Smart ways to maximise cashback rebates or rewards with cashless payments in Singapore

PHOTO: Unsplash

Today, there are many financial tools available to make payments in Singapore; Traditional methods like cash and credit cards, as well as newer digital platforms such as Apple Pay and GrabPay.

Some enjoy the physical thrills of wielding cash and credit cards to make payments, while others prefer the convenience that digital payments bring, with these digital platforms integrated with their smartphones.

However, do you know that if you are smart about how you pay, you can save a significant amount of money in the long run?

In Singapore where there is a steady inflation rate of 2-3 per cent each year, how are we able to best utilize the many payment methods out there in the market to earn the best deals and rewards for ourselves to combat this inflation?

Read on to find out more on how you can save as you pay.

Credit card companies are constantly competing to offer the most appealing rewards for their consumers; Some cards offer lucrative sign-up rewards, while others give higher cashback for spending categories such as air travel, food and transport.

Cashback cards are a convenient alternative to points and miles cards that can offset your monthly card bill by earning rebates on specific kinds of spending.

To find the best cashback credit card that maximises rebates for your budget based on your income and spending numbers, check out our rewards calculator to compare between credit cards and see what value you could get from each cashback card in Singapore.

Below is a list of credit cards suitable for every need:

PROMO: Receive a Dyson V8 Slim™ Fluffy, Nintendo Switch OLED, Samsonite Straren Spinner 67/24, or $350 cash with a min. spend of $500

Apply Now Apply Now Citi Cash Back+ Card offers one of the highest unlimited cashback rates on the market – 1.6 per cent, on all spend without restrictions, boosted to 4.5 per cent for the first three months since card approval. Read Review

Citibank Cash Back+ Card. Cardholders earn an unlimited 1.6 per cent cashback on all spend, which is higher than the 1.5 per cent offered by most competitors. In most cases, consumers with very large budgets end up feeling restricted by typical capped rewards cards. With Citi Cash Back+, however, affluent cardholders can continue to earn on all of their spend, up to their full rewards potential. ALSO READ: Going cashless pays off in the long run for soya bean hawker Individuals spending about $7,000+/month can truly maximise their earnings with. Cardholders earn an unlimited 1.6 per cent cashback on all spend, which is higher than the 1.5 per cent offered by most competitors. In most cases, consumers with very large budgets end up feeling restricted by typical capped rewards cards. With Citi Cash Back+, however, affluent cardholders can continue to earn on all of their spend, up to their full rewards potential. |

PROMO: Receive a Dyson V8 Slim™ Fluffy, Nintendo Switch OLED, Samsonite Straren Spinner 67/24, or $350 cash with a min. spend of $500

Apply Now Apply Now Citi Cash Back+ Card offers one of the highest unlimited cashback rates on the market – 1.6 per cent, on all spend without restrictions, boosted to 4.5 per cent for the first three months since card approval. Read Review

|

|

Citibank Cash Back+ Card. Cardholders earn an unlimited 1.6 per cent cashback on all spend, which is higher than the 1.5 per cent offered by most competitors. In most cases, consumers with very large budgets end up feeling restricted by typical capped rewards cards. With Citi Cash Back+, however, affluent cardholders can continue to earn on all of their spend, up to their full rewards potential. Individuals spending about $7,000+/month can truly maximise their earnings with. Cardholders earn an unlimited 1.6 per cent cashback on all spend, which is higher than the 1.5 per cent offered by most competitors. In most cases, consumers with very large budgets end up feeling restricted by typical capped rewards cards. With Citi Cash Back+, however, affluent cardholders can continue to earn on all of their spend, up to their full rewards potential. |

Apply Now Apply Now UOB One Card offers great cashback rates (up to 10 per cent) for consistent spenders looking to earn cashback on everyday essentials. Read Review

UOB One Card than with any other flat rebate card. Spend at this level earns 5 per cent cashback, up to $300/quarter–amongst the highest earning potentials on the market. This rate is further boosted to 10 per cent on Dairy Farm Singapore transactions, Grab and UOB Travel and 6 per cent on electric bills. Lower or inconsistent spend also earns 3.33 per cent up to $50 or $100/quarter (depending on minimum spend), but these rates are slightly less competitive. If you consistently spend $2,000/month, you’ll earn more with than with any other flat rebate card. Spend at this level earns 5 per cent cashback, up to $300/quarter–amongst the highest earning potentials on the market. This rate is further boosted to 10 per cent on Dairy Farm Singapore transactions, Grab and UOB Travel and 6 per cent on electric bills. Lower or inconsistent spend also earns 3.33 per cent up to $50 or $100/quarter (depending on minimum spend), but these rates are slightly less competitive. One of the best features of UOB One Card is that cardholders can ‘double’ their rebates through UOB SMART$ Programme, which also earns SMART$ credits with select merchants, which then offset future purchases. With UOB One Card, consumers can make the most of their daily spend, while only paying a $192.6 annual fee. Overall, this card is the best flat rebate option on the market for average spenders. |

Apply Now Apply Now UOB One Card offers great cashback rates (up to 10 per cent) for consistent spenders looking to earn cashback on everyday essentials. Read Review

|

|

UOB One Card than with any other flat rebate card. Spend at this level earns 5 per cent cashback, up to $300/quarter–amongst the highest earning potentials on the market. This rate is further boosted to 10 per cent on Dairy Farm Singapore transactions, Grab and UOB Travel and 6 per cent on electric bills. Lower or inconsistent spend also earns 3.33 per cent up to $50 or $100/quarter (depending on minimum spend), but these rates are slightly less competitive. If you consistently spend $2,000/month, you’ll earn more with than with any other flat rebate card. Spend at this level earns 5 per cent cashback, up to $300/quarter–amongst the highest earning potentials on the market. ALSO READ: Some hawkers not too keen on cashless payments after customers repeatedly dupe them This rate is further boosted to 10 per cent on Dairy Farm Singapore transactions, Grab and UOB Travel and 6 per cent on electric bills. Lower or inconsistent spend also earns 3.33 per cent up to $50 or $100/quarter (depending on minimum spend), but these rates are slightly less competitive. One of the best features of UOB One Card is that cardholders can ‘double’ their rebates through UOB SMART$ Programme, which also earns SMART$ credits with select merchants, which then offset future purchases. With UOB One Card, consumers can make the most of their daily spend, while only paying a $192.6 annual fee. Overall, this card is the best flat rebate option on the market for average spenders. |

| Apply Now Apply Now |

|

American Express Singapore Airlines KrisFlyer Card. Cardholders earn 1.1 miles per $1 on general spend (Two miles overseas in June & December), two miles with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab rides (up to 620 mi/mo). Rewards are earned directly as KrisFlyer miles, which are credited to the consumer's frequent flyer loyalty account. This is great because cardholders never have to worry about conversion rates, transfer fees or lengthy processing times. Amex SIA KF Card is also quite affordable with a $176.55 fee, waived the first year. Overall, if you prefer taking SIA flights and want a straightforward miles card, this could be the option for you. If you're interested in applying for your first miles credit card and tend to fly with SIA, you may want to consider. Cardholders earn 1.1 miles per $1 on general spend (Two miles overseas in June & December), two miles with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab rides (up to 620 mi/mo). Rewards are earned directly as KrisFlyer miles, which are credited to the consumer's frequent flyer loyalty account. This is great because cardholders never have to worry about conversion rates, transfer fees or lengthy processing times. Amex SIA KF Card is also quite affordable with a $176.55 fee, waived the first year. Overall, if you prefer taking SIA flights and want a straightforward miles card, this could be the option for you. |

|

| Apply Now Apply Now |

|---|

|

|

|

American Express Singapore Airlines KrisFlyer Card. Cardholders earn 1.1 miles per $1 on general spend (two miles overseas in June & December), two miles with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab rides (up to 620 mi/mo). Rewards are earned directly as KrisFlyer miles, which are credited to the consumer's frequent flyer loyalty account. This is great because cardholders never have to worry about conversion rates, transfer fees or lengthy processing times. Amex SIA KF Card is also quite affordable with a $176.55 fee, waived the first year. Overall, if you prefer taking SIA flights and want a straightforward miles card, this could be the option for you. If you're interested in applying for your first miles credit card and tend to fly with SIA, you may want to consider. Cardholders earn 1.1 miles per $1 on general spend (two miles overseas in June & December), two miles with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab rides (up to 620 mi/mo). Rewards are earned directly as KrisFlyer miles, which are credited to the consumer's frequent flyer loyalty account. This is great because cardholders never have to worry about conversion rates, transfer fees or lengthy processing times. Amex SIA KF Card is also quite affordable with a $176.55 fee, waived the first year. Overall, if you prefer taking SIA flights and want a straightforward miles card, this could be the option for you. |

PROMO: Receive a Dyson V8 Slim™ Fluffy, Nintendo Switch OLED, Samsonite Straren Spinner 67/24, or $350 cash with a min. spend of $500

Apply Now Apply Now Citi Prestige MasterCard offers high rewards on food delivery and home entertainment (4mi/$1), and several luxury travel perks making it an overall great travel card. Read Review

Affluent travellers who prioritise luxury perks should consider. Cardholders earn 1.3 miles per $1 locally, two miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30 per cent annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure. Citi Prestige Card also offers more privileges than almost any other travel cards. Cardholders receive unlimited airport lounge access with no minimum spend requirements, free limo transfers, free hotel bonus nights, golfing privileges and more. While the $535 fee is high, it’s reflected in the value returned to consumers and further offset by 25,000 annual renewal miles, worth about $250. Ultimately, market-leading rates and luxury perks make Citi Prestige the best card for affluent travellers. |

PROMO: Receive a Dyson V8 Slim™ Fluffy, Nintendo Switch OLED, Samsonite Straren Spinner 67/24, or $350 cash with a min. spend of $500

Apply Now Apply Now Citi Prestige MasterCard offers high rewards on food delivery and home entertainment (4mi/$1), and several luxury travel perks making it an overall great travel card. Read Review

|

| Citi Prestige MasterCard. Cardholders earn 1.3 miles per $1 locally, two miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30 per cent annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure.

Affluent travellers who prioritise luxury perks should consider. Cardholders earn 1.3 miles per $1 locally, two miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30 per cent annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure. Citi Prestige Card also offers more privileges than almost any other travel cards. Cardholders receive unlimited airport lounge access with no minimum spend requirements, free limo transfers, free hotel bonus nights, golfing privileges and more. While the $535 fee is high, it’s reflected in the value returned to consumers and further offset by 25,000 annual renewal miles, worth about $250. Ultimately, market-leading rates and luxury perks make Citi Prestige the best card for affluent travellers. |

While OCBC 365 Card offers great cashback on everyday essentials, unlike its competitors, it has a relatively high cashback cap ($80/mo), a simple rewards structure and fewer merchant restrictions. Read Review

OCBC 365 Card offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6 per cent rebates on dining and 3 per cent on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty $80/month. Another perk is that cardholders can enjoy a fee waiver with $10,000 annual spend – that's just $833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver. Offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6 per cent rebates on dining and 3 per cent on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty $80/month. Another perk is that cardholders can enjoy a fee waiver with $10,000 annual spend – that's just $833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver. |

While OCBC 365 Card offers great cashback on everyday essentials, unlike its competitors, it has a relatively high cashback cap ($80/mo), a simple rewards structure and fewer merchant restrictions. Read Review

|

|

OCBC 365 Card offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6 per cent rebates on dining and 3 per cent on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty $80/month. Another perk is that cardholders can enjoy a fee waiver with $10,000 annual spend – that's just $833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver. Offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6per cent rebates on dining and 3 per cent on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty $80/month. Another perk is that cardholders can enjoy a fee waiver with $10,000 annual spend – that's just $833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver. |

PROMO: New DBS/POSB Cardmembers can get $150 cash back with a min. spend of $800

Apply Now Apply Now DBS Live Fresh Card offers 5 per cent cashback on online and contactless spend, and an additional 5 per cent green cashback, making it perfect for modern young professionals. Read Review

DBS Live Fresh Card. Cardholders earn an impressive 5 per cent cashback for spend in both categories, and an additional 5per cent on sustainable spend, with a total monthly cashback cap at $75/month. There is a $600 minimum spend requirement to access these rates, but it's slightly lower than the $800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods. If you're a modern spender who frequently shops online and feels comfortable using digital wallets, look no further than. Cardholders earn an impressive 5 per cent cashback for spend in both categories, and an additional 5 per cent on sustainable spend, with a total monthly cashback cap at $75/month. There is a $600 minimum spend requirement to access these rates, but it's slightly lower than the $800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods. |

PROMO: New DBS/POSB Cardmembers can get $150 cash back with a min. spend of $800

Apply Now Apply Now DBS Live Fresh Card offers 5 per cent cashback on online and contactless spend, and an additional 5 per cent green cashback, making it perfect for modern young professionals. Read Review

|

|

DBS Live Fresh Card. Cardholders earn an impressive 5 per cent cashback for spend in both categories, and an additional 5 per cent on sustainable spend, with a total monthly cashback cap at $75/month. There is a $600 minimum spend requirement to access these rates, but it's slightly lower than the $800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods. If you're a modern spender who frequently shops online and feels comfortable using digital wallets, look no further than. Cardholders earn an impressive 5 per cent cashback for spend in both categories, and an additional 5 per cent on sustainable spend, with a total monthly cashback cap at $75/month. There is a $600 minimum spend requirement to access these rates, but it's slightly lower than the $800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods. |

Here is an example of using several credit cards with a monthly spend of $3,000:

| Credit Card | Monthly payment | Annual Card Fees | Monthly Cashback | Annual Cashback | Net Savings per Year |

|---|---|---|---|---|---|

| UOB One Card | $2,000 (House/Car Loan) | $192.60 | $100 | $1,200 | $1,007.40 |

| OCBC 365 Card | $500 (Food) | $192.60 | $30 | $360 | $167.40 |

| DBS Live Fresh | $500 (Online Shopping + Groceries) | $192.60 | $25 | $300 | $107.40 |

| $1,282.20 |

By using the best credit card for individual spend categories, you can maximise your cashback and save up to $1,282.20 every year.

We’re seeing increased adoption of digital payments in schools and across the nation, not to mention government announcements of expanding digital payment infrastructure across the country.

With the increasing number of digital payment options and each offering varying rewards and promotions, how are we able to identify which is the best platform to use to get the best deals for ourselves?

Listed below are some platforms we have identified for you and how to go about getting the best deals.

Since its launch in 2016, GrabPay has evolved from an e-wallet with basic payment features to a popular payment option in Singapore.

Although Grab has seen a devaluation of its points across transactions back in January 2020, Grab remains to be a popular payment option with its wide merchant acceptance pool and ever-increasing partnerships to offer more lucrative rewards to its users.

You can still continue to maximise the opportunity to earn points and cash rebates across all platforms with GrabPay.

Here’s how to do so:

For those who want to maximize the number of Grab points earned, the GrabPay Card accelerator allows you to earn an additional 0.8 per cent cashback, on top of your current cashback based on your membership tier, by spending on selected categories:

Do take note that booster points are capped at a maximum of 20 transactions per month and 500 points for each transaction. Strategise well to make full use of this reward scheme!

Besides using your GrabPay wallet or Mastercard at merchants, you can also maximise the potential of earning additional cashback by linking your GrabPay account to other platforms such as the Fave App or Samsung Pay.

This approach allows you to earn GrabPay points, cashback from FavePay transactions as well as Samsung Reward points. For the same spending, you earn double to triple the points.

That’s not all, some credit cards issue points or cash rebates for topping up their e-wallet using their credit cards, including GrabPay.

This means that you can continue to stack the rewards with the same spending!

Using GrabPay for your expenses allows you to reach higher membership tiers and earn Grab points faster with every purchase.

Assuming that you are a Platinium member, you could earn up to 9,800 Grab Points with a monthly expense of $1,000. Here is a breakdown of how to do so:

| Categories | Money Spent | Points Earned | Additional Points (Accelerator) | Total Points Earned |

|---|---|---|---|---|

| Groceries | $300 | 1800 | 1200 | 3000 |

| Dining | $300 | 1800 | 1200 | 3000 |

| Transport | $50 | 300 | 0 | 300 |

| Streaming Apps | $25 | 150 | 100 | 250 |

| Online Shopping | $200 | 1200 | 800 | 2000 |

| Gym | $125 | 750 | 500 | 1250 |

| $1,282.20 |

Here are some of the redeemable rewards from the various categories available on the GrabRewards catalogue.

Food & beverage:

Shopping:

Services & entertainment:

Alternatively, you could use the points to offset purchases within the Grab App, such as GrabMart, GrabFood or Grab Car rides.

ShopeePay is the digital wallet service offered by Shopee. ShopeePay allows you to make both in-app payments and offline transactions by scanning the merchant’s ShopeePay or SGQR code.

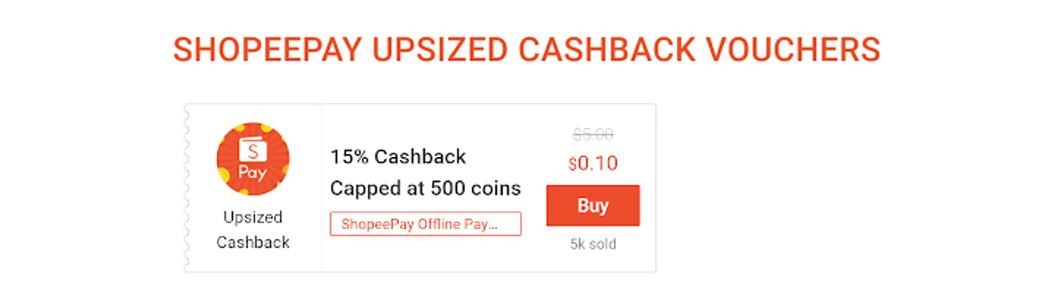

Enjoy upsized cashback vouchers of up to 18 per cent cashback for your in-app purchases. You are able to stack cashback vouchers on top of seller vouchers to enjoy greater savings, especially during monthly sales such as Black Friday or the 11.11 sale.

In addition, you could stand to win seasonal prizes and be part of exciting lucky draw prizes when you top up your account or transfer funds to other users using ShopeePay!

In addition to the 2 per cent cashback capped at $1 whenever you make payment by ShopeePay, ShopeePay Scan & Pay vouchers offer direct discounts or cashback at the price of $0.10 or $0.01. These discounts and cashback vouchers differ from merchant to merchant so do remember to check the app to see what kind of vouchers your favourite brands offer!

For first time users, enjoy up to $5 off on your first purchase with ShopeePay Scan & Pay vouchers with your favourite brands!

ShopeePay also offers upsized cashback vouchers of 15 per cent cashback capped at 500 coins at the price of $0.10 that is applicable to all merchants that accept ShopeePay as a payment method.

However, do take note that these vouchers are not stackable. In addition, users are limited to one voucher per visit. Be strategic about when and what you use the vouchers on!

During major events such as the 11.11 sale or the celebration of Shopee’s birthday on 12.12, be on the watch out for ShopeePay rewards to reap the best benefits!

Promotions during the 11.11 sale include: Plant a ShopeePay seed on Shopee Farm from Nov 8 to Nov 14 with a minimum top-up of $8 to the Shopee wallet and stand to win an additional $100 Shopee vouchers. 90per cent off deals with ShopeePay. Limited-time only vouchers on popular brands.

BNPL payments are all the rage now in Singapore. So, what’s the fuss with BNPL?

BNPL, as its name suggests, allows you to delay your payments and split them up into monthly installments. Pay your balance on time, and zero interest is charged. If you miss a payment, you would be charged a late payment fee ranging up to $60, depending on your BNPL provider.

| BNPL Provider | Installment | Late Payment Fee |

|---|---|---|

| Atome | 3 months | $15 – $30 |

| Hoolah | 3 months | $5 – $30 |

| Grab PayLater | Up to 4 months | $10 |

| OctiFi | 3 months | From $15 |

| Pace | 3 months | $10 – $60 |

| Rely | Up to 3 months | $1 – $40 |

| Split | 3 months | None |

BNPL has a similar framework to your traditional 0per cent credit card installment plans, but with the addition of multiple perks.

Suppose you are making an online purchase of $3,000 on a desktop computer using your OCBC Frank Card that gives you a 6per cent rebate capped at $75 per month.

Although there is a 6 per cent rebate offered that should warrant you a cashback of $180, there is a monthly cap of $75. Hence, you are only able to get back $75 and miss out on $115. How are you able to ensure that this $115 that you have missed out goes into your bank account? Do you look for another credit card with a higher cap per month?

BNPL solves this problem without the need to look for alternative credit cards or payment methods. Suppose you put the purchase on a three-month installment plan with Atome. Each month you are charged $1,000 and awarded a cashback of $60, a figure below the monthly cap of your Frank Card. After three months, you will have received a total of $180 in cashback.

Do note, however, that while BNPL programmes are great for extending your dollars, you have to exercise prudence in your spending as the lack of discipline might land you in more debts.

As you will not be paying the full amount upfront via BNPL, you will be able to keep a sum of the amount for a period of one to two months and receive interest on the balance in your bank account or insurance savings plan, or receive earnings on your investments.

Although this may not amount to much depending on the interest rates your bank or savings plan offer, who would say no to money!

Since BNPL payment services are rather new in Singapore, BNPL providers are giving attractive rewards to attract and acquire customers, so as to gain a larger market share.

Atome: $10 off first online purchase. Merchant-specific discount vouchers.

Pace: OCBC Yes! Debit Card holders $50 off with min. spend $250. Merchant-specific vouchers.

Rely: 12 per cent cashback on first transaction. Merchant-specific cashback vouchers

There are so many payments out there in the market with attractive rewards and perks. Some prefer direct cash discounts, others prefer cashback rewards, while the rest prefer to pay in installments.

This article was first published in ValueChampion.