CIMB World Mastercard review 2021: Unlimited cashback of up to 2% but there's a catch

PHOTO: Unsplash

Cashback credit cards are some of the most worthwhile cards to sign up for because they’re essentially giving you free money. Seeing as even McDonald’s charges for sauce these days, we’ll take whatever free stuff we can get.

But most cashback cards require you to satisfy minimum spending requirements and impose a cap on the amount of cashback you can earn each month — meaning you have to work for that “free” money.

Not so for CIMB World Mastercard, which professes to offer unlimited cashback of up to 2 per cent.

But is it really as good as it sounds? Let’s find out.

|

CIMB World Mastercard |

|

|

Annual fee & waiver |

Free |

|

Supplementary annual fee |

Free |

|

Interest free period |

23 days |

|

Annual interest rate |

25.9 per cent |

|

Late payment fee |

$100 |

|

Minimum monthly repayment |

3 per cent or $50, whichever is higher |

|

Foreign currency transaction fee |

3 per cent |

|

Cash advance transaction fee |

6 per cent or $15, whichever is higher |

|

Overlimit fee |

$50 or 5 per cent of excess, whichever is higher |

|

Minimum income |

$30,000 |

|

Card association |

MasterCard |

|

Wireless payment |

MasterCard PayPass |

CIMB World Mastercard has declared itself the most generous unlimited cashback card in Singapore, offering cashback of 2 per cent, with no minimum spending requirement and no cashback cap.

2 per cent is certainly generous when you consider that the next best unlimited cashback cards are only offering 1.5per cent to 1.7 per cent cashback. But alas, reality doesn’t quite match up to the advertising.

First of all, unlimited cashback cards in Singapore usually offer cashback on all spending. By contrast, the CIMB World Mastercard only offers 2 per cent cashback on spending in certain categories, namely: drinking, dining and online food delivery, movies and digital entertainment, taxis and automobile and luxury goods.

There is another catch. You only qualify for the 2 per cent cashback on these spending categories when you spend $1,000 and above in a statement month. If you don’t manage to spend $1,000, you get only 1 per cent cashback.

What about miscellaneous spending outside of these above-mentioned categories? You can get 1per cent cashback… but only if you spend at least $500 in a statement month.

Unlimited cashback cards tend to be useful because they let you spend on those big-ticket, miscellaneous purchases that no other card will be able to reward you adequately for. Things like wedding dinners and home renovations.

But you wouldn’t be able to do that with the CIMB World Mastercard, which limits the 2 per cent cashback to a few categories.

Those who can benefit most from this card are high spenders who have no problem hitting at least $1,000 a month in the eligible categories.

The problem is that some of these categories like dining and/or transport already enjoy more generous cashback through other cards like Citi Cash Back Card and CIMB’s own Visa Signature Card, with less onerous minimum spending requirements.

So, in the end, people who would truly benefit from this card would probably be high rollers who have busted the cashback caps on their other cards and are looking for an alternative way to earn cashback on spending in the eligible categories… and who are still able to meet the card’s $1,000 spending requirement.

For instance, if you’re looking to buy a $20,000 Hermes handbag, you could get 2 per cent cashback or $400 back by using the card to pay, since one of the eligible categories is luxury goods. In this case, it’d be hard to find another card that would be willing to pay $400 worth of cashback in a single month.

What’s the card’s biggest plus? It is free for life. So, there’s no harm in just applying for it and keeping it on hand in case you, too, decide to buy a $20,000 Hermes handbag someday.

Truth be told, the newly-revamped CIMB World Mastercard isn’t for everyone. It’s really for a specific kind of person who spends a lot on drinking, dining and luxury shopping. That probably applies to a significant chunk of Singaporeans, though.

However, if this credit card unfortunately doesn’t suit you, there are plenty of other unlimited cashback cards to choose from. Here are some of the best.

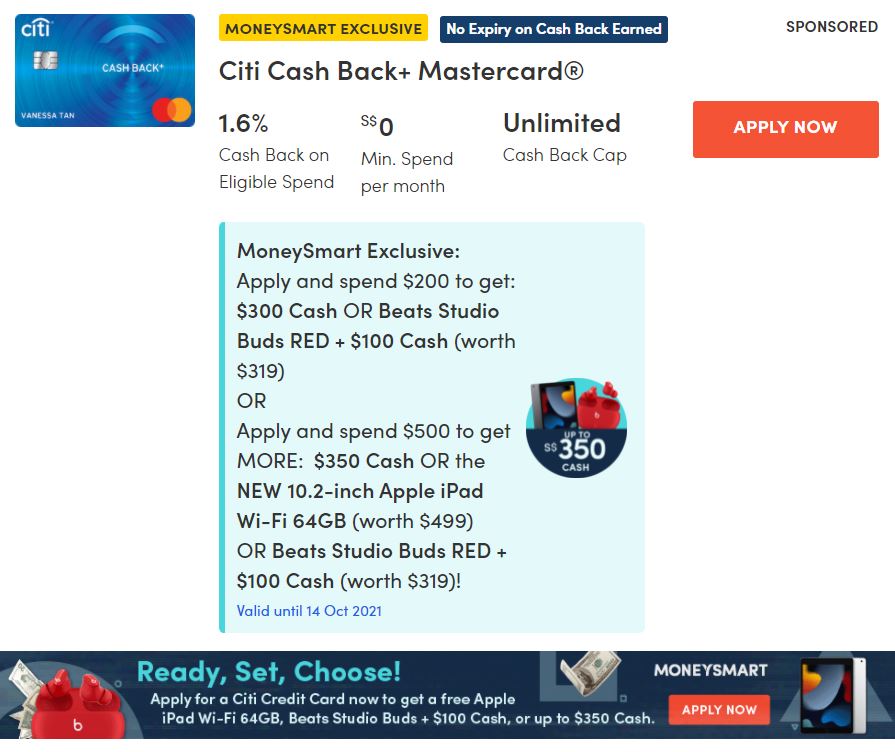

Citi Cash Back+ Card – 1.6 per cent cashback on all spending, with no cashback cap and no minimum spend. What’s more, in your first three months with the card, you get 4.5 per cent cashback on up to $5,000 worth of spending.

Standard Chartered Unlimited Cashback Card – 1.5 per cent cashback on all spending, with no cashback cap and no minimum spend. New sign-ups get cashback upon hitting the minimum spend requirement and six free months of Disney+.

UOB Absolute Cashback Card – 1.7 per cent cashback on all spending, with no cashback cap and no minimum spend. Just note that it’s an American Express card and some merchants don’t accept it.

This article was first published in MoneySmart.