UOB personal loan review: Interest rates, approval times and loan amounts

PHOTO: MoneySmart

A personal loan is not something you should take out on a whim just because your bank account balance is getting low at the end of the month but you want to go shopping.

But if you're already in debt, consolidating it with a personal loan that charges lower interest rates than your existing lenders can be a smart move.

Let's check out the UOB personal loan to see whether it's worth your time.

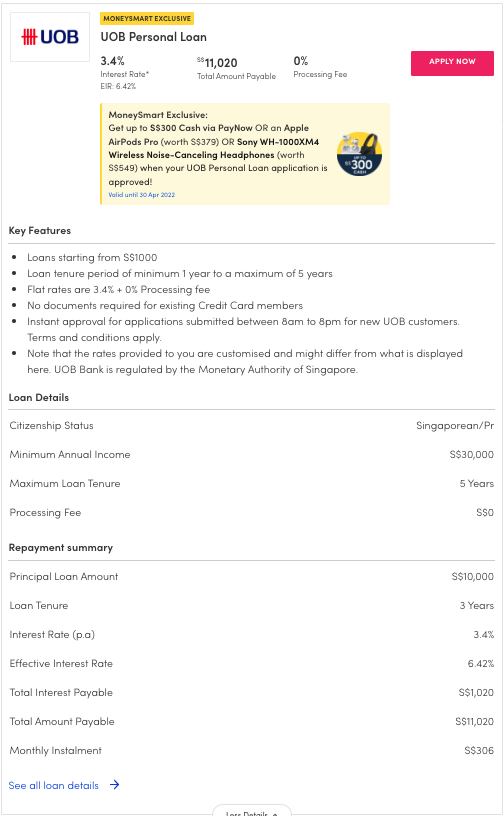

The most important factor for most of us when choosing a personal loan is interest rate. After all, if you're consolidating your loans, the whole idea is to get an interest rate that is lower than what you're currently paying.

UOB is currently offering a 3.4 per cent per annum interest rate on their personal loans when you sign up online. The Effective Interest Rate (EIR) of the UOB personal loan is estimated at 6.42 per cent p.a. for a three-year loan

What's the difference between the regular interest rate vs EIR (effective interest rate)?

Well, when you take out a personal loan, the hidden fees and charges can add up. In UOB's case, the zero per cent or one per cent (for one-year loans) processing fee are also factors to consider.

We won't get into it here, but if you're curious, here's how banks calculate effective interest rate.

In any case, the EIR is the actual interest rate you end up paying as a percentage of your loan. So when comparing between personal loans, always compare the EIR rather than the advertised rate.

The minimum amount you can borrow is $1,000, and the maximum will depend on your monthly income.

Well, let's see. For a loan of $10,000 taken over a period of three years, this is how much you would be paying in total:

$11,020 - $10,000 = $1,020 interest

So, how do these interest rates measure up compared to the personal loans offered by other banks in Singapore?

Honestly, this is a pretty decent personal loan currently. So, if you're looking for a better deal, look elsewhere.

READ ALSO: Why you should never take a personal loan for home renovations

From now till April 30, 2022, UOB is offering up to $600 cash rebate when you apply for a $30,000 UOB Personal Loan with a loan tenure of three years, four years or five years.

… But would we recommend borrowing MORE money just to hit the higher cashback tier? Absolutely not!

Because that cashback is going to be eaten by the amount of interest you pay UOB when repaying the loan.

When you're short of cash and need it fast, UOB offers two main solutions: The UOB Personal Loan and UOB Cash Plus. But what's the difference?

UOB Cash Plus is a line of credit. How it works is that you apply for the line of credit ahead of time, and once approved you have it on standby to use whenever you want.

You withdraw the money, generally at an ATM machine, when you wish to use it. You will then be charged interest on the sums you have withdrawn.

With the UOB Personal Loan, you need to make up your mind how much money you need ahead of time and how much time you need in order to repay it.

Once the money has been disbursed, you're locked into repaying a fixed sum every month.

Repaying money you've withdrawn through UOB Cash Plus, however, is a lot like repaying credit card debt. You only have to pay the minimum sum on your bill every month in order to get the debt collectors off your back. That means you can potentially roll a significant sum over to the next month.

You should definitely not do so, however, as credit lines like UOB Cash Plus typically charge much higher interest rates at 20.9 per cent than personal loans.

From now till June 30, 2022, UOB Cash Plus is offering a promotional three, six, or 12-month-long loans at zero per cent interest and minimal processing fees. Effective interest rates (EIR) make up to 1.11 per cent to 1.22 per cent.

But once that time is up, you'll be charged interest rates that are comparable to those of credit cards. Proceed with care!

UOB offers instant approval for both new and existing UOB customers, provided you apply during their operating hours from 8am to 9pm.

The cash will be deposited into a savings account of your choice.

Compared to credit card debt or UOB Cash Plus's line of credit, the interest rate charged by the UOB personal loan doesn't sound that high.

But it's still high! When you factor in the EIR, you're still losing a lot of money in order to borrow that cash.

So you should not be relying on personal loans on a regular basis. Rather, think of them as a last resort, only to be used in an emergency.

Ideally, you want to get your finances to the point where you'll never have to take out personal loans in the first place.

That could mean spending less or earning more per month, as well as accumulating an emergency fund that will give you a cash buffer for unexpected expenses.

READ ALSO: Personal loan pros & cons, and 5 things you should never use them for

This article was first published in MoneySmart.