What is SGFindex, and should you bother setting it up?

PHOTO: MoneySmart

The glory days of high-interest savings accounts are over, and we're left weeping over the ravages of our rapidly depreciating cash savings.

The good news is that the DBS Multiplier Account has just added SGFindex as a way to earn bonus interest, something we all desperately need.

But what the heck is SGFindex and how do we use it to get at that bonus interest? Let's find out.

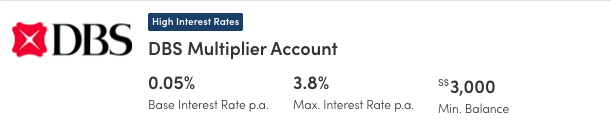

Even if you're not a DBS Multiplier account holder, you might already have come across it in your search for a high-interest savings account as it's one of the more attractive options available.

In a nutshell, DBS Multiplier offers bonus interest on your savings when you fulfil certain requirements.

The one requirement that is compulsory for everyone is to credit salary or dividends to the account.

Once you've done that, you can go on to fulfil other requirements in order to earn bonus interest, like spending on your DBS credit card, repaying your home loan instalments, buying insurance and investing.

Until recently, those aged 30 and above who didn't have a salary or dividends to credit to the account weren't eligible to earn bonus interest through DBS Multiplier.

This included freelancers or self-employed people who didn't receive a monthly salary as well as those who were taking a break from work.

All that has changed, because you can now satisfy the compulsory requirement by connecting your DBS account with SGFindex. And did I mention that it's free?

SGFindex, or Singapore Financial Data Exchange, is a sort of financial planning interface set up jointly by the MAS and the Smart Nation and Digital Government Group (SNDGG).

SGFindex consolidates all your financial information and links it using your SingPass. You will be able to retrieve the following data in one place:

All financial data that the government has will be accessible via SGFindex. That includes any info from the CPF Board, IRAS and HDB.

Meanwhile, any data from participating banks can only be released to SGFinDex after you have authorised them to do so. Your authorisation is valid for one year.

At the moment, the seven participating banks are:

The biggest advantage of using SGFindex is convenience. Instead of logging in multiple times to various government and banking websites, you've now got a one-stop shop where you can check most of your financial data.

If you're juggling multiple accounts, cards and loans from more than one bank, SGFindex helps you keep track of them all.

Unfortunately, it's convenient not only for you but also would-be hackers, identify thieves and so on. By consolidating everything in one place, you could potentially be giving these villains easy access to your financial data.

SGFindex uses a data transmission process that's supposed to be secure. They claim that personal financial data is neither read nor stored, and everything is encrypted during retrieval.

For most laymen this explanation is enough but if you're really worried, you might want to ask a cyber security expert for their take on this.

As for information from the banks, no data will be retrieved until you have given consent. So don't worry, if you have a bank account where you're hiding your secret riches, nobody has to know if you don't connect that bank to SGFindex.

You can access SGFindex through the website of a participating bank by first logging in and authorising your bank to release data.

It can be tricky to find the website through which you authorise SGFindex, as some banks require you to do so on their main page while others have created a separate page. For DBS account holders you will have to first go to the NAV Planner page.

Next, you will be directed to log in and authenticate your request using your SingPass. If completed successfully, the bank will be displayed when you log into SGFinDex.

You'll need to repeat this process with all the banks you're using.

(For DBS Multiplier Account holders, once you've authorised DBS to share information with SGFinDex, the bank should automatically be able to detected that you've done so. Don't forget to request for NAV Planner to retrieve information through SGFinDex every month in order to satisfy the Multiplier account's compulsory requirement.)

Once you've connected all your banks, you can access your SGFindex info in many ways-through one of your banks' apps or websites or by logging into the government's MyMoneySense website.

You can also use the DBS Nav Planner app even if you're not a DBS customer.

ALSO READ: Side hustle ideas for students: How to earn extra money while studying

This article was first published in MoneySmart.