who does not have the time and/or knowledge to create their own investment portfolio, Robo advisors will be the ideal platform to kick-start their passive investment journey.

The investment account can be set up electronically in a matter of minutes and with a click of the button, the algorithms will do the heavy lifting of investing your money.

There is no need for active management and you can monitor and track the performance of your portfolio easily through the platform at any point in time.

Investing in Robo advisors tend to have low minimum investment threshold. More importantly, they are often low-cost in nature with all-in fees typically within the 1 per cent region.

What you get by paying 1 per cent/annum could at times be a dedicated investment specialist allocated to your account as well as a diversified portfolio of different asset classes that are re-balance periodically to ensure the best risk-adjusted return.

Most investors tend to be heavily weighted on investments from their home nation. This tends to create a geographic-centric risk that can be diversified away through a Robo advisor, which could adopt an investment strategy of geographical diversification.

Most of the Robo advisors invest in ETFs/funds that are globally diversified which might be an attractive feature for a Singapore-based investor who is currently heavily-weighted on Singapore-listed equities, for example.

Typically, we tend to shun Robo advisors investing directly in funds due to the higher expense ratios associated with investing in funds vs. ETFs. However, there are exceptions as seen from our analysis below.

Launched in 2019, MoneyOwl is a joint venture between Providend and NTUC Enterprise. MoneyOwl offers "bionic" advice through a combination of humans and robots to deliver low-cost investment solutions with a human touch.

Currently, MoneyOwl offers 5 different investment options - Equity, Growth, Balanced, Moderate and Conservative based on a mix of 3 different Dimensional Funds:

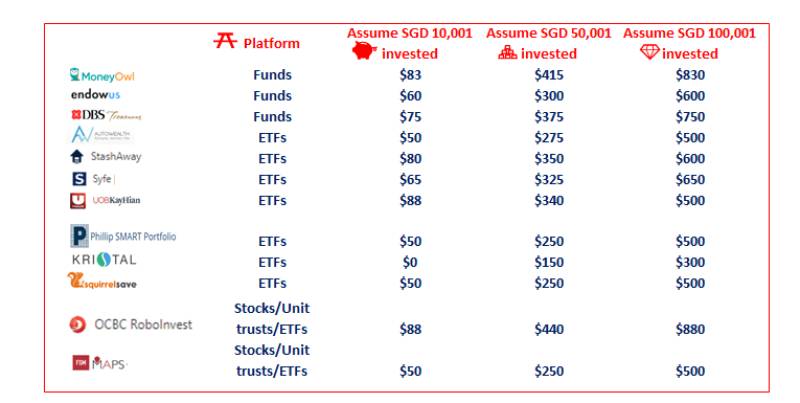

MoneyOwl charges an advisory fee of 0.65 per cent (promotional advisory fee of 0.50 per cent from now to 31 Dec 2019) and levies a custodian/platform fee of 0.18 per cent, bringing total fees to 0.83 per cent.

According to them, the fund TER amounts to a manageable 0.31 per cent - 0.37 per cent which brings total charges to approx. 1.2 per cent. The low management fees of the Dimensional funds, as opposed to other more actively managed funds, is a key differentiating factor here that allows MoneyOwl to remain competitive vs. other Robo advisors.

MoneyOwl's low minimum initial investment amount of $100 with an option for an $50/month regular saving plan is ideal for the regular man in the street to kick start their investment journey. It also allows for your SRS funds to be invested.

Endowus is a Singapore-based investment platform that enables people to invest their CPF, SRS and cash savings better at the lowest cost possible. This fee-only firm invests in institutional share classes of funds, where management fees are significantly lower.

These funds are offered by Dimensional Fund Advisory (similar to MoneyOwl) and PIMCO.

When you create an Endowus account, they will create a trust account in your own name at UOB Kay Hian. This trust account will handle your assets and process the transactions you make on the Endowus platform.

[[nid:484070]]

The ability to use our CPF funds to invest is a major advantage that this platform has over the rest, in our view. The platform cost of using CPF/SRS funds are also lower at 0.40 per cent flat.

Endowus charges a fee of 0.25 per cent-0.60 per cent, although the lower tier charges are applicable only to likely high net-worth with AUM of $5 million and more. For common folks like you and me, the advisory fee is at 0.60 per cent for AUM under $200,000.

Endowus also guided that investors have to pay fund management fees of between 0.43 per cent to 0.64 per cent (could potentially be lowered ahead). This is higher than MoneyOwl's fund management fees range of 0.31 per cent - 0.37 per cent.

However on the basis of a total charge, Endowus fees of approx. 1.03 per cent - 1.24 per cent is pretty comparable.

Compared to MoneyOwl, Endowus trumps in its potential CPF investment option although MoneyOwl, with its bionic touch, has that added human element advantage.

I believe the key selling point for Endowus and MoneyOwl is access to Dimensional funds. I have written about Dimensional funds in this article: Dimensional Funds. Are they worth their weight in gold?

Endowus also has the CPF investment element which currently is not available from other Robo advisors. However, their CPF investment option currently does not include Dimensional funds.

DBS digiPortfolio used to be only available for DBS Treasures clients who have assets under management of $350,000 and above.

However, DBS announced in early September that it will be extending its DBS digiPortfolio to retail investors with a multi-currency account through the launch of two portfolios comprising Singapore and UK-listed ETFs.

The Asia Portfolio has a minimum investment sum of $1,000 while investors seeking global diversification can opt for the Global Portfolio which offers UK-listed ETFs for a minimum investment sum of US$10,000 (S$140,000).

[[nid:481563]]

However, since the Global Portfolio is classified as a Specified Investment Product (SIP) and denominated in USD, investors must be willing to take on currency risk and must pass a Customer Account Review.

Unlike the offering for Treasures clients which invest in funds, the retail offering is ETFs-based digiPortfolios, but with a limited scope of SGX or UK-listed ETFs, with a collection of four to seven ETFs in total that represent between 200 and 13,000 holdings in a single transaction.

In terms of fees, the advisory fees amount to 0.75 per cent. A typical Singapore ETF such as the Nikko AM STE ETF which tracks the Straits Times Index (STI) has an expense ratio of 0.35 per cent. This brings total charges to approx. 1.1 per cent, again pretty similar to both MoneyOwl and Endowus.

However, in terms of global exposure, this DBS digiPortfolio offering for retail investors is likely at a disadvantage, given that its global exposure is only limited to a small array of UK-listed ETFs.

This could be due to tax-related purposes. UK-listed ETFs are not subject to withholding tax for a Singapore investor.

Most of the Robo advisors in Singapore invest in ETFs as their key investment platform, not surprising given the low-cost nature of ETF investing, which is as easily tradable as a stock.

Some ETF such as the Vanguard ETF VOO has an expense ratio of only 0.04 per cent, making this investment the ideal tool to track the S&P500 index. However, that excludes dividend tax withholding cost which can become rather substantial.

AutoWealth is one of the pioneers of Robo advisors in Singapore, first started in 2015. Like MoneyOwl, AutoWealth has a wealth manager that is assigned to each client, hence having that bionic or hybrid touch that might be an advantage over an all Robo-only advisor (as long as we are not paying higher fees for it).

Unlike some Robo advisors like StashAway which pool investors' money and invests them as a whole, AutoWealth will require investors to open a separate Saxo Capital Markets account (custodian) where client assets are held in legally segregated accounts under their own name.

This means that only you have any legal claims on all your assets in all circumstances.

AutoWealth engages a passive market-returns portfolio investment approach, with essentially a two-fund portfolio. One comprising of Global Equity (MSCI Index) and the other Global Government (US + International) bonds at your desired allocation based on your risk profile to create 4 portfolios:

In terms of investing in global equity assets, AutoWealth typically invests in extremely low-cost ETFs such as Vanguard Total Stock market ETF (VTI) with 0.04 per cent expense, Vanguard FTSE Europe ETF (VGK) with 0.10 per cent expense, etc.

On the bond side, some of the ETFs used are iShares 7-10 Year Treasury Bond ETF (IEF) with 0.15 per cent expenses.

Hence after adding a flat 0.5 per cent advisory fee + USD18/annum in platform fees, the total charges will likely be approx. 0.7 per cent-1.0 per cent, on our estimate, a very competitive amount compared to some of the Robo advisors which we have previously highlighted.

However, this excludes the dividend withholding tax impact which could translate to an additional 0.6 per cent (assume 2 per cent yield) in cost, bringing the total cost to 1.3-1.6 per cent.

Autowealth also provides a personal advisor (similar to MoneyOwl) where an investor can get support through mobile or arrange a face-to-face meeting.

StashAway was started back in 2016 by ex Zalora Group CEO, Michele Ferrario. The company employs a proprietary investment strategy called the Economic Regime-based Asset Allocation (ERAA) which continually monitors economic and market cycles to re-balance accordingly.

Hence unlike AutoWealth's passive investment model, there is more active management based on StashAway's investment methodology. Is this good or bad?

[[nid:424894]]

Well for starters, StashAway charges a 0.2 per cent-0.8 per cent in terms of advisory/management fees and highlighted that the management fees charged by the ETF manager typically average to 0.2 per cent.

This means that all-in charges amount to an attractive 0.4 per cent (above $1 million) -1.0 per cent (below $25,000). That's really attractive for an "actively" managed portfolio. The million-dollar question is whether such "activeness" will result in better or worst performance?

The company offers 31 risk profiles based on 19 ETFs investments spanning across a myriad of sectors and geographies.

Since Dec 2018, investors can also invest their Supplementary Retirement Scheme (SRS) funds via StashAway. This is again an attractive feature, given the limited investment scope for SRS funds.

Another "attractive" feature is its cash management service called Stashaway Simple where an investor can earn a projected 1.9 per cent simply by parking cash with the Robo advisor. Can you really generate 1.9 per cent return? Long answer short, I think it is going to be a challenge to achieve such rates.

Smartly announced its closure on March 24, 2020. Users will no longer be able to log into their accounts from April 18, 2020.

Syfe is one of the latest digital wealth managers launched in July 2019 after raising $5.2 million in seed funding. Again, similar to Smartly, funds in Syfe are held in a Trust Account with DBS Bank while investments are held in a Custodian Account through Saxo Capital.

The Robo advisor uses Automated Risk-managed Investments (ARI) strategy which automatically adjusts your portfolio to ensure enhanced risk-adjusted returns by managing your portfolio's downside risk.

Bottom-line: Focus is on risk management vs returns.

[[nid:486979]]

For example, during the GFC period, its simulation forecasted higher volatility ahead and hence reduced its portfolio exposures to higher-risk equities while during calmer periods like in 2017, the algorithms will increase its exposure to higher-risk assets.

Once an investor set their "maximum" downside risk, one of the Robo advisor's key aims is to avoid breaching that level.

Its investment style seems like the opposite of Smartly which adopts a Modern Portfolio Theory. MPT will theoretically sell appreciating bonds during periods of volatility and buy depressed stocks to ensure that your portfolio remains balanced.

However, the concern over MPT is if the correlation between bonds and equities start breaking down in a particular scenario. For example, in a market downturn, it is expected that bond performance will appreciate, helping to counteract the draw-down from equities. What happens when both asset classes fall in value?

The MPT will still re-balance the portfolio by selling bonds, where declines are likely lower vs. equities and reinvest the proceeds into the latter.

There is no minimum amount for investors to start investing with Syfe. The Robo advisor charges 0.65 per cent in advisory fees which gives you unlimited, free withdrawals and unlimited rebalancing. With ETF fees estimated at 0.15 per cent, that brings all-in charges to approx. 0.80 per cent.

A key feature of Syfe is their REIT platform offering. I have written about Syfe in this article: Syfe Guide. Did Syfe's ARI algorithm outperform in today's market volatility? The company just announced that it has collaborated with SGX to launch a pure 100 per cent REIT portfolio.

This is different from its previous REIT+ portfolio (which is still available) which invests in a mixture of both REITs and government bonds.

Syfe provides one of the cheapest solutions to invest in a portfolio of high-yielding and quality REITs, with a starting fee of 0.65 per cent. Since the invested asset is not a fund nor ETF, there are no additional fees pertaining to its 100 per cent REIT and REIT+ portfolio so all-in cost is just the platform fees of 0.65 per cent.

Similar to Smartly, UTrade Robo engages a Modern Portfolio Theory methodology. The Robo advisor will first identify the set of major asset classes that are invest-able. It will then select low-cost ETFs (typical expense ratios average 0.13 per cent-0.40 per cent) to represent each asset class and use MPT to allocate among the asset classes.

The asset classes are broadly segregated into equities, fixed income and commodities.

The Robo advisors look at ETF selections that are London-listed or Ireland-domiciled ETFs which are not subject to withholding tax at the investor level. This is similar to the DBS digiPortfolio structure that invests in mainly SGX-listed and London-listed ETFs to likely avoid the payment of withholding tax at the investor level.

UTrade Robo has a minimum investment amount of $5,000 and their advisory fees range from 0.5 per cent to 0.88 per cent. Most retail investors will likely have to pay the top-end of the advisory fees of 0.88 per cent.

Add in the typical fund expense ratios of 0.13 per cent - 0.40 per cent and total costs could be at least 1.0 per cent-1.4 per cent which is on the high-end of Robo advisor charges.

Unlike the other Robo advisors, Phillip SMART Portfolio is not driven by an algorithm but is instead managed by a team of investment managers to create a portfolio structure.

Its methodology uses a diversified portfolio of primarily ETFs across geographical regions, countries and industry sectors. However, it may also invest in unit-trusts, closed-end funds, investment trusts, business trusts and Exchange-traded notes (ETN)

While not a "pure" Robo advisor per se, given the lack of an algorithm that drives the investment methodology, investors are not penalized by the high advisory fees, which at 0.50 per cent all-in, is among the most competitive. All-in charges including ETF management fees are likely to be in the region of 1.0 per cent.

Kristal.AI stands out as the Robo advisor with the lowest management fees among its peers with no management fees for accounts of less than $50,000. That in itself is a significant cost-savings of at least 0.5 per cent which is the normal advisory fee for most Robo advisors.

Minimum investment amount of $0.

Kristal.AI's proprietary AI uses an underlying genetic algorithm to choose and modify strategies from a pool of thousands of permutations.

[[nid:482301]]

At each stage, the curated strategies are tested against user-defined objectives with only the "fittest' strategies chosen into a risk-limiting model which optimises asset allocation and maximises returns.

Sounds complicated? Well, you are not alone.

Investing in Kristal.AI is not exactly dummy-proof. The Robo advisor provides a variety of customised ETFs selected by their AI. You will need to decide which of these customised/thematic ETFs or what they termed as Kristal's suit you best. Hence, a certain level of investment knowledge will be required.

The Robo Advisor also provides an ETF basket option which is like a fund of fund structure where there are multiple ETFs being invested concurrently.

There is also a stock basket available for the retail investor which is based on either mimicking selected Gurus or investing in a concentrated portfolio of individual stocks such as the FAANG portfolio or BAT (Baidu, Alibaba, Tencent) portfolio.

This platform looks similar to the US-based Motif platform (just announced its closure to be effective in May 2020), the difference being that the Kristals are all selected by the AI algorithm compared to Motif that is personally created by the man-in-the-street.

If you are a DIY investor, this could be an interesting platform to select your own personaliSed ETFs (or Kristals) all under a single platform with no advisory fees (below $50,000).

However, similar to a Unit Trust, the minimum investment for each Kristal is based on the NAV of that particular Kristals. Hence it will be erroneous to assume that an investment of $10 can allow you to partake in all the ETFs available.

For example, the newly created BAT portfolio has a NAV of US$2,484. With a minimum investment of 1 unit, the minimum investment outlay is US$2,484.

Not the best solution for a Regular Savings Plan approach.

The new kid on the block SquirrelSave is led by Victor Lye who is a corporate entrepreneur with over 25 years' cross-industry experience in investments, insurance, and healthcare.

SquirrelSave is a fully AI-driven investment service offered by PIVOT Fintech, a Singapore-based technology company regulated by the MAS.

An investor will first input its risk level and SquirrelSave will subsequently trawl over 2,000 diversified ETFs to design a personalized portfolio comprising a few selected ETFs whose combined risk prediction matches your chosen risk and gives the highest predicted return for the time horizon.

I tried selecting a portfolio structure and came away rather confuse. First, you are ask to select your age and investment horizon. You are then asked to select your risk profile base on the 5 options:

I inputted my age, investment horizon, and selected the Conservative portfolio. It shows me a fixed income allocation of 76 per cent and a currency allocation of 15 per cent. It forecast a 7 per cent expected return.

Using the same age and investment horizon parameters, I re-selected the Very Aggressive portfolio. It shows me a 79 per cent fixed income allocation and 12 per cent currency allocation with equity at 0 per cent. The expected return is 10 per cent.

I am not exactly sure how they derived such asset allocation.

In addition, the fees consist of a 10 per cent performance fee based on a "high-watermark" area. These fees could be rather substantial and eat into the returns of an investor. Usually, such performance fees are only reserved for hedge funds, hence I am rather surprised that SquirrelSave has this component as part of its fee structure.

Some Robo advisors engage in a hybrid of assets beyond just ETFs but also using alternative investment funds etc which might increase the overall fee charges.

Unless there is a huge value proposition for such a platform, if not we believe that the total costs associated with such hybrids might not justify the returns associated with them.

OCBC RoboInvest was launched in Aug 2018, making it the first bank in Singapore to offer a Robo advisory solution.

Investors will have access to 28 baskets of portfolios comprising stocks and ETFs, specially curated by OCBC's wealth experts. There will be automated portfolio monitoring and re-balancing on a quarterly or biannual basis.

[[nid:485925]]

The Robo advisors invest in predominantly ETFs but there could be occasions where there could be a combination of both ETFs and equities. Investors can choose ETFs that are geographic centric, such as focusing only on Singapore-themes ETFs over US-based ETFs to avoid exchange-related fees.

OCBC RoboInvest has the highest advisory fees among all the Robo advisors in Singapore at a flat 0.88 per cent across all investment amounts. Adding in ETFs management fees and we are probably looking at all-in charges of approx. 1.2 per cent.

There are also other fees such as Exchange Fees & charges where applicable. For example, if you trade in the Hong Kong market, there' a stamp duty of 0.1 per cent of contract value and an exchange fee of 0.077 per cent of the contract value.

OCBC RoboInvest has an initial minimum investment amount of USD3,500 and depending on the portfolio you choose, the amount may be higher.

Similar to Phillips SMART Portfolio, FSM Maps is not driven by an algorithm but managed by a team of managers and research analysts.

FSM Maps features 5 portfolios, with all of them crafted to cater to different needs of investors.

The portfolio may invest in balanced funds, alternative investment funds, money market funds, and ETFs.

An advisory fee of 0.35 per cent-0.5 per cent is levied on the investments. Investors also have to fork out a transaction charge of 0.04 per cent as well as the relevant SGX clearing and Trading fees, including GST for ETF transactions. All-in charges could amount to the region of 1.0 per cent, based on our estimate.

There are options for a lump sum investment with a minimum sum of $1,000 or a regular saving plan with a minimum contribution of $500/month.

Unfortunately, there is no Robo advisor a present that ticks all the right boxes. Our ideal Robo advisor will be one with:

All-in charges of approx. 0.8 per cent/annum. We want a low-cost investment platform that does not eat into our returns. Based on our assessment of total charges, AutoWealth and Syfe (REIT portfolio) rank highly in this arena.

[[nid:486676]]

Provide a cheap RSP solution. The purpose of a Robo Advisor should be a fuss-free, cheap + automated solution for a newbie investor who probably also has a limited amount of capital to get started on his/her investment journey.

A low minimum investment barrier will be ideal. Concurrently, the option to invest a small amount every month on an automated basis will be welcomed as well.

A greater degree of customisation. We want to have the option of choosing between a purely passive investment route like AutoWealth but yet also has customisation features like that of Kristal.AI which allows for thematic investing for more advanced investors.

Ability to invest using CPF and SRS funds. Currently, only a few Robo advisors have the option of investing using SRS funds while Endowus is the first Robo advisor to get approval for investments using CPF funds.

The Robo Advisors in Singapore all provide different value propositions. While the common-theme across the board is that these Robo advisors tend to be lower cost in nature vs. traditional mutual funds, they all employ a myriad of algorithms/management philosophy.

If you highly favour a highly passive route that tracks key indices, then AutoWealth might be the right Robo advisor pick for you. If you wish for a more active approach, then StashAway's ERAA model might be a unique proposition for you.

If you are risk-averse and wants to control your maximum downside risk, then Syfe's ARI strategy might be your best option.

Ultimately, we believe the value-add of a Robo advisor is its ability to: Pick the CORRECT investment asset to invest for the RIGHT person.

For example, there are thousands of ETFs to choose from globally. Which are the right ones suited for a particular individual with a certain risk profile? Which Robo advisors can do it best? That again is the million-dollar question.

Another benefit will be the ability to engage in constant re-balancing that a DIY investor will not be able to execute at ease.

At the end of the day, we are betting that the algorithms driving these Robo advisors are better "stock" pickers than the average fund manager. Even if they are not, at least we are not "overpaying" for their services.

This article was first published in New Academy of Finance. All content is displayed for general information purposes only and does not constitute professional financial advice.